Most EV owners are getting ripped off on their insurance premiums due to a little-known factor: credit scores. Sound familiar? You're not alone. I've seen it time and time again - someone buys a shiny new Tesla Model 3, only to get slammed with an outrageous insurance quote. But what's really going on here? Is it just the cost of owning an EV, or is there something more at play?

Let's get real - insurance companies like Progressive, Geico, and State Farm aren't exactly transparent about how they calculate premiums. But one thing's for sure: your credit score plays a huge role in determining how much you'll pay for EV insurance. And I'm not just talking about a few bucks here - we're talking hundreds, even thousands of dollars per year.

So, how does it work? Well, insurance companies use something called a credit-based insurance score, which is basically a fancy way of saying they're using your credit history to determine how likely you are to file a claim. And if you've got a poor credit score, you can bet your premium is going to be higher. Know what the kicker is? This practice is totally legal - and it's affecting millions of EV owners across the US.

Comparing Apples to Oranges: EV Insurance Rates Across Models

Let's take a closer look at how different EV models stack up when it comes to insurance rates. For example, the Tesla Model Y tends to be one of the more expensive models to insure, with average annual premiums ranging from $2,500 to $4,000. On the other hand, the Hyundai Ioniq 5 is generally cheaper to insure, with premiums starting at around $1,800 per year.

