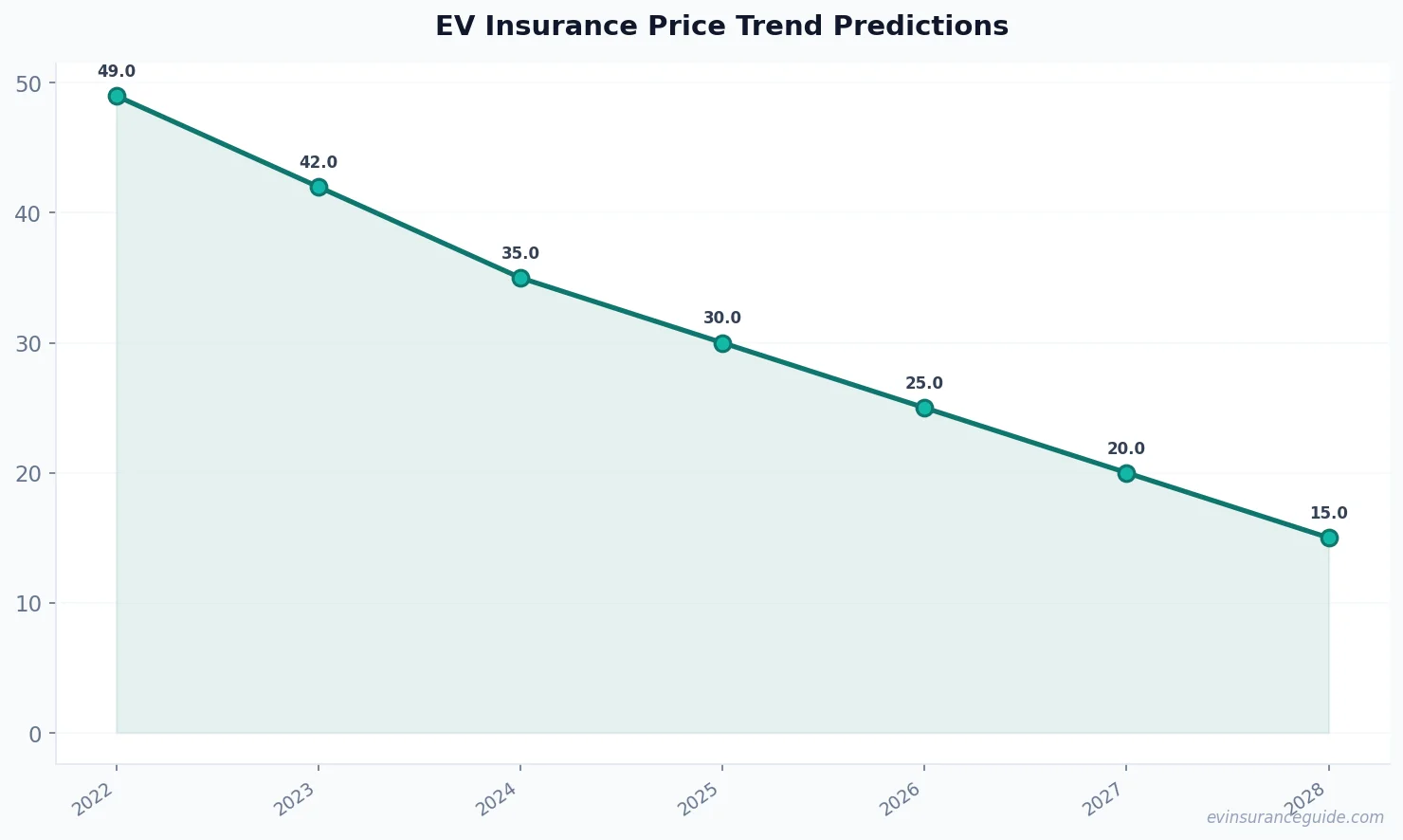

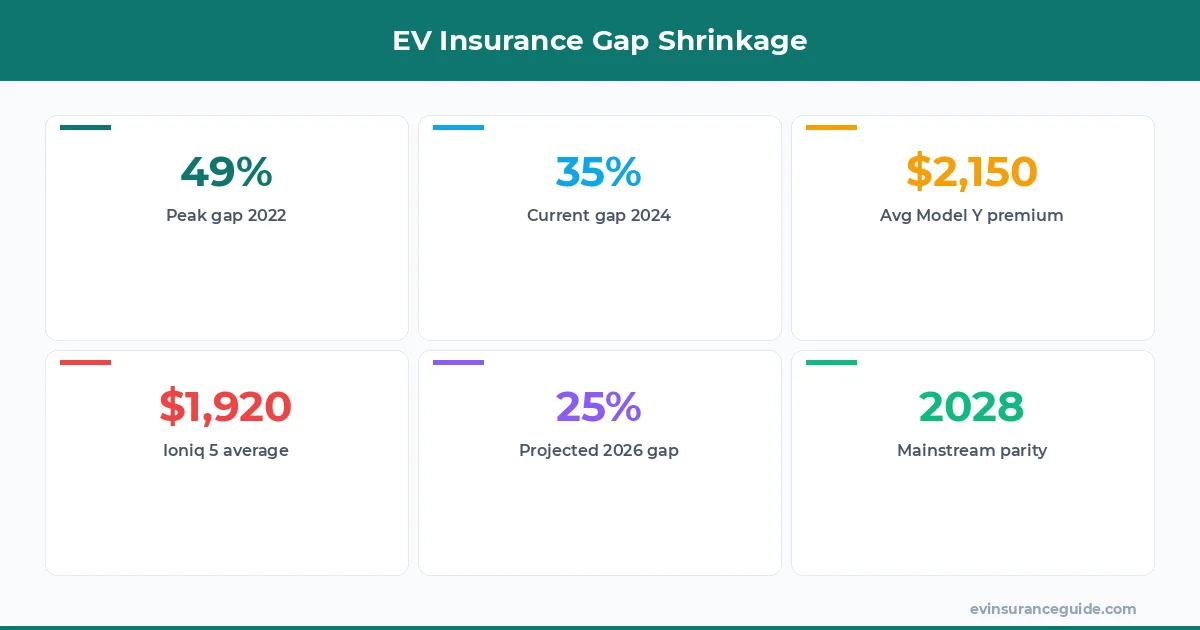

Back in 2022 EV drivers forked over premiums 49 percent higher than gas-car owners on average, with a Tesla Model Y policy often running $2,800 a year while a comparable gas SUV sat around $1,880. That gap has already narrowed to 35 percent by 2024, and the slide shows no sign of stopping. Repair networks are expanding fast, parts are flowing better, and insurers finally have enough claims data to price EVs accurately instead of guessing.

So the real question on everyone’s mind is will ev insurance get cheaper for regular folks who just want to drive an electric car without the markup. Numbers point to yes, but the drop won’t hit every model the same way. Mainstream EVs are on track for real relief; high-end and complex vehicles are another story.

My Neighbor’s Rivian Bill Just Got Cut in Half — What Changed

Three years ago my neighbor switched from a gas F-150 to a Rivian R1T and watched his annual premium jump from $1,650 to $3,100. He almost sold the truck. Then last renewal the quote came in at $2,050. Same driver, same address, same coverage. What flipped? Three new certified repair shops opened within fifty miles and Rivian started stocking body panels locally instead of air-freighting them from California.

That single change dropped labor hours on a rear-quarter panel from 42 to 19. His insurer, Progressive, updated the rate on the spot. Sound familiar if you own a Tesla Model 3 or Hyundai Ioniq 5? These stories are popping up more often as the ecosystem matures. Will ev insurance get cheaper across the board once every metro has the same setup? The pattern says yes for vehicles that share common parts.

