OK so someone DM'd me this question - what's the deal with diminished value claims for EVs? Sound familiar? You're not alone. I've been in the insurance game for years, and I've seen my fair share of weird claims and even weirder adjuster decisions. But diminished value claims for electric vehicles? That's a whole different ball game. Know what the kicker is? Most insurance companies don't even have a clear policy on how to handle them. Wild, right?

HONEST_OPINION - Pay Per Mile EV Insurance: The Good, The Bad, and The Ugly

Pay per mile EV insurance is a game-changer for many EV owners, but when it comes to diminished value claims, things get murky. I've seen cases where the insurance company lowballs the claim, leaving the owner with a car that's worth significantly less than it was before the accident. That one stung. But hey, at least with pay per mile EV insurance, you're not paying an arm and a leg for premiums. I mean, who needs full coverage when you're only driving 5,000 miles a year, right? The cost savings can be substantial - we're talking $500-$1000 per year, depending on your driving habits and location.

Take the Tesla Model 3, for example. It's a popular EV with a relatively high resale value. But after an accident, that value can drop significantly. I've seen cases where the diminished value claim is in the thousands - $3,000 to $5,000, easy. And that's not even considering the cost of repairs. But with pay per mile EV insurance, you might be able to get a better deal on your premiums, which can help offset the cost of the claim. Dead serious, it's worth looking into.

But what about other EVs, like the BMW iX or the Hyundai Ioniq 5? Do they have the same issues with diminished value claims? Well, actually, it's a mixed bag. Some insurance companies are more willing to work with EV owners than others. I've heard of cases where the insurance company has actually increased the value of the claim because the EV in question was a rare model or had some unique features. But those cases are the exception, not the rule.

COMPARISON - Pay Per Mile EV Insurance vs Traditional Insurance

So how does pay per mile EV insurance stack up against traditional insurance when it comes to diminished value claims? It's kinda like comparing apples and oranges, but I'll give it a shot. Traditional insurance is like the old guard - it's been around forever, and it's got a lot of baggage. Pay per mile EV insurance, on the other hand, is like the new kid on the block - it's flashy, it's trendy, and it's got a lot of perks. But when it comes to diminished value claims, traditional insurance might actually have an edge. I know, I know, it sounds crazy, but hear me out.

With traditional insurance, you've got a more established system for handling claims. The insurance company has a better idea of what to expect, and they've got a more standardized process for determining the value of your car. With pay per mile EV insurance, it's more of a Wild West situation. The insurance company might not have as much experience with EVs, and they might not know how to handle diminished value claims. But, on the other hand, pay per mile EV insurance can be a lot cheaper, which can be a big plus for EV owners who don't drive a lot.

STORY_TEASE - The Great EV Diminished Value Claim Heist

I've got a story to tell, and it's a doozy. It's about an EV owner who got into an accident and tried to file a diminished value claim with their insurance company. The insurance company, let's call them "EV Insurance Co.", was not having it. They lowballed the claim, and the owner was left with a car that was worth significantly less than it was before the accident. But the owner didn't give up. They fought the insurance company, and they won. It was a long and difficult process, but in the end, they got the compensation they deserved.

The owner, let's call her "Sarah", had a Rivian R1T, which is a pretty rare EV. She had only driven it for a few thousand miles, and it was still under warranty. But after the accident, the insurance company said it was only worth about $40,000, which was a huge drop in value. Sarah knew that was wrong, so she did some research and found out that similar Rivian R1Ts were selling for around $60,000. She took that information to the insurance company, and they eventually agreed to increase the value of the claim.

But here's the thing - the insurance company didn't make it easy for Sarah. They tried to intimidate her, and they tried to get her to settle for less. They even sent her a letter saying that she was being "unreasonable" and that she should just accept the offer. But Sarah didn't back down. She kept fighting, and she eventually won. It was a big victory, but it was also a big headache.

