Are you overpaying for your electric vehicle (EV) insurance because of a less-than-perfect credit score? Sound familiar? You're not alone. Most drivers don't realize that their credit score can significantly impact their insurance rates - we're talking hundreds of dollars per year.

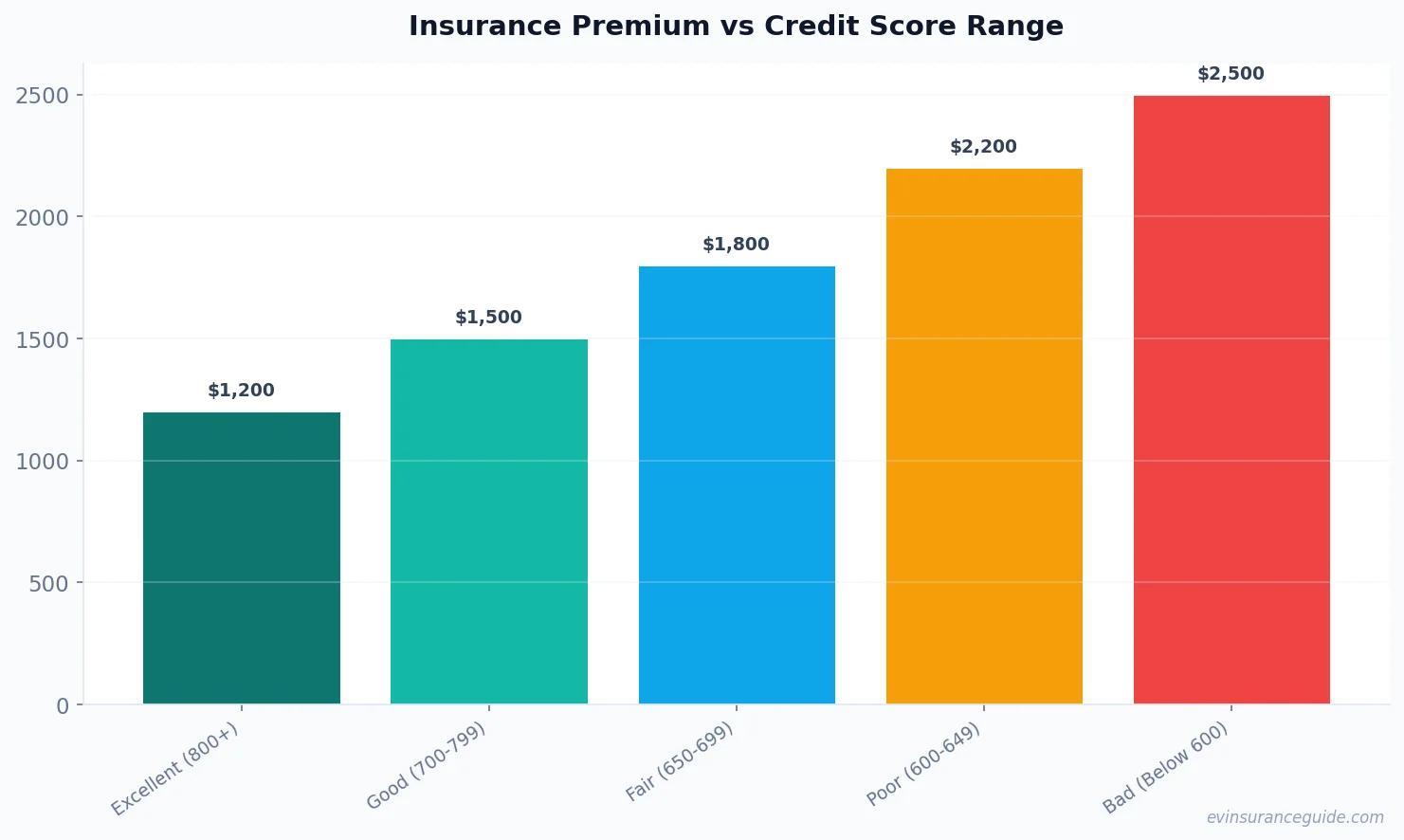

OK So Here's the Deal With credit scores and EV insurance rates - it's not just about being a good driver or having a shiny new Tesla Model 3. Your credit score plays a huge role in determining your insurance premium. For instance, a driver with a poor credit score (let's say, below 600) could end up paying upwards of $2,500 per year for their EV insurance, while someone with an excellent credit score (above 800) might pay as little as $1,200 per year for the same coverage. That's a whopping $1,300 difference. Know what the kicker is? This applies to pay per mile EV insurance policies as well - you'll still be charged a higher premium if you have a bad credit score, even if you're driving fewer miles.