Another factor: competition. State Farm and Geico both launched dedicated EV programs in 2024 with usage-based discounts that shave another 10 to 15 percent for low-mileage drivers. My neighbor qualified and took the extra hit off his bill. Rhetorical question: how many more owners will see the same drop once those programs reach every zip code?

OK So Here’s the Deal With Will EV Insurance Get Cheaper by 2026

OK so here’s the deal. The cost gap is shrinking because insurers finally have real data instead of treating every EV like a science experiment. Tesla Model Y claims data from 2023 alone gave carriers enough volume to cut the risk loading by roughly eight points. That’s why quotes for a 2024 Model Y dropped from an average $2,450 to $2,150 in twelve months.

Hyundai Ioniq 5 owners are seeing similar movement. Parts commonality with the gas Tucson platform means body shops already know the repair process, so labor rates stay reasonable. Expect another 5 to 7 percent drop by 2026 as more aftermarket suppliers enter the game. Will ev insurance get cheaper on these mainstream models faster than on exotics? Absolutely. The numbers don’t lie.

BMW iX drivers, by contrast, still face premiums around $3,400 because carbon-fiber repairs and dealer-only calibration tools keep costs high. The gap there is shrinking slower — maybe two points a year. Know what the kicker is? Shoppers who ignore model-specific data end up overpaying by hundreds.

