Insuring an electric vehicle is a total rip-off — unless you know the secret to bringing down those costs: resale value. That's right, the way your EV holds its value can significantly impact your insurance premiums. Sound familiar? You buy a brand new EV, excited to hit the road, only to find out your insurance quotes are through the roof. But what if you could slash those costs by choosing an EV with a high resale value? Dead serious, it's a game-changer.

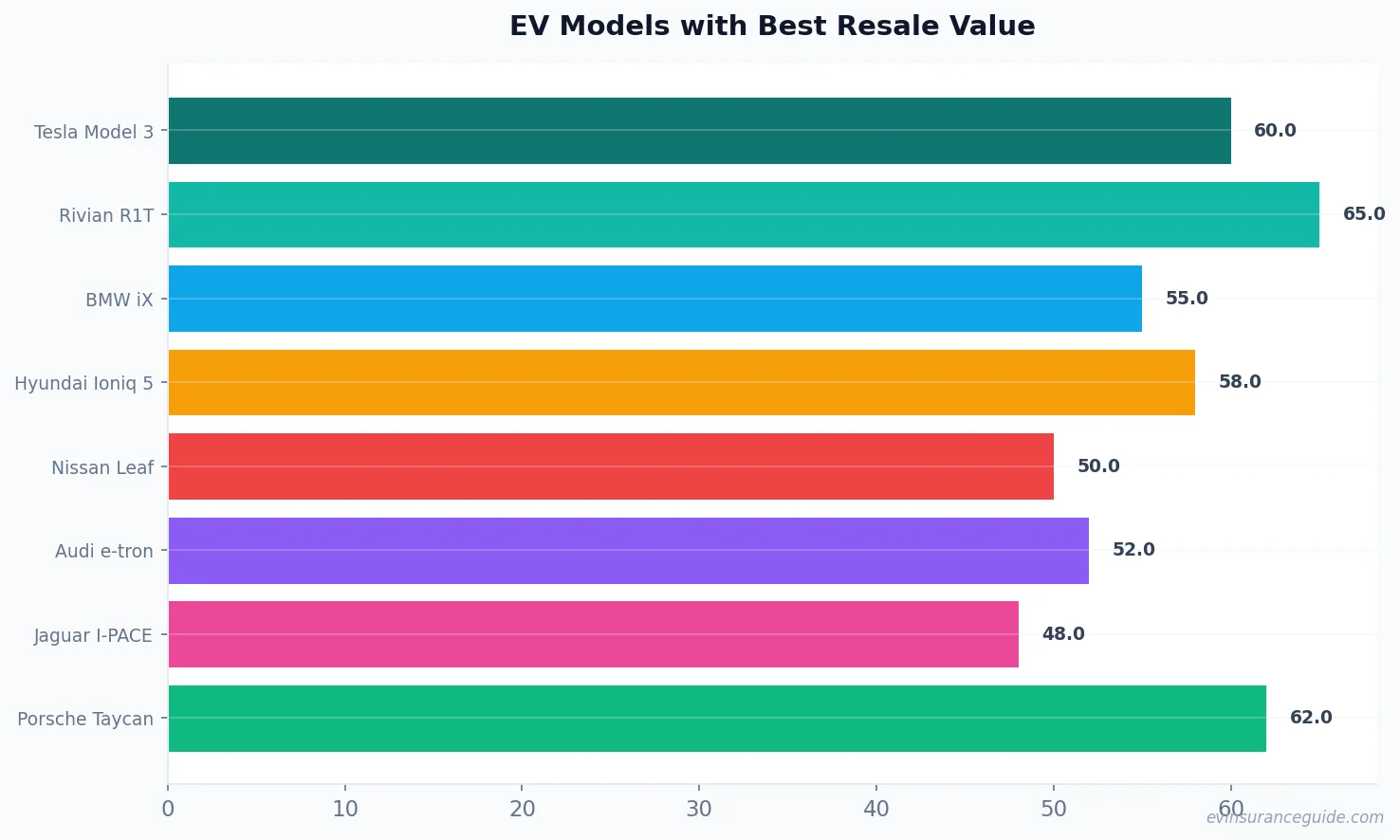

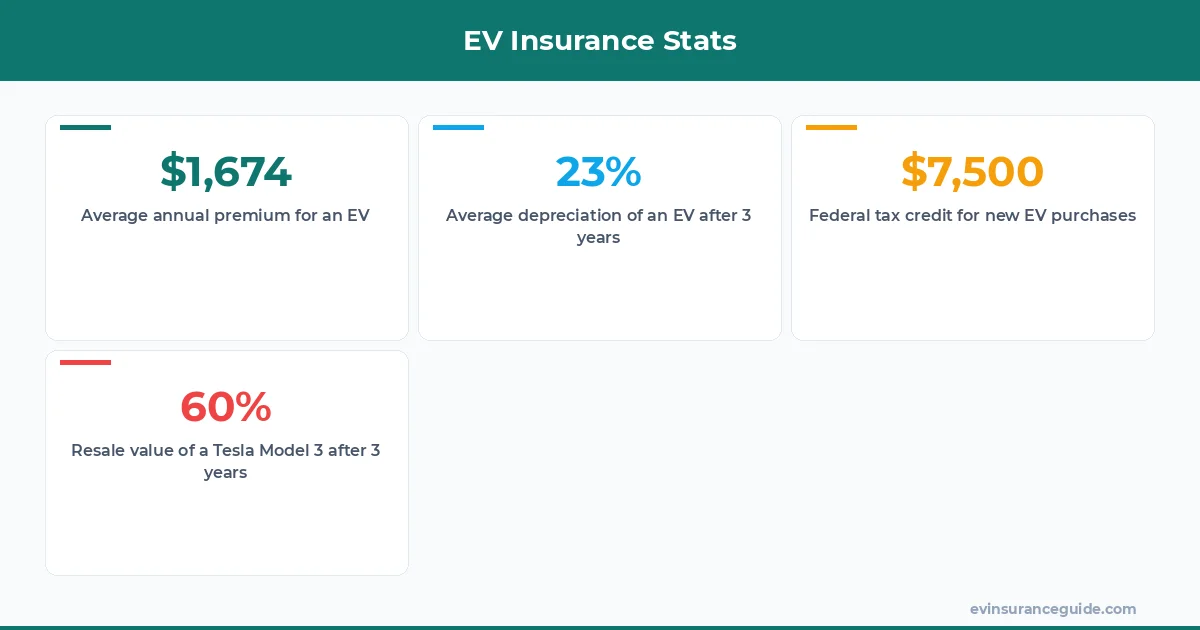

For instance, the Tesla Model 3 — one of the best-selling EVs on the market — retains around 60% of its value after 3 years, according to data from Kelley Blue Book. That's a major factor in determining your insurance premiums. Know what the kicker is? Insurers care about resale value because it directly affects the cost of replacing or repairing your vehicle in the event of an accident. So, if you're in the market for a new EV and want to keep your insurance costs in check, you need to consider the resale value of your potential new ride.

OK So Here's the Deal With Resale Value and EV Insurance

The resale value of an EV is a crucial factor in determining insurance premiums. It's simple math, really: if your vehicle holds its value well, the insurer won't have to shell out as much to replace it if something goes wrong. And that means lower premiums for you. But, which EVs hold their value best? Well, actually, it's not just about the vehicle itself — it's also about the manufacturer's reputation, the overall demand for the model, and even the battery's durability. Take the Hyundai Ioniq 5, for example: its sleek design, impressive range, and eco-friendly features make it a hot seller, which in turn, drives up its resale value. And, as a result, its insurance premiums are relatively lower compared to other EVs in its class.

