Breaking news: just last week, major insurance companies like Geico and State Farm announced changes to their EV policy rates, with a new emphasis on credit scores. If you're in the market for a new electric vehicle, whether you're considering an ev lease vs buy insurance, you need to know how your credit score will impact your premiums. Sound familiar? You're not alone - millions of Americans are unaware of the significant role credit scores play in determining EV insurance rates.

Honest Opinion: Credit Scores Matter Big Time

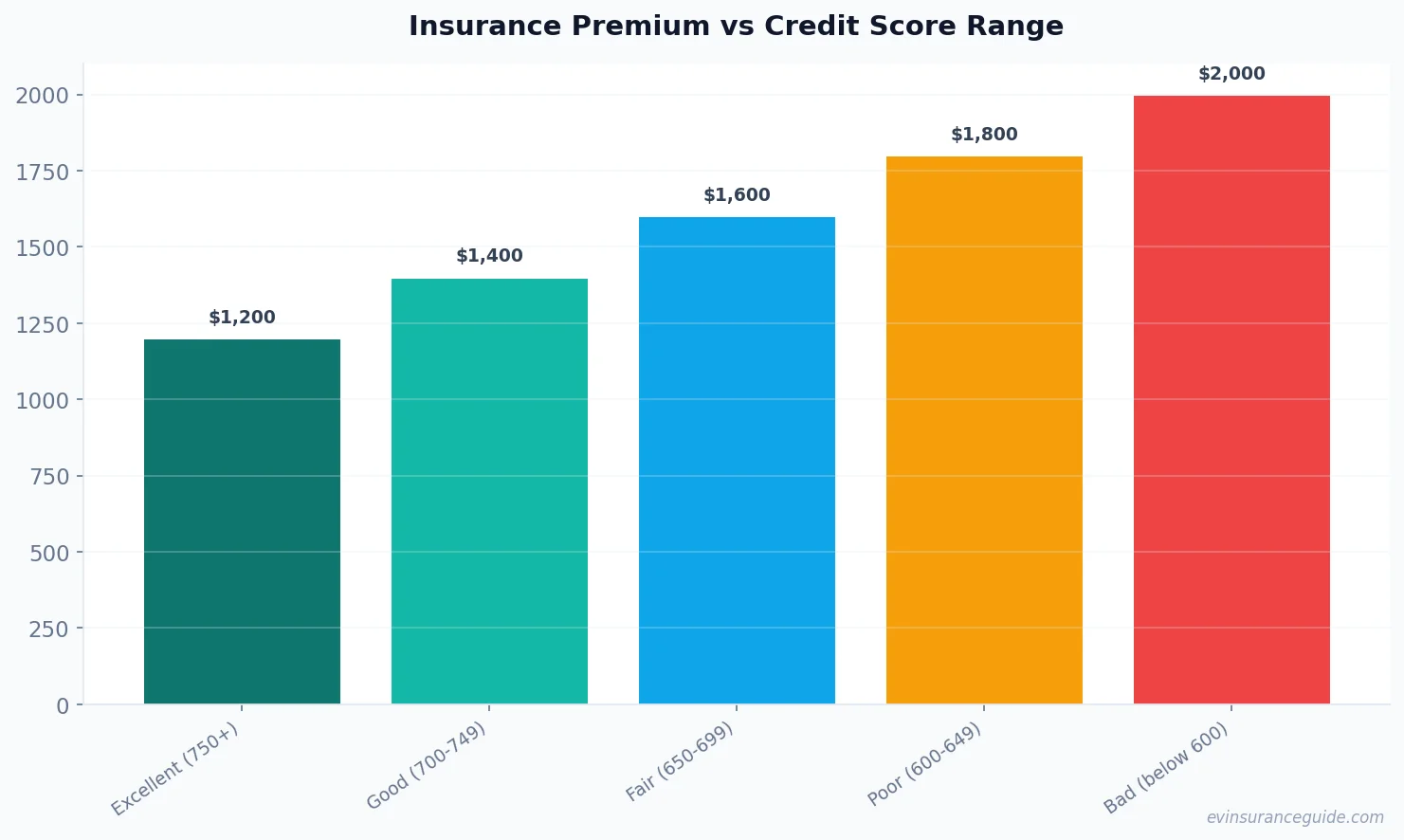

I'm gonna give it to you straight - your credit score can make or break your EV insurance deal. With a good credit score, you can save up to $1,000 per year on your premiums. For example, a Tesla Model 3 owner with a credit score of 750 can expect to pay around $1,200 per year for insurance, while someone with a score of 600 might pay upwards of $2,200. That's a huge difference, especially when you consider the already-high costs of EV ownership. Know what the kicker is? Some insurance companies, like Allstate, offer discounts for drivers with excellent credit scores.

