Over at the Electrify America station off Route 66 last week, two guys were leaning against their cars while the Tesla Model Y and Hyundai Ioniq 5 juiced up. One was complaining about his renewal notice jumping 40 percent just because he switched from a gas sedan to an EV. The other guy mentioned he leases his BMW iX and pays way less for the same coverage level. Their back-and-forth got me thinking hard about ev lease vs buy insurance and how the whole industry is scrambling to catch up with battery packs and repair costs.

That chat stuck with me because it highlighted something bigger than one bad quote. Insurance carriers have spent the last three years rewriting playbooks around EV-specific risks like battery replacement and high-voltage repair labor. Some moves help drivers. Others quietly pad profits. If you're weighing ev lease vs buy insurance for a Rivian or Tesla Model 3, the differences can swing your annual bill by over a thousand bucks.

Claims data from the last two years shows average EV repair costs sitting at $4,800 compared to $2,900 for similar gas cars. That gap forces carriers to test new rating factors like charger type and software update frequency. Wild, right?

Repair Shop Realities vs Traditional Auto Claims

Body shops used to swap fenders and call it a day. Now a fender bender on a Tesla Model Y can mean recalibrating cameras and checking the battery cooling system. Progressive started rolling out specialized EV repair networks in 2023, cutting average claim times by 11 days in pilot cities. State Farm followed with their own certified tech program for Hyundai Ioniq 5 and Kia EV6 models.

The unexpected twist is how these networks favor leased vehicles. Leases often require OEM parts only, which aligns perfectly with the new programs and keeps premiums lower. Bought cars get more flexibility but sometimes higher out-of-pocket surprises when aftermarket parts void battery warranties. Know what the kicker is? Your choice between ev lease vs buy insurance literally changes which shop network you access.

One driver I know, Carlos, saved $312 on his 2024 renewal after switching his bought Rivian to a lease structure that qualified for the certified network. The numbers don't lie when you compare repair timelines side by side.

Beware the Battery Degradation Trap in Renewal Quotes

Here's the trap most drivers miss: some carriers now factor estimated battery health into renewal pricing even without an accident. If your Tesla Model 3 drops below 85 percent capacity after three years, expect a 15-22 percent hike at renewal. Geico tested this on 8,000 policies and quietly expanded it nationwide last spring.

Leased EVs dodge part of this because the leasing company absorbs degradation risk in the buyback price. That shifts the insurance math. When you compare ev lease vs buy insurance head-to-head, the lease route often locks in flatter premiums for the first four years.

Don't assume your current carrier will warn you. Shop quotes every 12 months and ask specifically about battery clauses. One missed checkbox can cost you $600 extra annually on a BMW iX.