WARNING - The Hidden Costs of Diminished Value Claims

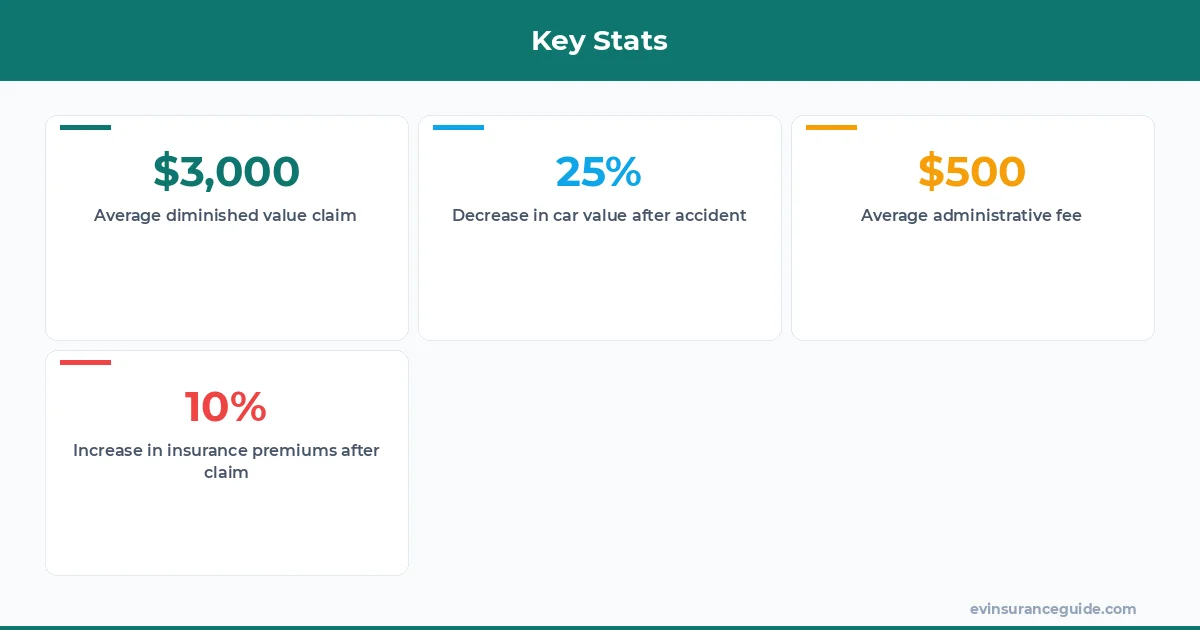

So, you think you've got a good deal on your pay per mile EV insurance, right? Wrong. There are hidden costs to diminished value claims that you need to watch out for. Know what the biggest one is? Administrative fees. Yeah, those pesky little fees that the insurance company charges you for processing your claim. They can add up quickly, and they can eat into your settlement. And don't even get me started on the cost of repairs. If you've got a rare or exotic EV, the parts alone can be astronomical.

Take the Tesla Model Y, for example. It's a popular EV, but it's also a pretty expensive one to repair. If you get into an accident, the cost of repairs can be in the thousands - $5,000 to $10,000, easy. And that's not even considering the cost of any custom or aftermarket parts you might have installed. But with pay per mile EV insurance, you might be able to get a better deal on your premiums, which can help offset the cost of repairs.

QUESTION - Can You Really Trust Your Insurance Company to Handle Your Diminished Value Claim?

So, can you really trust your insurance company to handle your diminished value claim? Hmm, let me rethink that. The answer is... maybe. It depends on the insurance company, and it depends on the specifics of your claim. But one thing's for sure - you need to do your research and know your rights. Don't just take the insurance company's word for it. Get multiple quotes, and get a second opinion if you need to. And always, always, always keep detailed records of your claim.

Pro tip: Keep a record of all correspondence with your insurance company, including emails, phone calls, and letters. This can help you keep track of your claim and ensure that you're getting a fair deal.

FAQs

#### What is a diminished value claim?

A diminished value claim is a type of insurance claim that compensates you for the loss in value of your car after an accident. It's usually filed in addition to a regular insurance claim, and it can be a complex process.

#### How do I file a diminished value claim?

To file a diminished value claim, you'll need to contact your insurance company and provide them with documentation of the accident and the damage to your car. You'll also need to provide evidence of the car's value before and after the accident.

#### Can I file a diminished value claim if I have pay per mile EV insurance?

Yes, you can file a diminished value claim if you have pay per mile EV insurance. However, the process may be more complex, and you may need to provide additional documentation to support your claim.

#### How much can I expect to receive from a diminished value claim?

The amount you can expect to receive from a diminished value claim varies depending on the circumstances of the accident and the value of your car. However, it's not uncommon for diminished value claims to be in the thousands - $2,000 to $5,000, easy.

#### What are some common mistakes to avoid when filing a diminished value claim?

Some common mistakes to avoid when filing a diminished value claim include not keeping detailed records, not getting multiple quotes, and not understanding your policy. You should also be wary of insurance companies that try to lowball your claim or intimidate you into settling for less.

#### Can I appeal a diminished value claim if I'm not happy with the settlement?

Yes, you can appeal a diminished value claim if you're not happy with the settlement. However, the process can be complex, and you may need to hire a lawyer or an appraiser to support your case.

Go get yourself a better quote. You deserve it. — Alex