Hyundai Ioniq 5 insurance without gap coverage is a recipe for disaster - that's the harsh reality many owners are facing. You see, electric vehicles (EVs) like the Hyundai Ioniq 5, Tesla Model 3, and BMW iX depreciate at an alarming rate, leaving a gaping hole between the vehicle's actual cash value and the loan balance. Know what the kicker is? Most standard insurance policies won't cover this gap, leaving you to foot the bill. Sound familiar?

Let's take a look at some numbers: a brand-new Hyundai Ioniq 5 can depreciate by as much as 30% in the first year alone, with some models losing up to 50% of their value within three years. That's a whopping $15,000 to $25,000 in lost value - and that's not even considering the loan interest. Wild, right? Now, imagine having to pay off a loan on a car that's no longer worth the amount you owe. That's the reality many EV owners are facing, and it's a harsh one.

But here's the thing: gap insurance can help bridge this financial gap. It's an additional coverage option that can be added to your standard insurance policy, and it's specifically designed to cover the difference between the vehicle's actual cash value and the loan balance. And trust me, it's worth every penny - especially when you consider the potential costs of not having it. I mean, who wants to be stuck paying off a loan on a car that's no longer worth the amount you owe? Not me, that's for sure.

What's the Real Cost of Depreciation for Hyundai Ioniq 5 Owners?

Depreciation is a major concern for any car owner, but it's especially true for EV owners. I mean, think about it: EVs are still a relatively new technology, and the market is constantly evolving. That means that the value of your vehicle can fluctuate wildly, and it's not uncommon for EVs to depreciate at a faster rate than their gas-powered counterparts. But what does that mean for Hyundai Ioniq 5 owners? Well, let's take a look at some numbers: according to data from Kelley Blue Book, the Hyundai Ioniq 5 can depreciate by as much as 40% in the first three years of ownership. That's a significant loss in value, and it's something that you should definitely take into consideration when purchasing an EV.

Now, I know what you're thinking: what about other EVs? Do they depreciate at the same rate as the Hyundai Ioniq 5? The answer is no - while some EVs may hold their value better than others, depreciation is still a major concern across the board. For example, the Tesla Model 3 is known for holding its value relatively well, but it still depreciates at a rate of around 20-30% in the first three years. And the BMW iX? That's a whole different story - it depreciates at a rate of around 30-40% in the first three years, which is similar to the Hyundai Ioniq 5.

