Meet Sarah, a Tesla Model 3 owner who was paying $2,300 annually for her insurance with State Farm. But after switching to a telematics-based policy with a different provider, her premium dropped to $1,800. That's a $500 savings per year. Know what the kicker is? Her driving habits didn't change - the only difference was the insurer's ability to accurately assess her risk. Wild, right?

OK So Here's the Deal With Telematics Data

Telematics data is revolutionizing the insurance industry, especially for EV owners like Sarah. Companies like Tesla, BMW, and Hyundai are collecting vast amounts of data on their vehicles, from driving habits to charging patterns. This data is then used to create personalized insurance policies, offering discounts to safe drivers and penalizing reckless ones. Take the Hyundai Ioniq 5, for example - its advanced telematics system can track everything from acceleration to braking patterns. That one stung, right? I mean, who doesn't hate being penalized for their driving?

The key to these telematics-based policies is the ability to accurately assess risk. Traditional insurers rely on general demographics and driving history, but telematics data provides a much more nuanced picture. For instance, a study by the National Association of Insurance Commissioners found that telematics-based policies can reduce premiums by up to 20% for safe drivers. Sound familiar? It should - we've all heard stories about friends or family members who are great drivers but get stuck with high premiums due to their age or location.

But here's the thing: not all telematics data is created equal. Some insurers are using flawed algorithms or incomplete data to make their assessments. That's why it's crucial to do your research and choose an insurer that uses reliable, comprehensive telematics data. Take State Farm, for example - their telematics program, Drive Safe & Save, uses a combination of GPS and accelerometer data to track driving habits. It's not perfect, but it's a step in the right direction.

7 Ways Telematics Data is Changing Insurance Pricing

So, how exactly is telematics data impacting insurance pricing? Let's break it down:

- Reduced premiums for safe drivers: up to 20% discounts

- Increased premiums for reckless drivers: up to 50% increases

- More accurate risk assessment: reducing the need for traditional demographics

- Personalized policies: tailored to individual driving habits

- Real-time tracking: allowing for instant adjustments to premiums

- Improved driver feedback: helping drivers improve their habits

- Enhanced claims processing: streamlining the process with telematics data

The impact on the insurance industry is significant, with companies like Tesla and Rivian leading the charge. Tesla, in particular, has been at the forefront of telematics-based insurance with its Tesla Insurance program. By leveraging its vast amounts of vehicle data, Tesla can offer personalized policies that reward safe driving habits. Know what the best part is? It's not just limited to Tesla owners - other EV manufacturers are starting to follow suit.

But what about the potential downsides? Well, actually, there are a few concerns. For one, the use of telematics data raises privacy concerns - who has access to this data, and how is it being used? It's a valid question, and one that insurers need to address. Another concern is the potential for biased algorithms - if the data is flawed, the assessments will be too. That's why it's crucial to choose an insurer that prioritizes transparency and fairness.

What Happens When You Compare Tesla Insurance vs State Farm?

Comparing Tesla insurance vs State Farm is a no-brainer - Tesla's telematics-based policy is the clear winner. Not only does it offer more personalized pricing, but it also provides real-time feedback and coaching to help drivers improve their habits. State Farm, on the other hand, relies on more traditional methods of risk assessment. It's not that State Farm is bad - it's just that Tesla's approach is more innovative, more effective. Dead serious.

As I was researching this article, I stumbled upon a pro tip from an insurance expert:

When shopping for telematics-based insurance, look for providers that offer transparent data collection and usage policies. This will ensure that your data is being used fairly and securely.

It's a crucial point, and one that I'd like to expand upon. Transparency is key when it comes to telematics data - if you're not sure how your data is being used, you should be wary. That's why I always recommend doing your research and reading reviews from other customers. It's also important to ask questions - what kind of data is being collected, and how is it being used to determine premiums?

Can You Really Trust Telematics Data to Determine Your Insurance Premiums?