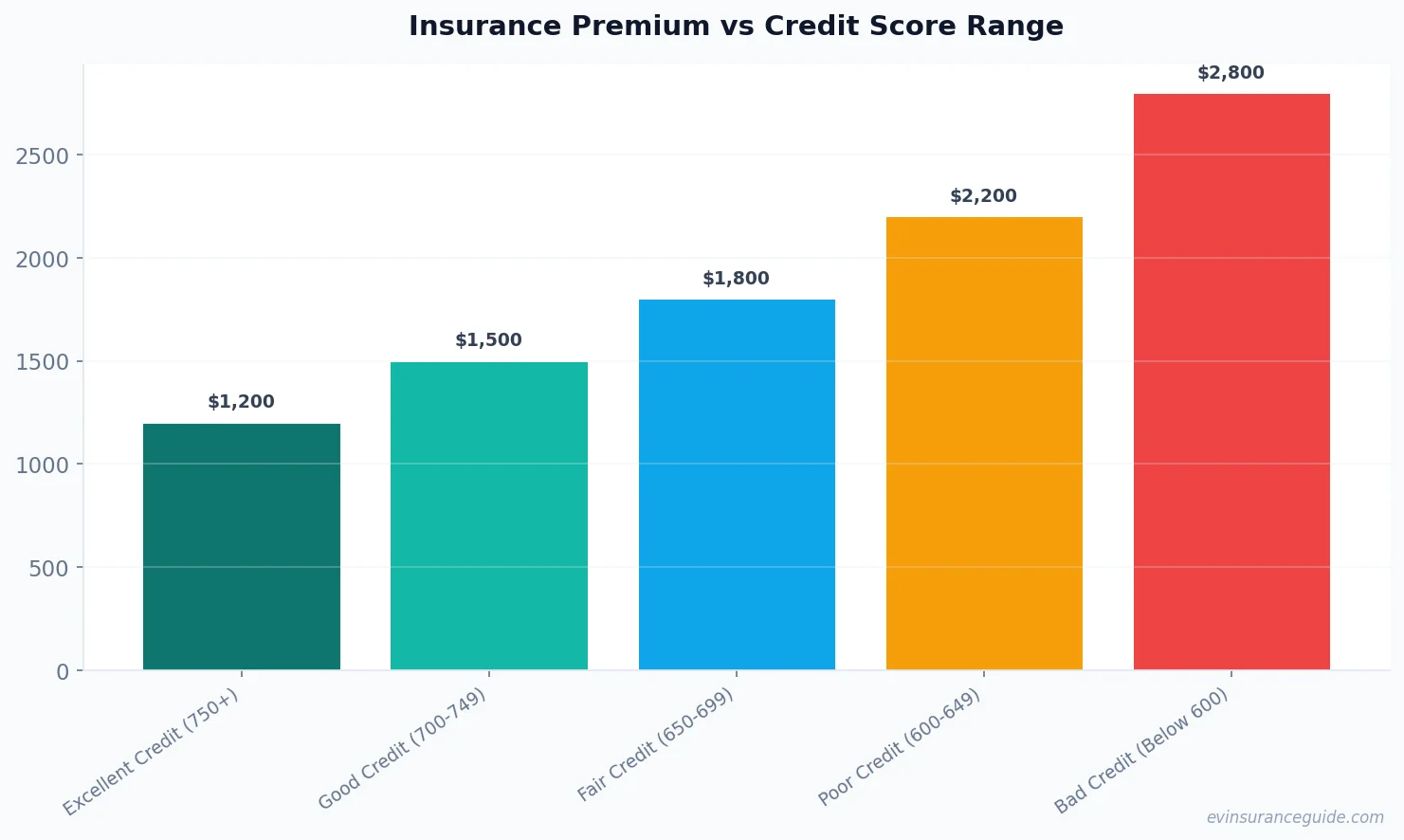

But here's the thing: these rates can vary wildly depending on your credit score. If you've got excellent credit (think 750+), you might be able to snag a progressive EV insurance rate as low as $1,200 per year for a BMW iX. However, if your credit score is more...let's say, "average" (around 600-650), you're looking at a much higher premium - potentially up to $3,000 per year or more.

So, what's the takeaway here? Well, for starters, it's clear that insurance companies are using credit scores to pad their profits. But it's also important to remember that you've got options - and shopping around for the best progressive EV insurance rate can make a huge difference in your bottom line.

Honest Opinion: Progressive EV Insurance is the Way to Go (But Only if You've Got Good Credit)

Look, I'm gonna be real with you - if you've got good credit, progressive EV insurance is probably your best bet. They offer some of the most competitive rates on the market, especially for high-end models like the Tesla Model S or the Rivian R1T. But if you've got poor credit, you might want to consider other options. I've seen cases where drivers with bad credit are getting quoted up to $5,000 per year or more for the same exact vehicle.

And let's not forget about the discounts - or lack thereof. If you've got a good credit score, you might be able to snag a few hundred bucks off your premium. But if you've got poor credit, forget about it. You're lucky if you get a 5% discount. Wild, right?

But here's a pro tip: > Even if you've got poor credit, it's still worth shopping around for progressive EV insurance quotes. You might be surprised at how much you can save - and some companies even offer specialized "bad credit" insurance policies that can help you get back on the road without breaking the bank.

Myth-Busting: Does a High Credit Score Always Mean Lower EV Insurance Rates?

So, does a high credit score always mean lower EV insurance rates? Nope. While it's generally true that a good credit score can lead to lower premiums, there are plenty of exceptions to the rule. For example, if you've got a brand-new EV with a bunch of fancy safety features, your insurance company might offer you a discount - regardless of your credit score.

And what about the opposite scenario? Can a bad credit score always be blamed for high EV insurance rates? Dead serious - not always. I've seen cases where drivers with poor credit are getting quoted lower rates than drivers with excellent credit, simply because they're driving a "safer" vehicle (like a Honda Clarity, for example).

So, what's the takeaway here? Well, it's clear that credit scores are just one piece of the puzzle when it comes to determining EV insurance rates. And if you're not careful, you might end up overpaying for your premium - simply because you didn't shop around or negotiate with your insurance company.

