Are you aware that your credit score can increase your electric vehicle insurance rates by up to 200%? Yep, it's a thing. Most drivers don't even think about it when shopping for gap insurance for electric cars. Sound familiar? You're not alone. I've seen it time and time again - people focusing on the sticker price of their new Tesla Model 3 or Hyundai Ioniq 5, without considering the long-term costs of insurance. Know what the kicker is? Your credit score can make or break your insurance rates.

WARNING — The Credit Score Trap

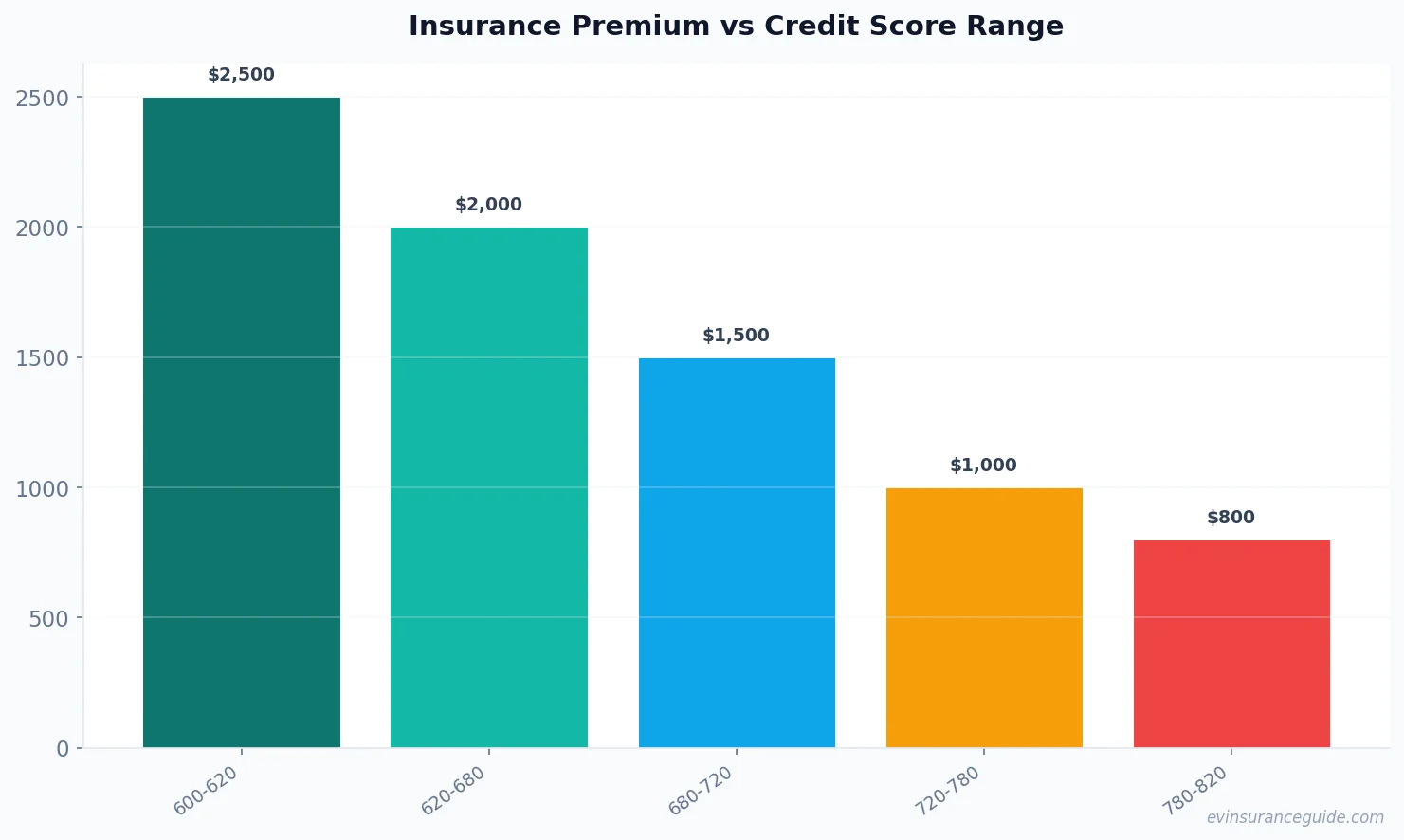

Don't get caught off guard by the credit score trap. It's a hidden cost factor that can sneak up on you. Let's say you've got a credit score of 620, which is considered fair. You're looking to insure your brand new Rivian R1T, and you're quoted $1,800 per year. Not bad, right? But, if your credit score was 780, you'd be looking at a quote of around $1,200 per year. That's a difference of $600. And, if you've got a poor credit score, say 500, you're looking at a quote of over $3,000 per year. Ouch. That one stung.