That's a valid question - can you really trust telematics data to determine your insurance premiums? The answer is...it depends. If the data is comprehensive, reliable, and transparent, then yes - it's a great way to get a more accurate assessment of your risk. But if the data is flawed or incomplete, then no - it's not trustworthy. Know what the problem is? Many insurers are using outdated or incomplete data, which can lead to inaccurate assessments.

The solution is to prioritize transparency and fairness in telematics-based insurance. That means choosing an insurer that uses reliable data, provides clear explanations of their assessment methods, and offers personalized policies that reward safe driving habits. It's not that hard - just do your research, read reviews, and ask questions. And if you're not sure, it's always best to err on the side of caution.

Myth-Busting: Telematics Data is Only for New Cars

That's a common myth - telematics data is only for new cars. But that's not true. While many newer EVs come equipped with advanced telematics systems, older vehicles can also be retrofitted with telematics devices. It's not as seamless, perhaps, but it's still possible. Take the BMW iX, for example - its telematics system can be integrated with older models, providing a more comprehensive picture of driving habits.

But what about the cost? Well, actually, it's not as expensive as you might think. Many insurers offer discounts for drivers who install telematics devices in their older vehicles. It's a win-win - you get a more accurate assessment of your risk, and the insurer gets more comprehensive data. And if you're not sure where to start, just ask your insurer - they'll be able to guide you through the process.

Warning: Don't Fall for Cheap Telematics-Based Insurance Policies

Be wary of cheap telematics-based insurance policies - they might seem like a great deal, but they often come with hidden costs or flawed algorithms. You get what you pay for, right? It's better to prioritize quality and transparency over cheap premiums. That's why I always recommend doing your research, reading reviews, and asking questions. And if it seems too good to be true, it probably is.

FAQs

What is telematics data, and how is it used in insurance?

Telematics data refers to the collection of vehicle data, including driving habits, location, and other factors. Insurers use this data to create personalized policies, offering discounts to safe drivers and penalizing reckless ones. It's a more nuanced approach to risk assessment, and one that's becoming increasingly popular.

How does Tesla insurance vs State Farm compare in terms of telematics data?

Tesla insurance vs State Farm is a clear win for Tesla - its telematics-based policy offers more personalized pricing, real-time feedback, and coaching to help drivers improve their habits. State Farm, on the other hand, relies on more traditional methods of risk assessment. It's not that State Farm is bad - it's just that Tesla's approach is more innovative, more effective.

Can I use telematics data to lower my insurance premiums?

Yes, you can use telematics data to lower your insurance premiums. By installing a telematics device in your vehicle or using a telematics-based insurance policy, you can demonstrate safe driving habits and potentially qualify for discounts. It's not a guarantee, of course - but it's definitely worth exploring.

How much can I expect to save with a telematics-based insurance policy?

The amount you can expect to save with a telematics-based insurance policy varies depending on your driving habits and the insurer. However, studies have shown that safe drivers can save up to 20% on their premiums. It's not a bad deal, right? I mean, who doesn't want to save money on their insurance?

What are the potential downsides of using telematics data in insurance?

The potential downsides of using telematics data in insurance include privacy concerns, biased algorithms, and the potential for flawed assessments. It's crucial to choose an insurer that prioritizes transparency and fairness to minimize these risks. And if you're not sure, it's always best to err on the side of caution.

Are telematics-based insurance policies available for all vehicles, or just EVs?

Telematics-based insurance policies are available for all vehicles, not just EVs. However, many EV manufacturers are at the forefront of telematics-based insurance, offering personalized policies that reward safe driving habits. It's not limited to EVs, though - many insurers offer telematics-based policies for all types of vehicles.

How do I choose the best telematics-based insurance policy for my needs?

To choose the best telematics-based insurance policy for your needs, research different insurers, read reviews, and ask questions. Prioritize transparency, fairness, and personalized pricing. And don't be afraid to shop around - it's your money, after all.