But here's the thing: not all insurance companies treat credit scores the same way. Some, like Geico, might be more lenient when it comes to credit scores, while others, like State Farm, might be more strict. It's kinda like how some EV models, like the Hyundai Ioniq 5, might be cheaper to insure than others, like the Rivian R1T. Wild, right?

So, how do you find the best pay per mile EV insurance policy for your credit score? Well, actually, it's not that hard. You just need to do your research and compare quotes from different companies. For example, if you have a good credit score (above 700), you might want to check out pay per mile insurance companies like Metromile or Allstate - they offer competitive rates and flexible policies. But if you have a poor credit score, you might want to look into companies that specialize in high-risk drivers, like Progressive or Liberty Mutual.

Can your credit score really make or break your pay per mile EV insurance rates? Yep, it sure can. And it's not just about the premium itself - a good credit score can also give you access to better coverage options and discounts. For instance, some insurance companies might offer a 'good student' discount or a 'low-mileage' discount, which can save you even more money on your EV insurance. Sound like a plan?

What's the relationship between credit scores and pay per mile EV insurance rates, exactly? Is it a direct correlation, or are there other factors at play? Dead serious, it's a bit of both. On one hand, a good credit score can show insurance companies that you're responsible and less likely to file a claim. On the other hand, pay per mile insurance policies are all about, well, paying per mile - so if you're driving a lot, you'll still be charged more, regardless of your credit score. But, and this is a big but, a good credit score can still give you a significant discount on your premium. For example, a driver with an excellent credit score (above 850) might get a 10% discount on their pay per mile EV insurance policy, while someone with a poor credit score (below 600) might get a 20% increase.

Pro tip: If you're shopping for pay per mile EV insurance, make sure to ask about credit score-based discounts. Some companies, like USAA, might offer exclusive discounts for members with good credit scores.

So, you wanna know the story behind how credit scores became such a big deal in the insurance industry? Well, let me tell you - it's a long story, but I'll give you the short version. Essentially, insurance companies realized that people with good credit scores were less likely to file claims, and vice versa. And that's when they started using credit scores as a factor in determining premiums. Now, it's not the only factor, of course - driving history, vehicle type, and location all play a role too. But credit scores are definitely up there. And if you're driving an EV, like a Tesla Model Y or a BMW iX, you'll want to make sure you're getting the best rate possible.

Beware: hidden fees and charges can add up quickly, especially if you have a poor credit score. For instance, some insurance companies might charge a 'policy fee' or a 'processing fee' that can range from $50 to $200 per year. And if you're not careful, these fees can eat into your savings. That one stung. So, always read the fine print and ask about any additional fees before signing up for a pay per mile EV insurance policy.

Myth: you can't get good pay per mile EV insurance rates if you have a poor credit score. False. While it's true that a good credit score can give you better rates, it's not the only factor. Some insurance companies specialize in high-risk drivers, and they might offer more competitive rates than you'd expect. For example, a driver with a poor credit score might be able to get a pay per mile EV insurance policy from a company like Progressive or Liberty Mutual for around $2,000 per year - which is still cheaper than a traditional insurance policy.