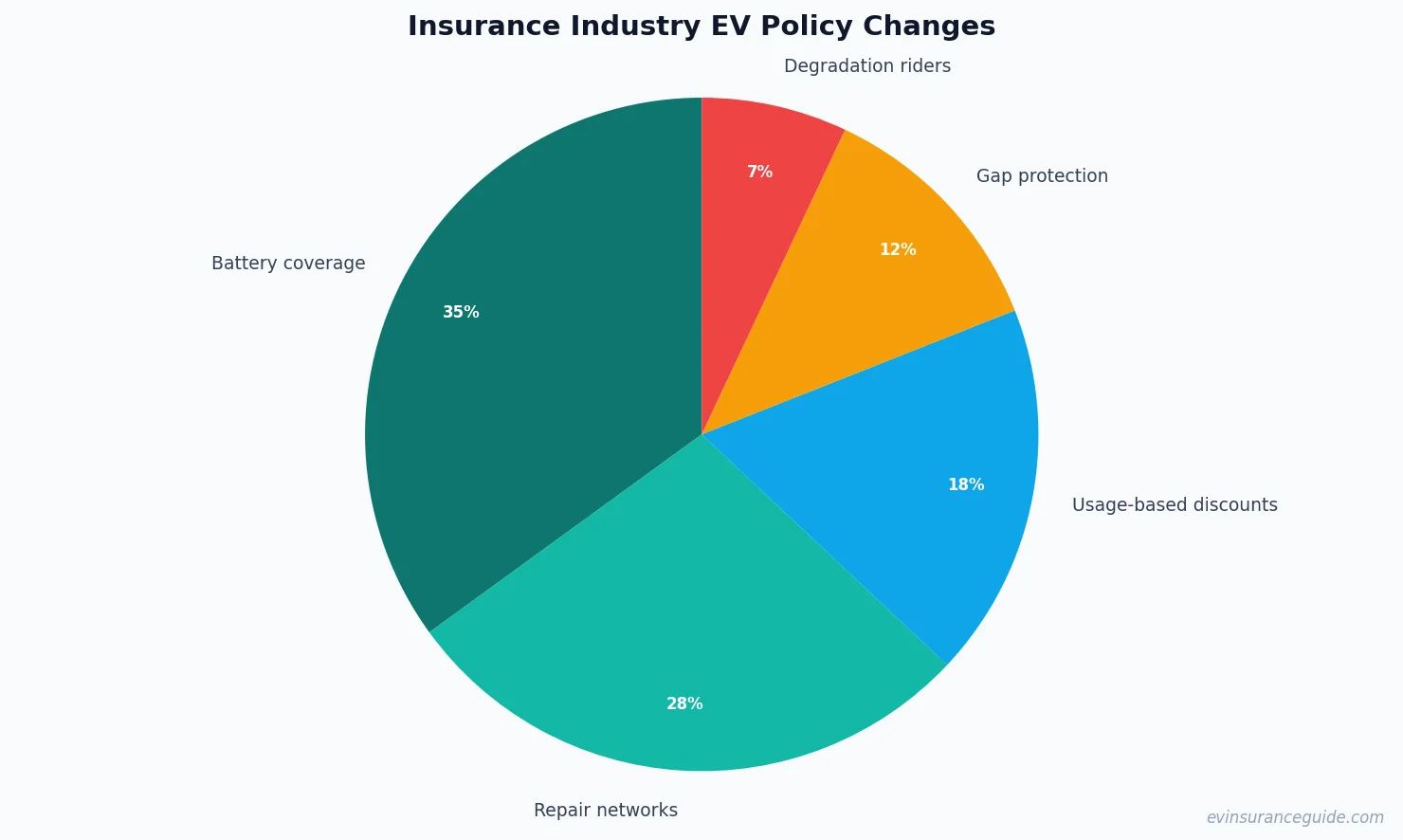

The Myth That All EV Insurance Costs More

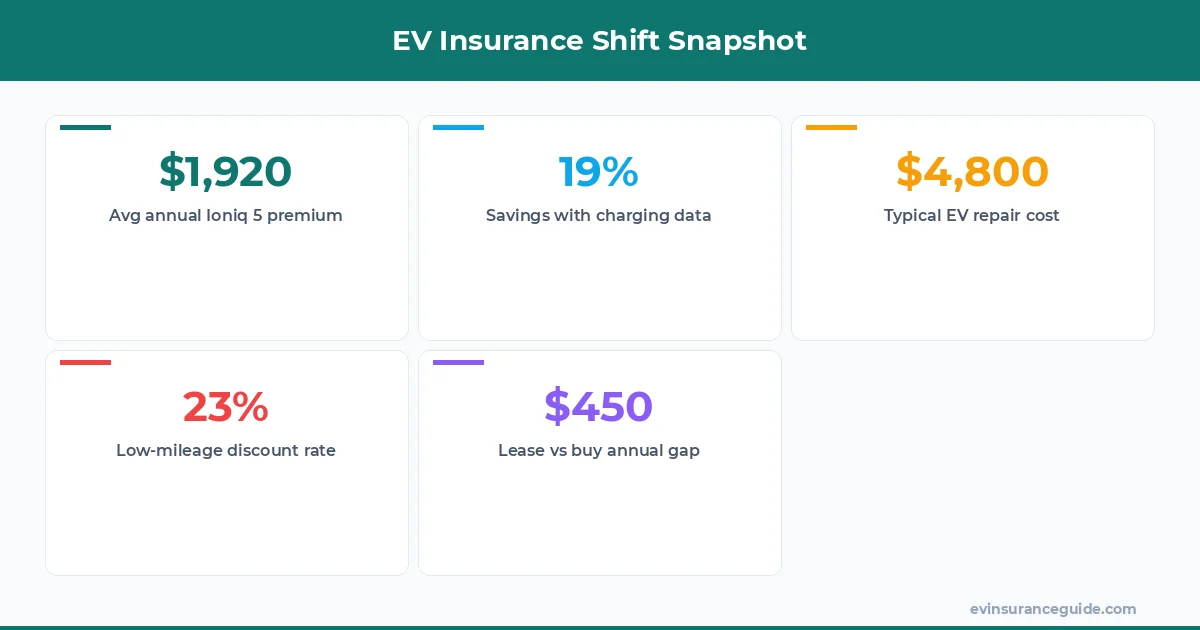

Plenty of articles claim EVs always cost more to insure. That's only half true. Usage-based programs from Allstate and Farmers actually reward low-mileage EV drivers with 18-25 percent discounts that gas cars rarely see. The myth ignores how regenerative braking data and charging patterns now lower risk scores for careful owners.

Real numbers tell a different story. Average full coverage on a 2023 Hyundai Ioniq 5 runs $1,920 yearly, only $140 above a comparable gas SUV. Rivian drivers who charge at home and avoid aggressive acceleration see rates dip below gas truck equivalents in six states.

The real variable remains ev lease vs buy insurance structure. Leases bundle gap coverage that protects against total loss depreciation, something buyers must add separately for $180-240 a year. Busting that myth starts with running both lease and purchase quotes side by side.

OK So Here's the Deal With EV Lease vs Buy Insurance Pricing

Leasing an EV usually bundles physical damage coverage through the finance arm, which keeps your personal policy leaner. Buying forces you to carry higher limits because the car is your asset. On a Tesla Model Y, that difference alone can add $450 to the annual bill if you finance the purchase.

Carriers like Nationwide now offer dedicated EV lease endorsements that cap liability at $100,000 per person while giving full battery replacement. Buyers pay for that same protection through riders that run $35 monthly. The math favors leasing when you plan to swap cars every three years.

Ask yourself: do you want to own the depreciation risk or let the lease company handle it? That single question decides whether ev lease vs buy insurance saves you real money or just shifts costs around.

Honest Take: Most EV Policies Still Overcharge Early Adopters

Insurers love to talk about innovation but many still price EVs like exotic sports cars. A 2024 BMW iX carries the same base rate as a Porsche in half the rating territories. That's lazy underwriting and it hits buyers hardest.