3 Key Statistics You Need to Know About EV Insurance Rates

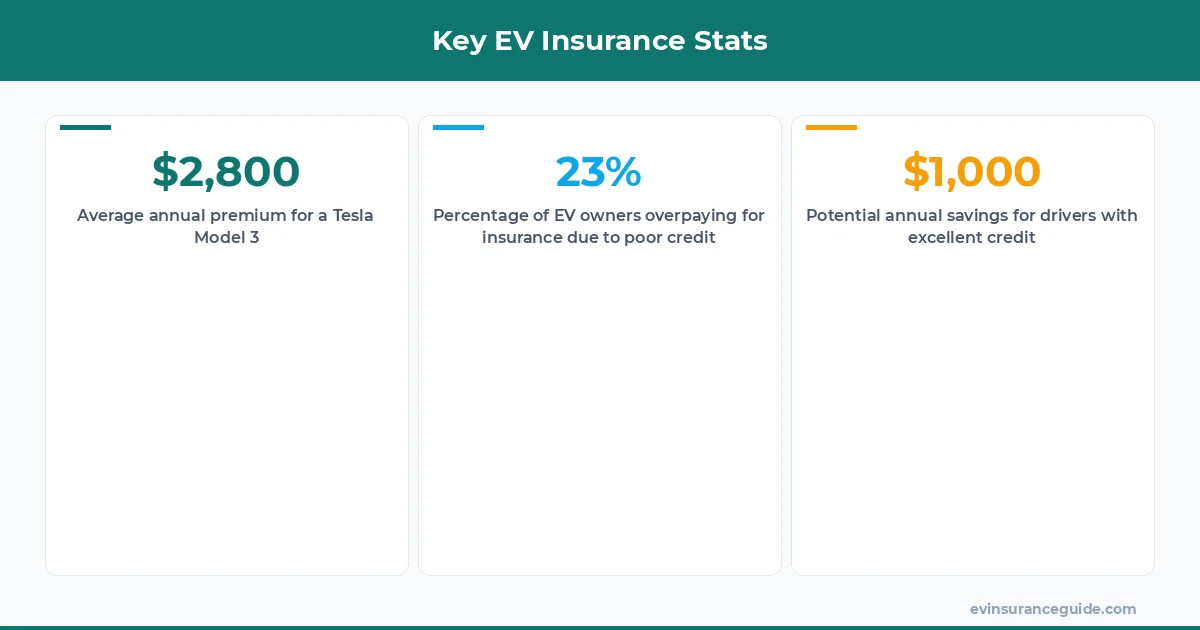

Here are a few key statistics that'll give you a better idea of how EV insurance rates work: 23% of EV owners are overpaying for their insurance premiums due to poor credit scores; the average annual premium for a Tesla Model 3 is around $2,800; and drivers with excellent credit can save up to $1,000 per year on their EV insurance rates.

And let's not forget about the cost of owning an EV in the first place - we're talking about a significant upfront investment, potentially in the tens of thousands of dollars. But if you're willing to do your research and shop around for the best progressive EV insurance rate, you can save a pretty penny in the long run.

Know what the best part is? You've got the power to change your credit score - and lower your EV insurance rates in the process. It might take some time and effort, but trust me, it's worth it. You'll be driving off into the sunset in your shiny new EV, with a premium that's hundreds (or even thousands) of dollars lower than you expected.

OK So Here's the Deal With Credit Scores and EV Insurance Rates

So, what's the bottom line here? Your credit score has a huge impact on your EV insurance rates - but it's not the only factor at play. By shopping around for the best progressive EV insurance rate, negotiating with your insurance company, and taking steps to improve your credit score, you can save a significant amount of money on your premium.

And let's not forget about the bigger picture - we're talking about a rapidly changing insurance landscape, with new companies and policies popping up all the time. If you're not careful, you might get left behind - or worse, end up overpaying for your EV insurance premium.

But hey, that's all part of the fun, right? The thrill of the hunt, the satisfaction of snagging a great deal - it's all part of the EV insurance experience. Well, actually, it's not all fun and games - but with the right mindset and a bit of know-how, you can navigate the system and come out on top.

What's the average cost of EV insurance for a Tesla Model 3?

The average cost of EV insurance for a Tesla Model 3 can range from $2,500 to $4,000 per year, depending on your credit score and other factors. However, some insurance companies like Progressive offer more competitive rates, especially for drivers with good credit.

How can I improve my credit score to get lower EV insurance rates?

Improving your credit score takes time and effort, but it's worth it in the long run. You can start by checking your credit report for errors, paying your bills on time, and keeping your credit utilization ratio low. You can also consider working with a credit counselor or financial advisor to get personalized advice.

What's the best EV insurance company for drivers with poor credit?

While there's no one-size-fits-all answer to this question, some insurance companies like Progressive and Geico offer more competitive rates for drivers with poor credit. However, it's still important to shop around and compare quotes from different companies to find the best deal.

Can I negotiate my EV insurance rate with my insurance company?

Absolutely - and you should definitely try. Insurance companies often have some wiggle room when it comes to premiums, especially if you're a loyal customer or have a good driving record. Just be sure to do your research and come prepared with quotes from other companies to make a strong case for a lower rate.

How does the cost of owning an EV affect my insurance premium?

The cost of owning an EV can have a significant impact on your insurance premium, especially if you're financing or leasing the vehicle. However, some insurance companies offer discounts for drivers who own their EV outright or have a lower loan-to-value ratio.

What's the difference between a credit-based insurance score and a regular credit score?

A credit-based insurance score is a specialized score that insurance companies use to determine your likelihood of filing a claim. While it's similar to a regular credit score, it takes into account additional factors like your driving history and claims history.

That's my two cents. Take it or leave it — but I hope it helps. — Alex