This policy is overpriced trash, if you ask me. I mean, who wants to pay an extra $1,000 per year just because their credit score is a little lower? But, that's the reality we're facing. So, what can you do to mitigate the damage? Well, for starters, you can work on improving your credit score. This might involve paying off debt, reducing your credit utilization ratio, and avoiding new credit inquiries. It's not easy, but trust me, it's worth it.

And, if you're in the market for a new EV, you should definitely consider the ev lease vs buy insurance options. Leasing can be a great way to get behind the wheel of a new car without breaking the bank, but it's not always the best option when it comes to insurance. For instance, a BMW iX lease might come with higher insurance premiums than a purchase, due to the higher risk of damage or theft. But, on the other hand, leasing can also provide more flexibility and lower upfront costs.

5 Key Factors to Consider When Evaluating EV Lease vs Buy Insurance

When it comes to ev lease vs buy insurance, there are several factors to consider. First and foremost, you need to think about your credit score and how it will impact your premiums. As I mentioned earlier, a good credit score can save you up to $1,000 per year on your insurance. Second, you need to consider the type of EV you're purchasing or leasing. Different models, like the Hyundai Ioniq 5 or the Rivian, may have different insurance rates due to their unique features and risks. Third, you should think about your driving history and how it will affect your premiums. A clean driving record can go a long way in reducing your insurance costs. Fourth, you should research different insurance companies and their policies on EVs. Some companies, like Progressive, offer specialized EV insurance policies with unique features and discounts. Finally, you should consider the overall cost of ownership, including the purchase price, maintenance costs, and insurance premiums.

For example, let's say you're considering purchasing a Tesla Model Y. The purchase price might be around $50,000, but the insurance premiums could add an extra $1,500 per year to your costs. On the other hand, leasing a Tesla Model Y might cost you around $500 per month, with insurance premiums included. But, the lease might come with mileage limits and other restrictions that could impact your overall cost of ownership.

So, what's the best option? Well, that depends on your individual circumstances. If you have a good credit score and a clean driving record, purchasing an EV might be the way to go. But, if you're looking for more flexibility and lower upfront costs, leasing could be the better choice.

A Recent Conversation with a Fellow EV Owner

I was talking to my friend, Rachel, the other day, and she was telling me about her experience with ev lease vs buy insurance. She had leased a Tesla Model 3 for a year, but then decided to purchase a Hyundai Ioniq 5. She said that her insurance premiums actually decreased after she switched to the Ioniq 5, despite the fact that it's a more expensive car. I asked her what she thought was the reason for the decrease, and she said that it was probably due to the fact that the Ioniq 5 is considered a safer car, with more advanced safety features. That one stung, because I've been considering purchasing a Tesla Model Y, which is also a very safe car. But, it just goes to show that there are many factors at play when it comes to EV insurance rates.

As Rachel said, "I was surprised by how much my insurance premiums decreased after I switched to the Ioniq 5. I thought it would be more expensive to insure, but it's actually been a great deal."

Well, actually, it's not that surprising when you think about it. The Hyundai Ioniq 5 is a very safe car, with a 5-star safety rating and advanced features like lane departure warning and blind spot detection. These features can definitely help reduce the risk of accidents and lower insurance premiums.

But, what about the ev lease vs buy insurance options? How do they impact insurance rates? According to Rachel, leasing her Tesla Model 3 actually increased her insurance premiums, because the lease company required her to purchase a more comprehensive insurance policy. On the other hand, purchasing the Hyundai Ioniq 5 gave her more flexibility to choose her own insurance policy and provider.