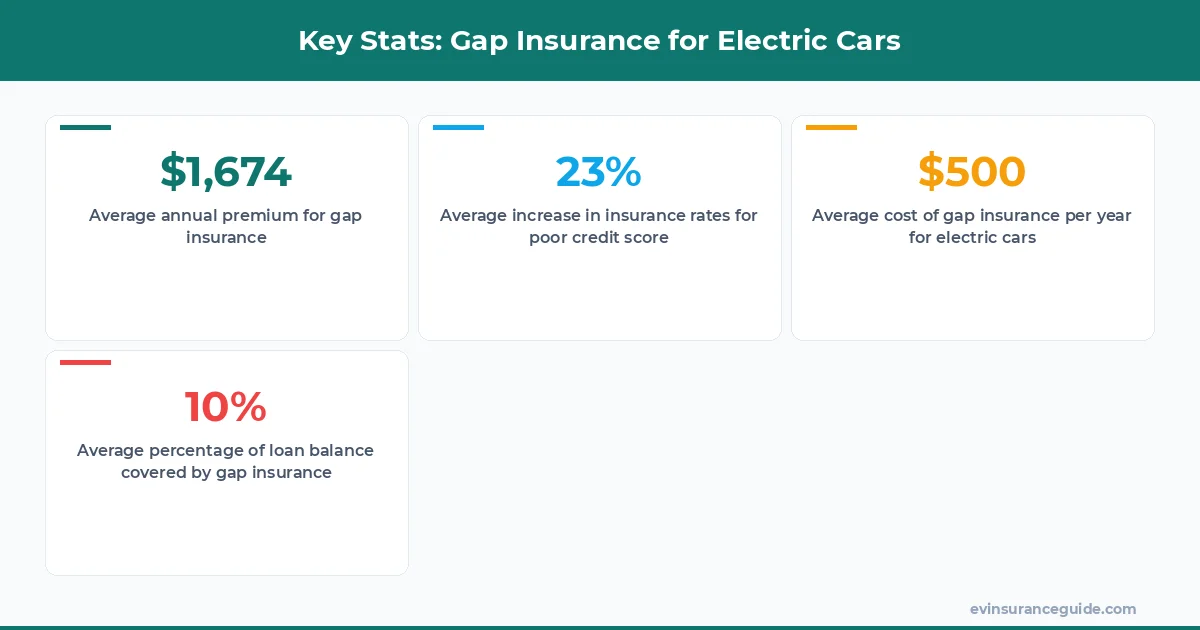

It's not just about the initial quote, either. Your credit score can also impact your gap insurance premiums. Gap insurance for electric cars is designed to cover the difference between the actual cash value of your vehicle and the amount you still owe on your loan or lease. If you've got a poor credit score, you can expect to pay more for this type of insurance. For example, let's say you've got a Tesla Model Y with a loan balance of $40,000. If you've got a good credit score, you might pay around 5% of your annual premium for gap insurance. But, if you've got a poor credit score, you might pay 10% or more. That's an extra $200 to $400 per year.

We've seen cases where drivers have been quoted over $2,000 per year for gap insurance for electric cars, simply because of their credit score. It's not fair, but it's the reality. And, it's not just about the cost - it's also about the hassle. If you've got a poor credit score, you might find it harder to get approved for insurance in the first place. Wild, right?

HONEST_OPINION — The Gap Insurance Premium Rip-Off

Let's be real - some gap insurance premiums for electric cars are just plain ridiculous. I've seen quotes of over $1,500 per year for a BMW iX, just because the driver had a credit score of 580. That's just not right. Gap insurance should be there to protect you, not rip you off. And, it's not just about the cost - it's also about the value. If you've got a good credit score, you might be able to negotiate a better rate for your gap insurance. But, if you've got a poor credit score, you're at the mercy of the insurance company.

I'm not saying that all gap insurance premiums for electric cars are bad. There are some good options out there, like the ones offered by companies like GEICO and Progressive. They offer competitive rates and flexible payment plans. But, you've got to do your research and shop around. Don't just accept the first quote you get. You might be surprised at how much you can save.

