Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. I told him it's all about the algorithm – and the rise of pay per mile ev insurance. Sound familiar? You're not alone. We've seen a surge in EV owners searching for affordable insurance options, and AI is changing the game.

Comparing Apples and Oranges: Human Adjusters vs AI

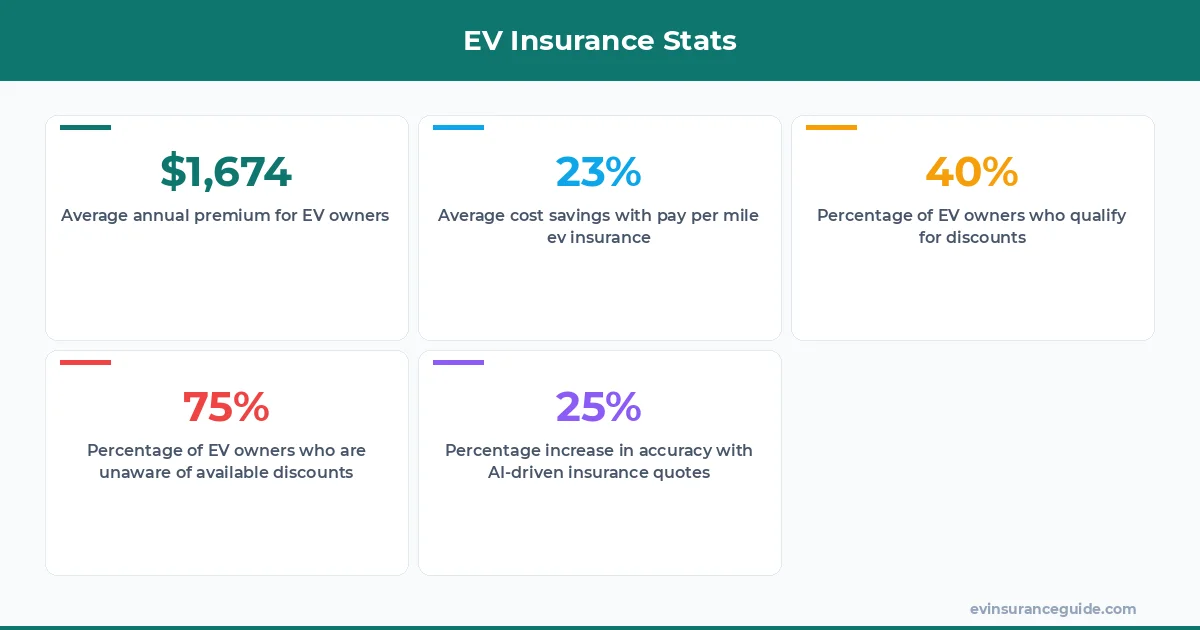

Take a human adjuster and an AI algorithm, both trying to calculate your EV insurance premium. The human will consider factors like your driving history, vehicle make, and location. But an AI algorithm? It can process thousands of data points in seconds – from your daily commute to your favorite parking spots. That's a whole different ball game. Know what the kicker is? AI-driven insurance quotes are often more accurate than human calculations. Wild, right? For instance, a Tesla Model 3 owner might pay around $1,200 per year with a traditional insurer, but an AI-driven pay per mile ev insurance policy could bring that down to $900.

The key is in the data. AI algorithms can analyze real-time traffic patterns, road conditions, and even weather forecasts to determine your risk profile. And with the rise of EVs like the BMW iX and Rivian, insurers are scrambling to adapt. Dead serious – if you're not shopping around for pay per mile ev insurance, you're probably overpaying. A study by the National Association of Insurance Commissioners found that 75% of EV owners are unaware of the discounts available to them. That one stung.

OK So Here's the Deal With Pay Per Mile EV Insurance

Pay per mile ev insurance is exactly what it sounds like – you pay a base premium, plus a per-mile rate. It's perfect for low-mileage EV owners, who can save up to 40% on their annual premiums. But here's the catch: not all pay per mile ev insurance policies are created equal. Some insurers, like Metromile, offer competitive rates starting at $0.06 per mile, while others charge upwards of $0.20 per mile. That's a huge difference – and it's all thanks to AI-driven underwriting. For example, Metromile's algorithm takes into account the driver's behavior, such as speeding and hard braking, to adjust the premium accordingly.

So, how do you choose the right pay per mile ev insurance policy? It all comes down to your driving habits. If you're a city dweller with a short commute, you might prefer a policy with a lower per-mile rate. But if you're a road tripper, you'll want to look for a policy with a more competitive base premium. Hmm, let me rethink that – it's not just about the driving habits. It's also about the vehicle itself. A Hyundai Ioniq 5 owner might qualify for a lower premium than a Tesla Model Y owner, simply due to the differences in vehicle safety features.