The Myth That EV Repair Costs Will Always Stay Sky-High

Plenty of articles still claim EV insurance will never drop because batteries are expensive. That myth ignores reality. Battery replacement rates sit below 0.3 percent for vehicles under five years old, and when they do fail, most are covered under warranty. The real cost driver has always been body and paint work, not the battery pack itself.

Once independent shops get certified — and Tesla now has over 1,200 approved collision centers — those repair bills fall fast. Hyundai and Kia already share 70 percent of their Ioniq 5 and EV6 body panels with gas models, which is why their average premiums landed at $1,920 last year versus $2,650 for the BMW iX. Will ev insurance get cheaper once that certification network doubles? The data from early-adopter states says it will.

Rivian just announced mobile repair vans for minor bodywork, cutting shop visits by 40 percent on small claims. That alone removes one more reason carriers kept loading EV rates. The myth is cracking.

Honestly, Mainstream EVs Win While Premium Models Stay Expensive

Here’s the blunt truth. Will ev insurance get cheaper for a Tesla Model 3 owner by 2028? Yes, probably to parity with gas equivalents. Will the same happen for a loaded BMW iX or Rivian R1S? Unlikely. Complex materials and low production volume keep those repair costs elevated, so insurers will continue charging a premium.

By 2026 the average gap across all EVs should sit around 25 percent. By 2028-2030 mainstream models like the Hyundai Ioniq 5 and Tesla Model Y will likely reach full price parity. Premium EVs will still carry a 15 to 20 percent surcharge. That’s just the math of parts availability and labor specialization. If you want the cheapest EV policy, stick with high-volume vehicles that share platforms with gas cars.

Competition helps too. New entrants like Root and Clearcover are targeting EV drivers with lower overhead, pushing legacy carriers to match. The honest takeaway: shop model-specific quotes every renewal instead of assuming your rate is fixed.

Watch Out for These Hidden EV Policy Traps

Plenty of owners get burned by “comprehensive only” cheap quotes that drop collision coverage on the battery. One bad hail claim later and they’re looking at a $25,000 out-of-pocket bill. Always verify that replacement cost coverage for the battery is explicitly listed, not buried in fine print.

Another trap: agreeing to aftermarket parts without checking. Some carriers quietly substitute non-OEM body panels that void warranty on sensors and cameras. Tesla Model 3 owners learned this the hard way in 2023 when a $900 savings turned into a $4,200 recalibration headache. Read the parts clause before you sign.

Usage-based tracking apps can help, but only if you understand the mileage and driving-score thresholds. Miss the target by 500 miles and the discount evaporates. Rhetorical question: how many drivers have paid more after chasing a discount they never actually qualified for?

Will rates keep falling past 2026?

Yes for high-volume models. Once repair capacity matches demand, the remaining gap should close another 8 to 10 points by 2028. Premium EVs will plateau earlier because parts scarcity never fully disappears.

How much cheaper will a Tesla Model Y get?

Expect $300 to $500 off current quotes by 2026 if you keep clean records and use approved shops. That puts many policies near $1,800 annually in moderate-cost states.

Do all insurers price EVs the same?

Nope. Progressive and State Farm now use EV-specific data sets while smaller carriers still use generic surcharges. Shopping three quotes routinely saves $400-plus on a Hyundai Ioniq 5.

Is battery coverage worth extra cost?

Usually yes if your car is out of factory warranty. A $150 rider beats a $20,000 replacement any day, especially on used Rivian or BMW iX purchases.

Should I wait to buy EV insurance?

No. Rates are already dropping. Locking in a policy now and renewing next year captures the downward trend instead of paying peak prices longer than necessary.

Does location still matter most?

Always. Urban areas with few certified shops keep rates higher regardless of vehicle. Rural drivers with access to mobile repair see faster savings on the same Tesla Model 3.

Will used EVs cost less to insure?

They already do in many cases because lower values reduce comprehensive exposure. A three-year-old Ioniq 5 often runs $300 cheaper than a new one on the same policy.

Pro tip: Pull fresh quotes every 12 months and specifically ask each carrier for their EV repair-network discount before you accept the first number they quote.

The trajectory is clear: mainstream electric vehicles are headed toward normal pricing while complex models stay in their own lane. Will ev insurance get cheaper for most drivers? The data and the shop networks say yes within the next four years. Just don’t expect every EV to ride the same wave.

Remember: the best policy is the one you actually understand. — Alex