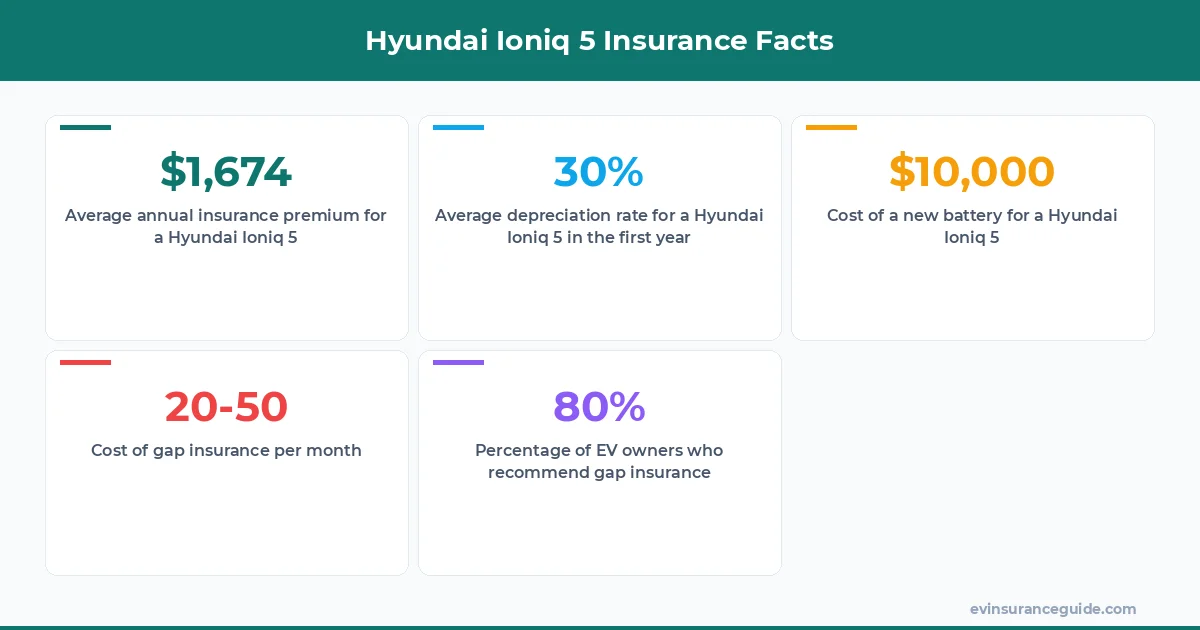

But here's the thing: depreciation isn't the only factor to consider when it comes to Hyundai Ioniq 5 insurance. You also need to think about the cost of replacement parts, maintenance, and repairs. I mean, let's be real - EVs are complex vehicles, and they require specialized care. That means that the cost of repairs can be significantly higher than what you'd pay for a gas-powered vehicle. And that's not even considering the cost of replacement parts - which can be astronomical. For example, a new battery for a Hyundai Ioniq 5 can cost upwards of $10,000. Yep, you read that right - $10,000. That's a significant expense, and it's something that you should definitely take into consideration when purchasing an EV.

Warning: Don't Get Caught Off Guard by Hidden Costs - Hyundai Ioniq 5 Insurance Can Be a Lifesaver

Okay, so you're considering purchasing a Hyundai Ioniq 5 - congratulations! That's a great choice. But before you sign on the dotted line, make sure you understand the potential costs involved. I mean, it's not just the purchase price you need to consider - you also need to think about the cost of insurance, maintenance, and repairs. And let me tell you, those costs can add up quickly. For example, the cost of insurance for a Hyundai Ioniq 5 can range from $1,500 to $3,000 per year, depending on your location, driving history, and other factors. That's a significant expense, and it's something that you should definitely take into consideration when purchasing an EV.