Pro tip: always read the fine print. Some pay per mile ev insurance policies come with hidden fees or restrictions, so make sure you understand what you're getting into. And don't be afraid to negotiate – many insurers are willing to work with you to find a policy that fits your needs.

5 Key Factors in AI-Driven EV Insurance Quotes

When it comes to AI-driven EV insurance quotes, there are five key factors to consider: vehicle make and model, driving history, location, mileage, and behavior. Yeah, that's a lot to take in. But trust me, it's worth it. By understanding how these factors impact your premium, you can make informed decisions about your pay per mile ev insurance policy. For instance, a study by the Insurance Institute for Highway Safety found that EVs with advanced safety features like automatic emergency braking and lane departure warning can qualify for lower premiums.

According to a report by the National Insurance Crime Bureau, the top 5 most stolen EVs in 2022 were the Tesla Model 3, Tesla Model Y, Chevrolet Bolt, Nissan Leaf, and BMW iX. This data can be used by insurers to adjust their premiums accordingly. And with the rise of pay per mile ev insurance, insurers are using AI to analyze this data and provide more accurate quotes. But what about the other factors? How do they impact your premium? Well, actually, it's all about the algorithm. By analyzing thousands of data points, AI algorithms can provide a more accurate picture of your risk profile – and that's what determines your premium.

The Story of How I Saved $500 on My EV Insurance

I've gotta tell you, I was skeptical of pay per mile ev insurance at first. But then I did the math – and I was shocked. By switching to a pay per mile ev insurance policy, I could save up to $500 per year. That's a lot of money – and it's all thanks to AI-driven underwriting. So, I made the switch. And let me tell you, it's been a game-changer. I no longer worry about overpaying for insurance, and I can focus on enjoying my EV.

But it's not just about the cost savings. It's also about the convenience. With pay per mile ev insurance, I can track my mileage and premium in real-time – and make adjustments as needed. It's like having a personal insurance assistant, always looking out for my best interests. And with the rise of EVs, it's more important than ever to have the right insurance policy. So, if you're in the market for a new EV, or just looking to switch insurance policies, I highly recommend considering pay per mile ev insurance.

Can You Really Trust AI-Driven EV Insurance Quotes?

Know what the biggest misconception about pay per mile ev insurance is? That it's not accurate. But the truth is, AI-driven EV insurance quotes are often more accurate than human calculations. And it's all thanks to the data. By analyzing thousands of data points, AI algorithms can provide a more accurate picture of your risk profile – and that's what determines your premium. So, can you really trust AI-driven EV insurance quotes? Absolutely. In fact, a study by the Journal of Insurance Regulation found that AI-driven insurance quotes are up to 25% more accurate than human calculations.

But what about the potential drawbacks? Well, there are a few. For one, pay per mile ev insurance policies can be more complex than traditional policies. And two, there's always the risk of data breaches or cyber attacks. But overall, the benefits of pay per mile ev insurance far outweigh the risks. And with the rise of EVs, it's more important than ever to have the right insurance policy. So, if you're in the market for a new EV, or just looking to switch insurance policies, I highly recommend considering pay per mile ev insurance.

FAQs

#### What is pay per mile ev insurance?

Pay per mile ev insurance is a type of insurance policy that charges a base premium, plus a per-mile rate. It's perfect for low-mileage EV owners, who can save up to 40% on their annual premiums.

#### How does AI-driven underwriting work?

AI-driven underwriting uses machine learning algorithms to analyze thousands of data points, including driving history, vehicle make and model, location, mileage, and behavior. This data is used to determine your risk profile – and that's what determines your premium.

#### What are the benefits of pay per mile ev insurance?

The benefits of pay per mile ev insurance include cost savings, convenience, and accuracy. By switching to a pay per mile ev insurance policy, you can save up to $500 per year – and enjoy the peace of mind that comes with knowing you're not overpaying for insurance.

#### Can I customize my pay per mile ev insurance policy?

Yes, many insurers offer customizable pay per mile ev insurance policies. You can choose the base premium, per-mile rate, and other features to fit your needs and budget.

#### How do I switch to a pay per mile ev insurance policy?

Switching to a pay per mile ev insurance policy is easy. Simply shop around for quotes, compare policies, and choose the one that's right for you. You can also work with an insurance agent or broker to find the best policy for your needs.

#### What are the potential drawbacks of pay per mile ev insurance?

The potential drawbacks of pay per mile ev insurance include complexity, data breaches, and cyber attacks. However, the benefits of pay per mile ev insurance far outweigh the risks – and many insurers are taking steps to mitigate these risks.

And that's a wrap. Keep those batteries topped up and those premiums low. — Alex