For example, let's say you've got a Hyundai Ioniq 5 with a loan balance of $30,000. You've got a good credit score of 720, and you're looking for gap insurance. You might get quoted around $400 per year from one company, but another company might quote you $600 per year. That's a difference of $200 per year. It's worth shopping around, trust me.

STORY_TEASE — A Real-Life Example

I've got a friend, let's call him Dave, who recently purchased a Tesla Model 3. He's got a good credit score of 780, but he didn't realize the impact it would have on his insurance rates. He was quoted $1,200 per year for his insurance, which seemed reasonable. But, when he added gap insurance to his policy, his rates increased by $300 per year. He was shocked. He didn't realize that his credit score would affect his gap insurance premiums so much. He's now shopping around for a better deal, but it's a hassle.

It's not just about the cost, either. Dave's also worried about the impact on his credit score. He's heard that multiple insurance quotes can hurt your credit score, so he's trying to be careful. It's a Catch-22 - you need to shop around to get the best rate, but shopping around can hurt your credit score. Know what I mean?

A pro tip: always check your credit score before shopping for insurance. You can get a free credit report from the three major credit bureaus once a year. It's worth it to make sure your credit score is accurate and up-to-date.

QUESTION — Can You Afford the Gap Insurance Premiums?

Can you really afford the gap insurance premiums for your electric car? It's a question worth asking. Let's say you've got a Rivian R1T with a loan balance of $60,000. You've got a good credit score of 780, but you're still quoted $1,000 per year for gap insurance. That's a lot of money. You've got to consider whether it's worth it.

For example, let's say you've got a budget of $500 per month for your car expenses. That includes your loan payment, insurance, and maintenance. If you've got to add $83 per month for gap insurance, that's a big chunk of change. You've got to prioritize your spending and make sure you can afford it.

COMPARISON — Gap Insurance for Electric Cars vs. Gas-Powered Cars

Gap insurance for electric cars is often more expensive than gap insurance for gas-powered cars. It's because electric cars tend to depreciate faster than gas-powered cars. For example, let's say you've got a Tesla Model Y and a Toyota Camry. Both cars are worth around $40,000. But, after three years, the Tesla Model Y might be worth around $25,000, while the Toyota Camry might be worth around $30,000. That's a big difference.

It's not just about the depreciation, either. Electric cars also tend to have higher insurance rates in general. It's because they're still a relatively new technology, and there's not as much data on them. But, that's changing. More and more insurance companies are starting to offer competitive rates for electric cars. It's worth shopping around to find the best deal.

And, let's not forget about the benefits of gap insurance for electric cars. It can provide peace of mind and protect you from financial loss if your car is totaled or stolen. It's worth considering, especially if you've got a high loan balance or a poor credit score.

FAQs

What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of your vehicle and the amount you still owe on your loan or lease. It's designed to protect you from financial loss if your car is totaled or stolen.

How much does gap insurance for electric cars cost?

The cost of gap insurance for electric cars varies depending on your credit score, loan balance, and other factors. On average, you can expect to pay around 5% to 10% of your annual premium for gap insurance. For example, if your annual premium is $1,200, you might pay around $60 to $120 per year for gap insurance.

Can I get gap insurance for my used electric car?

Yes, you can get gap insurance for your used electric car. However, the cost might be higher than for a new car. It's because used cars tend to depreciate faster than new cars. You might be able to negotiate a better rate if you've got a good credit score and a low loan balance.

How does my credit score affect my gap insurance premiums?

Your credit score can significantly impact your gap insurance premiums. If you've got a good credit score, you might be able to negotiate a better rate. But, if you've got a poor credit score, you might pay more for gap insurance. It's because insurance companies see you as a higher risk.

Can I cancel my gap insurance policy at any time?

Yes, you can cancel your gap insurance policy at any time. However, you might be subject to a cancellation fee. It's worth checking your policy documents to see what the terms are.

Is gap insurance for electric cars worth it?

Gap insurance for electric cars can be worth it if you've got a high loan balance or a poor credit score. It can provide peace of mind and protect you from financial loss if your car is totaled or stolen. However, if you've got a low loan balance and a good credit score, you might not need it.

Well, actually, the decision to get gap insurance for your electric car depends on your individual circumstances. You've got to weigh the costs and benefits and make an informed decision. It's not a one-size-fits-all solution.

OK wait, scratch that — the most important thing is to do your research and shop around. Don't just accept the first quote you get. You might be surprised at how much you can save. And, remember to always check your credit score before shopping for insurance. It's worth it to make sure your credit score is accurate and up-to-date.

Stay charged and stay covered! — Alex