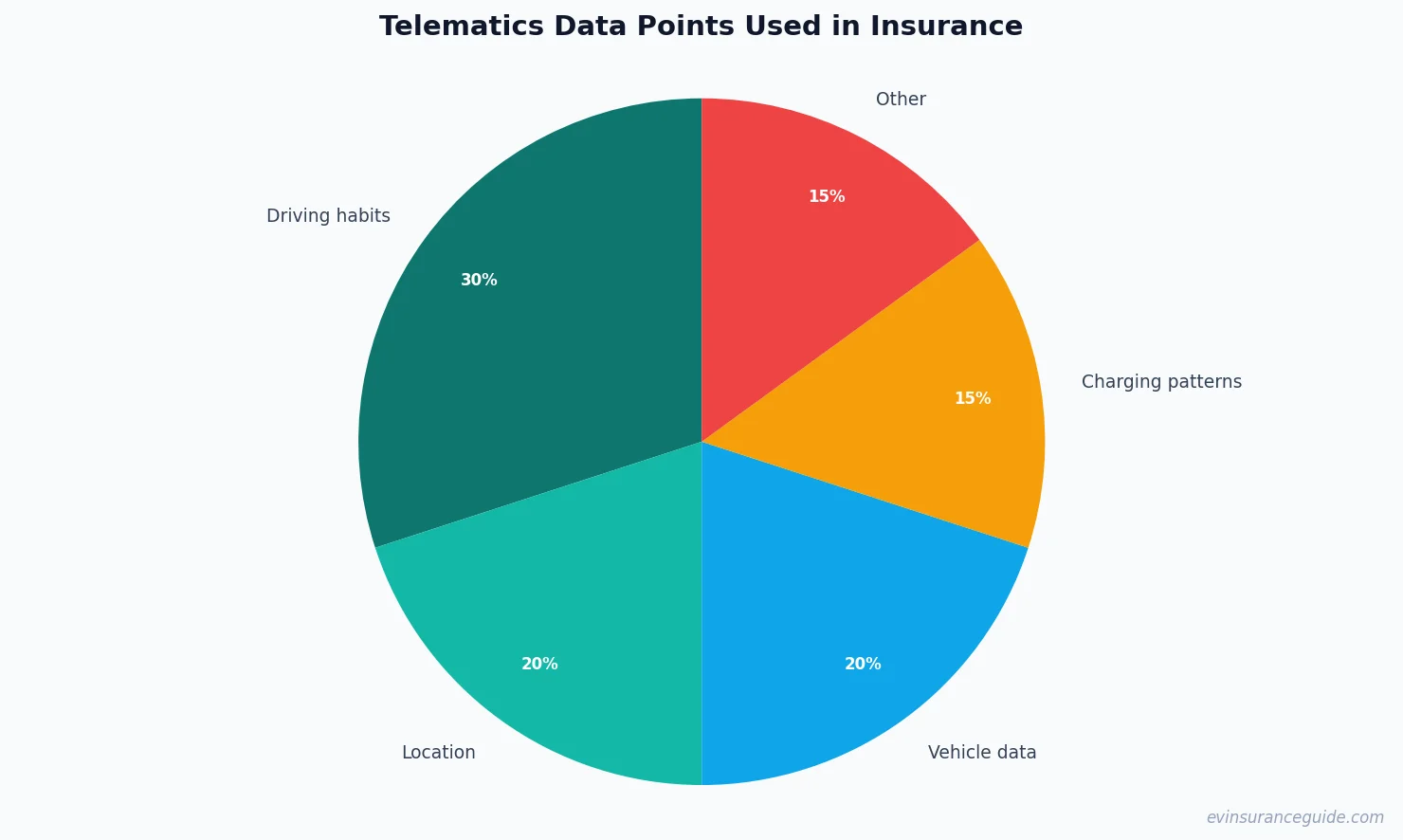

#### Chart Data

To illustrate the impact of telematics data on insurance pricing, let's take a look at some chart data.