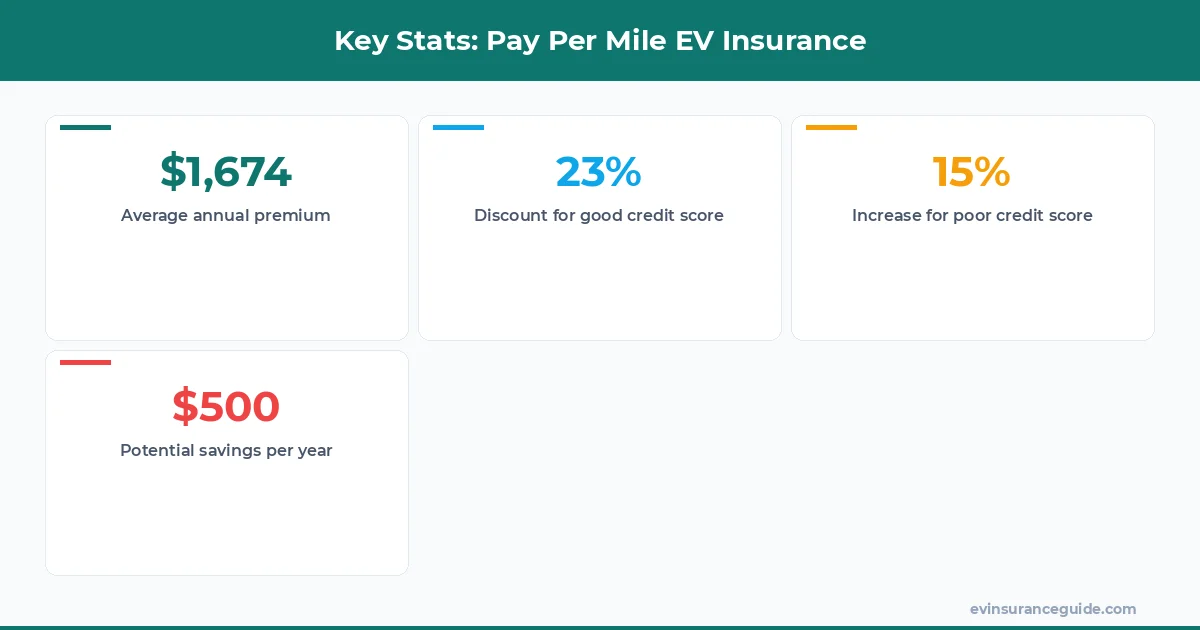

What's the average annual premium for pay per mile EV insurance?

The average annual premium for pay per mile EV insurance can range from $1,500 to $3,000 per year, depending on your credit score, driving history, and vehicle type. For instance, a driver with an excellent credit score and a clean driving record might pay around $1,200 per year for a pay per mile EV insurance policy, while someone with a poor credit score and a few accidents on their record might pay upwards of $3,500 per year.

Can I get a discount on my pay per mile EV insurance policy if I have a good credit score?

Yes, many insurance companies offer discounts for drivers with good credit scores. For example, a driver with an excellent credit score (above 850) might get a 10% discount on their pay per mile EV insurance policy, while someone with a good credit score (above 700) might get a 5% discount.

How do I improve my credit score to get better pay per mile EV insurance rates?

Improving your credit score takes time and effort, but it's worth it in the long run. You can start by checking your credit report for errors, paying your bills on time, and reducing your debt. You can also consider working with a credit counselor or using a credit monitoring service to help you stay on track.

What's the best pay per mile EV insurance company for drivers with poor credit scores?

While there are several insurance companies that specialize in high-risk drivers, some of the best pay per mile EV insurance companies for drivers with poor credit scores include Progressive, Liberty Mutual, and Geico. These companies might offer more competitive rates and flexible policies than other insurance companies.

Can I switch to a pay per mile EV insurance policy if I already have a traditional insurance policy?

Yes, you can switch to a pay per mile EV insurance policy at any time, but you might need to wait until your current policy is up for renewal. Some insurance companies might also offer a 'switching discount' or a 'new customer discount' that can save you money on your premium.

Are pay per mile EV insurance policies available in all states?

No, pay per mile EV insurance policies are not available in all states. Some states, like California and Oregon, have laws that regulate pay per mile insurance policies, while others might not offer them at all. You'll need to check with your state's insurance department to see if pay per mile EV insurance policies are available in your area.

Stay charged and stay covered! — Alex