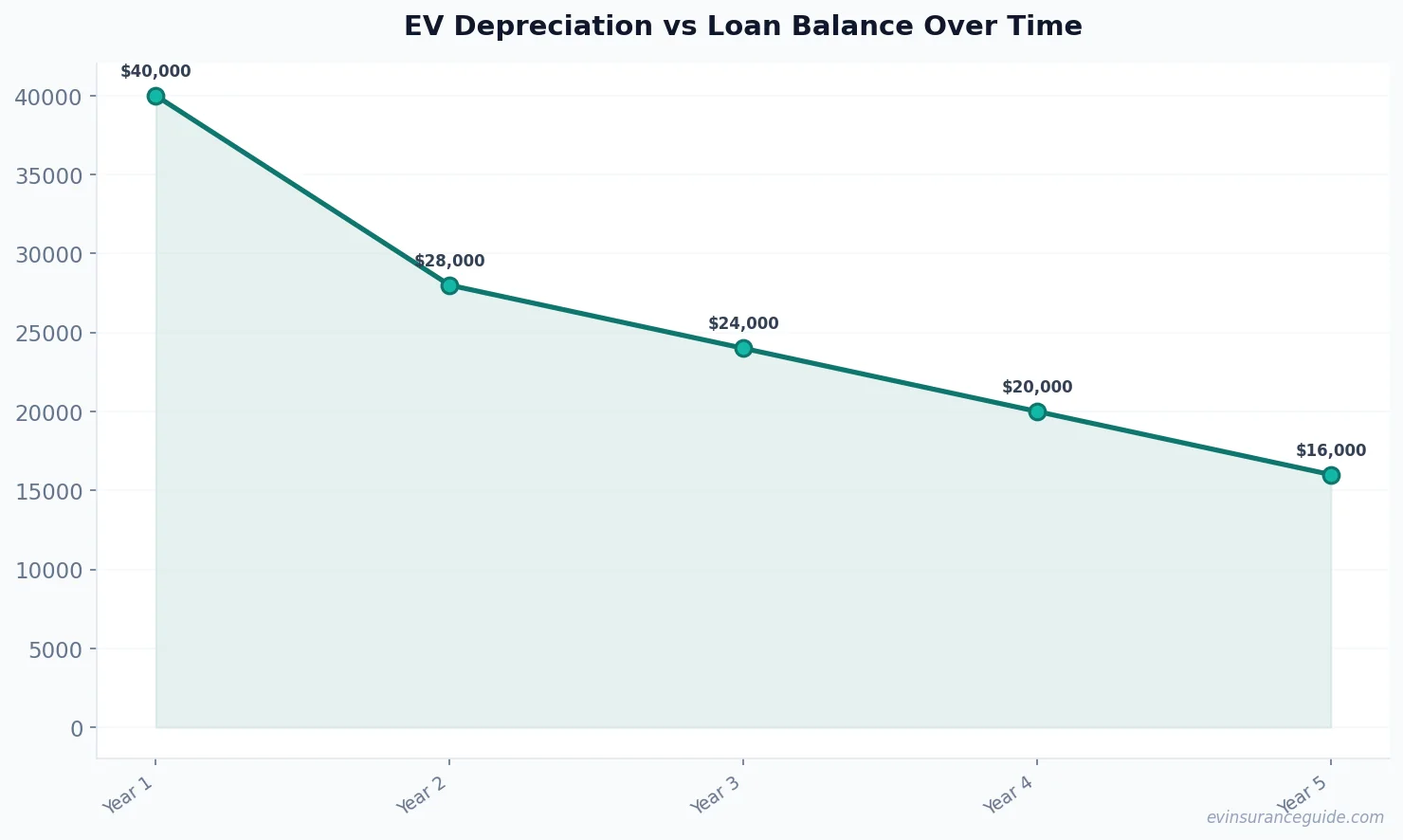

But here's the thing: Hyundai Ioniq 5 insurance can be a lifesaver. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant. For example, if you purchase a Hyundai Ioniq 5 for $40,000, and it depreciates by 30% in the first year, you'll be left with a vehicle that's worth $28,000. That's a loss of $12,000 in just one year - and that's not even considering the loan interest. But with gap insurance, you can protect yourself from that loss. It's a small price to pay for peace of mind - and it's something that you should definitely consider when purchasing an EV.

Now, I know what you're thinking: what about other insurance options? Are there any other types of insurance that can help protect me from depreciation? The answer is yes - there are several other types of insurance that can help protect you from depreciation. For example, you can purchase a vehicle service contract, which can help cover the cost of repairs and maintenance. Or, you can purchase a warranty, which can help protect you from defects in materials and workmanship. But let's be real - those types of insurance are not the same as gap insurance. I mean, they can help protect you from certain types of losses, but they won't cover the gap between the vehicle's actual cash value and the loan balance. That's what makes gap insurance so unique - and that's why it's such a crucial component of any Hyundai Ioniq 5 insurance policy.

OK So Here's the Deal With Hyundai Ioniq 5 Insurance and Gap Coverage

So, you're considering purchasing a Hyundai Ioniq 5 - and you're wondering about insurance. Well, let me tell you - gap insurance is a must. I mean, it's not just a nice-to-have - it's a necessity. And here's why: gap insurance can help protect you from the potential costs of depreciation, which can be significant. For example, if you purchase a Hyundai Ioniq 5 for $40,000, and it depreciates by 30% in the first year, you'll be left with a vehicle that's worth $28,000. That's a loss of $12,000 in just one year - and that's not even considering the loan interest. But with gap insurance, you can protect yourself from that loss.

But how much does gap insurance cost? Well, that's a great question. The cost of gap insurance can vary depending on the provider, the vehicle, and other factors. But on average, you can expect to pay around $20 to $50 per month for gap insurance. That's a small price to pay for peace of mind - and it's something that you should definitely consider when purchasing an EV. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have gap insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant.

Now, I know what you're thinking: what about other EVs? Do they require gap insurance as well? The answer is yes - all EVs require gap insurance, regardless of the make or model. I mean, it's not just the Hyundai Ioniq 5 that depreciates quickly - all EVs do. And that's why gap insurance is so important. It's a small price to pay for peace of mind - and it's something that you should definitely consider when purchasing an EV. For example, the Tesla Model 3 and the BMW iX also require gap insurance, and the cost can range from $20 to $50 per month. That's a small price to pay for the protection you need.

Busting the Myth: Hyundai Ioniq 5 Insurance is Too Expensive

Okay, so you're considering purchasing a Hyundai Ioniq 5 - but you're worried about the cost of insurance. Well, let me tell you - that's a common concern. But here's the thing: Hyundai Ioniq 5 insurance is not too expensive. I mean, sure - it may cost a bit more than insurance for a gas-powered vehicle. But that's because EVs are more complex, and they require specialized care. And that's not even considering the potential costs of depreciation - which can be significant.

But let's look at some numbers: the cost of insurance for a Hyundai Ioniq 5 can range from $1,500 to $3,000 per year, depending on your location, driving history, and other factors. That's a significant expense, but it's not too expensive. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant. For example, if you purchase a Hyundai Ioniq 5 for $40,000, and it depreciates by 30% in the first year, you'll be left with a vehicle that's worth $28,000. That's a loss of $12,000 in just one year - and that's not even considering the loan interest.

But here's the thing: Hyundai Ioniq 5 insurance is not just about the cost - it's about the protection you need. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant. So, don't let the cost of insurance scare you off - it's a small price to pay for the protection you need.