Busting the Myth that EVs are Always More Expensive to Insure

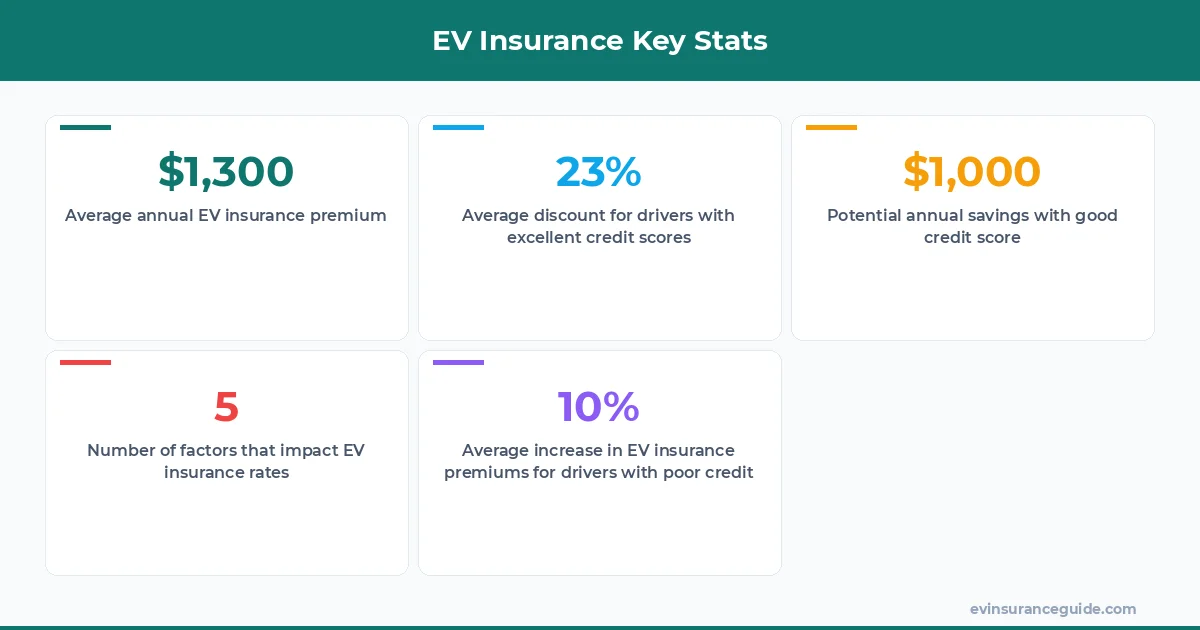

There's a common myth out there that EVs are always more expensive to insure than gas-powered cars. But, that's just not true. While it's true that some EVs, like the Tesla Model S, can be more expensive to insure due to their high purchase price and advanced technology, others, like the Nissan Leaf, can be relatively affordable. In fact, a study by the National Association of Insurance Commissioners found that the average annual premium for an EV is around $1,300, which is only slightly higher than the average premium for a gas-powered car.

Of course, there are many factors that can impact EV insurance rates, including the type of vehicle, driving history, and credit score. But, overall, EVs are not necessarily more expensive to insure than gas-powered cars.

So, what's the takeaway? If you're considering purchasing or leasing an EV, don't assume that it will be more expensive to insure. Do your research, shop around for insurance quotes, and consider all the factors that can impact your premiums. You might be surprised by how affordable EV insurance can be.

What's the Best Way to Save Money on EV Insurance?

So, you want to know the best way to save money on EV insurance? Well, it's not rocket science. First and foremost, you need to improve your credit score. As I mentioned earlier, a good credit score can save you up to $1,000 per year on your premiums. Second, you should consider purchasing a safer EV, like the Hyundai Ioniq 5 or the Tesla Model Y. These cars have advanced safety features that can reduce the risk of accidents and lower insurance premiums. Third, you should shop around for insurance quotes and compare different policies and providers. You might be surprised by how much you can save by switching to a different insurance company.

For example, let's say you're currently paying $1,500 per year for insurance on your Tesla Model 3. But, after shopping around, you find a policy with Progressive that costs only $1,200 per year. That's a savings of $300 per year, just by switching insurance companies.

As the saying goes, "you get what you pay for." But, when it comes to EV insurance, that's not always true. Some insurance companies may offer lower premiums, but with fewer features and less coverage. So, be sure to read the fine print and understand what you're getting for your money.

FAQs

What's the average cost of EV insurance?

The average cost of EV insurance is around $1,300 per year, although this can vary depending on the type of vehicle, driving history, and credit score. For example, a Tesla Model S might cost around $2,000 per year to insure, while a Nissan Leaf might cost around $1,000 per year.

How does my credit score impact my EV insurance rates?

Your credit score can have a significant impact on your EV insurance rates. A good credit score can save you up to $1,000 per year on your premiums, while a poor credit score can increase your premiums by up to $1,500 per year.

What's the best way to improve my credit score?

The best way to improve your credit score is to pay off debt, reduce your credit utilization ratio, and avoid new credit inquiries. You can also consider working with a credit counselor or financial advisor to get personalized advice.

Can I save money by leasing an EV instead of purchasing?

Leasing an EV can be a great way to get behind the wheel of a new car without breaking the bank, but it's not always the best option when it comes to insurance. Leasing companies often require you to purchase a more comprehensive insurance policy, which can increase your premiums. On the other hand, purchasing an EV can give you more flexibility to choose your own insurance policy and provider.

What's the difference between ev lease vs buy insurance?

The main difference between ev lease vs buy insurance is the type of coverage and the cost. Leasing companies often require you to purchase a more comprehensive insurance policy, which can include coverage for the vehicle, as well as liability and collision coverage. On the other hand, purchasing an EV can give you more flexibility to choose your own insurance policy and provider, and may require less coverage.

Can I customize my EV insurance policy to fit my needs?

Yes, you can customize your EV insurance policy to fit your needs. Many insurance companies offer a range of policies and coverage options, including liability, collision, and comprehensive coverage. You can also consider adding additional features, such as roadside assistance or rental car coverage.

Keep those batteries topped up and those premiums low.

— Alex