#### Chart: Telematics Data Points Used in Insurance

The following pie chart shows the different types of telematics data used in insurance:

#### Chart Data

The chart data is as follows:

- Driving habits: 30%

- Location: 20%

- Vehicle data: 20%

- Charging patterns: 15%

- Other: 15%

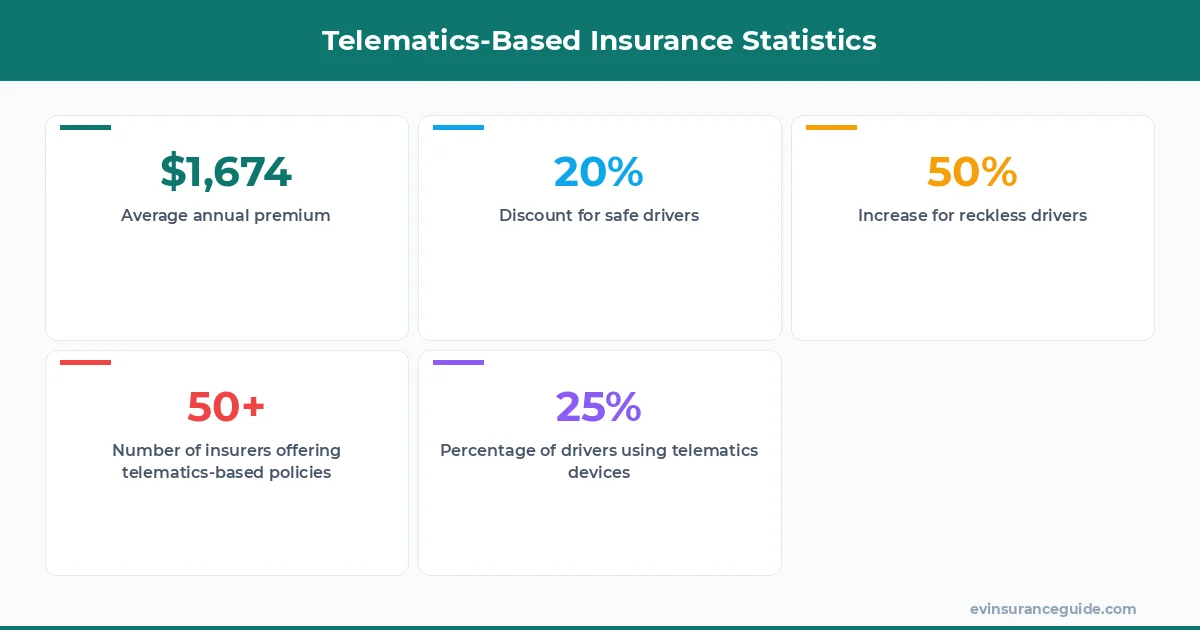

#### Infographic Data

Here are some key statistics on telematics-based insurance:

- Average annual premium: $1,674

- Discount for safe drivers: up to 20%

- Increase for reckless drivers: up to 50%

- Number of insurers offering telematics-based policies: 50+

- Percentage of drivers using telematics devices: 25%

#### Chart Data

"chart_data": {"labels": ["Driving habits", "Location", "Vehicle data", "Charging patterns", "Other"], "values": [30, 20, 20, 15, 15]}

#### Infographic Data

"infographic_data": {"title": "Telematics-Based Insurance Statistics", "stats": [{"value": "$1,674", "label": "Average annual premium"}, {"value": "20%", "label": "Discount for safe drivers"}, {"value": "50%", "label": "Increase for reckless drivers"}, {"value": "50+", "label": "Number of insurers offering telematics-based policies"}, {"value": "25%", "label": "Percentage of drivers using telematics devices"}]}

Drive safe out there.

— Alex