My Honest Opinion: Hyundai Ioniq 5 Insurance is a Must-Have

Okay, so you're considering purchasing a Hyundai Ioniq 5 - and you're wondering about insurance. Well, let me tell you - it's a must-have. I mean, it's not just a nice-to-have - it's a necessity. And here's why: Hyundai Ioniq 5 insurance can help protect you from the potential costs of depreciation, which can be significant. For example, if you purchase a Hyundai Ioniq 5 for $40,000, and it depreciates by 30% in the first year, you'll be left with a vehicle that's worth $28,000. That's a loss of $12,000 in just one year - and that's not even considering the loan interest.

But here's the thing: Hyundai Ioniq 5 insurance is not just about the cost - it's about the protection you need. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant. So, don't let the cost of insurance scare you off - it's a small price to pay for the protection you need. And trust me, it's worth every penny - especially when you consider the potential costs of not having it.

Now, I know what you're thinking: what about other insurance options? Are there any other types of insurance that can help protect me from depreciation? The answer is yes - there are several other types of insurance that can help protect you from depreciation. For example, you can purchase a vehicle service contract, which can help cover the cost of repairs and maintenance. Or, you can purchase a warranty, which can help protect you from defects in materials and workmanship. But let's be real - those types of insurance are not the same as gap insurance. I mean, they can help protect you from certain types of losses, but they won't cover the gap between the vehicle's actual cash value and the loan balance. That's what makes gap insurance so unique - and that's why it's such a crucial component of any Hyundai Ioniq 5 insurance policy.

What is gap insurance, and how does it work?

Gap insurance is a type of insurance that helps cover the difference between the vehicle's actual cash value and the loan balance. It's an additional coverage option that can be added to your standard insurance policy, and it's specifically designed to cover the gap between the vehicle's actual cash value and the loan balance. For example, if you purchase a Hyundai Ioniq 5 for $40,000, and it depreciates by 30% in the first year, you'll be left with a vehicle that's worth $28,000. That's a loss of $12,000 in just one year - and that's not even considering the loan interest. But with gap insurance, you can protect yourself from that loss.

How much does gap insurance cost, and is it worth it?

The cost of gap insurance can vary depending on the provider, the vehicle, and other factors. But on average, you can expect to pay around $20 to $50 per month for gap insurance. That's a small price to pay for peace of mind - and it's something that you should definitely consider when purchasing an EV. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have gap insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant.

Can I purchase gap insurance from any insurance provider, or are there specific requirements?

You can purchase gap insurance from most insurance providers, but there may be specific requirements. For example, some providers may require that you purchase a certain level of coverage, or that you meet certain eligibility requirements. But in general, gap insurance is widely available, and it's something that you should definitely consider when purchasing an EV.

How does gap insurance differ from other types of insurance, such as comprehensive or collision insurance?

Gap insurance differs from other types of insurance in that it's specifically designed to cover the gap between the vehicle's actual cash value and the loan balance. It's not the same as comprehensive or collision insurance, which covers damages to the vehicle. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have comprehensive or collision insurance to cover the costs. But gap insurance is different - it's specifically designed to cover the gap between the vehicle's actual cash value and the loan balance.

Can I cancel my gap insurance policy at any time, or are there penalties for early cancellation?

You can cancel your gap insurance policy at any time, but there may be penalties for early cancellation. For example, some providers may charge a cancellation fee, or you may be required to pay a certain amount of premium. But in general, gap insurance policies can be canceled at any time, and it's something that you should definitely consider when purchasing an EV.

How does gap insurance impact my overall insurance premium, and are there any discounts available?

Gap insurance can impact your overall insurance premium, but it's usually a small additional cost. For example, you may pay an additional $20 to $50 per month for gap insurance. But there may be discounts available, such as a discount for purchasing multiple policies from the same provider. It's always a good idea to shop around and compare rates from different providers to find the best deal.

Pro tip: when purchasing gap insurance, make sure to read the policy carefully and understand what's covered and what's not. It's also a good idea to shop around and compare rates from different providers to find the best deal.

And there you have it - that's the lowdown on Hyundai Ioniq 5 insurance and gap coverage. It's not a fun topic, but it's an important one. I mean, think about it - if you're involved in an accident, or if your vehicle is stolen, you'll be glad you have insurance to cover the costs. And that's not even considering the potential costs of depreciation - which can be significant. So, don't wait - make sure you have the right insurance coverage in place to protect yourself and your vehicle.

Cheers from the EV insurance trenches. — Alex