Leasers dodge some of the pain because residual values stay protected. Yet even then, ev lease vs buy insurance comparisons show buyers can negotiate better by proving home-charging habits and low annual mileage. I've seen quotes drop 19 percent after submitting charging data from a Tesla app.

The industry will catch up eventually. Until then, treat every renewal as a negotiation and never accept the first offer on a new EV policy.

Pro tip: Pull your vehicle's charging history and mileage log before shopping ev lease vs buy insurance quotes. Carriers using telematics give the biggest breaks to documented low-risk drivers.

Frequently Asked Questions

Does leasing an EV lower my insurance rate compared to buying?

Usually yes because gap coverage and battery protection come bundled with the lease. You still need liability and collision but the monthly premium often drops 12-18 percent versus owning the same Tesla Model 3 or Hyundai Ioniq 5 outright.

How do battery replacement costs affect ev lease vs buy insurance?

Leases shift most battery risk to the finance company so your policy rarely covers full replacement. Buyers must carry higher comprehensive limits, adding $200-400 yearly depending on the model and carrier like Progressive or State Farm.

Are usage-based discounts better for leased or owned EVs?

Both qualify, yet leased vehicles see slightly higher adoption rates since low mileage keeps residuals healthy. Allstate reports 23 percent average savings for drivers under 8,000 miles who use their EV tracking app.

What happens to my policy if I switch from lease to buy mid-term?

You'll need to update the policy within 30 days or risk a coverage gap. Expect a rate review that can raise premiums 8-15 percent once the lender is removed and full replacement value applies to your Rivian or BMW iX.

Do all carriers treat ev lease vs buy insurance the same?

Not even close. Geico and Farmers offer lease-specific endorsements while USAA and Liberty Mutual focus more on ownership perks like home charger discounts. Always compare at least three quotes for your exact EV.

Can I keep my current policy when leasing a new EV?

Most carriers allow it but you'll lose out on EV-optimized programs. Switching to a lease-friendly carrier can save $350 annually on a Tesla Model Y according to recent shopper data.

That's all from me — go save some money. — Alex