To give you a better idea, here are some estimated insurance costs for popular EVs: the Tesla Model Y can range from $1,500 to $2,500 per year, while the BMW iX can set you back around $2,000 to $3,500 annually. But, the Rivian R1T? That's a whole different story. With its impressive off-road capabilities, luxurious interior, and cutting-edge tech, the R1T is a highly sought-after vehicle, which means its resale value is through the roof. And, consequently, its insurance premiums are relatively lower, with estimates ranging from $1,200 to $2,200 per year.

Now, I know what you're thinking: "Is it really worth it to pay a premium for an EV with high resale value, just to save on insurance?" And my answer is, absolutely. Think about it: over the course of 5 years, you could save upwards of $5,000 to $10,000 on insurance alone, depending on your location, driving record, and other factors. That's a significant chunk of change, if you ask me.

5 Key Factors Affecting EV Resale Value

The resale value of an EV is influenced by a multitude of factors, including the vehicle's range, charging time, and overall performance. But, what about the role of rivian insurance cost in all this? Well, it's simple: if you're looking to minimize your insurance premiums, you need to choose an EV with a high resale value. And, one of the best ways to do that is to opt for a vehicle with a reliable battery, a solid warranty, and a reputation for durability.

For instance, the Rivian R1T comes with an 8-year, 175,000-mile battery warranty, which gives owners peace of mind and helps maintain the vehicle's resale value. On the other hand, the Tesla Model 3 has a more comprehensive warranty, with 8 years or 120,000 miles of coverage, whichever comes first. But, which one is better? Well, that depends on your specific needs and preferences. If you're looking for a more affordable option with a still-impressive range, the Hyundai Ioniq 5 might be the way to go. Its estimated 5-year depreciation is around 40%, which is relatively low compared to other EVs in its class.

And, let's not forget about the impact of software updates on resale value. Take Tesla, for example: its over-the-air updates ensure that its vehicles stay up-to-date with the latest features and tech, which in turn, helps maintain their resale value. Wild, right? It's like having a brand new car, every few months.

What Happened to John and His Rivian R1T

I've got a friend, John, who recently purchased a Rivian R1T. He's a huge fan of the brand and was excited to get behind the wheel of his new vehicle. But, what he didn't realize was that the R1T's high resale value would end up saving him a pretty penny on insurance. He was quoted around $1,800 per year, which is relatively low compared to other EVs in its class.

As John puts it, "I was expecting to pay a lot more for insurance, given the R1T's price tag. But, it turns out that its high resale value and impressive safety features really brought down the cost." Now, I know what you're thinking: "That's great and all, but what about the rest of us who can't afford a Rivian?" Well, the good news is that there are plenty of other EVs on the market with high resale value, and therefore, lower insurance premiums.

For example, the Nissan Leaf has an estimated 5-year depreciation of around 50%, which is relatively high compared to other EVs. But, its lower purchase price and affordable insurance premiums make it an attractive option for budget-conscious buyers. And, let's not forget about the federal tax credit, which can save you up to $7,500 on your new EV purchase.

Honestly, Some EV Insurance Policies Are Overpriced Trash

Let's get real for a second: some EV insurance policies are a total rip-off. I mean, who needs to pay $3,000 per year for insurance, when you can get a similar policy for half the price? It's all about doing your research, comparing quotes, and finding the best deal for your specific needs.

Pro tip: always ask about discounts for things like low mileage, good grades, or even being a member of certain organizations. You'd be surprised at how much you can save.

Now, I'm not saying that all EV insurance policies are created equal. Some are definitely better than others, and it's up to you to find the one that works best for you. But, one thing's for sure: if you're not considering the resale value of your EV when shopping for insurance, you're making a big mistake. It's like trying to buy a house without checking the neighborhood first — it just doesn't make sense.

Take the BMW iX, for example: its high purchase price and relatively low resale value make it a more expensive option to insure. But, its impressive range, luxurious interior, and cutting-edge tech make it a highly sought-after vehicle. So, is it worth it? Well, that depends on your priorities. If you're looking for a luxurious EV with all the bells and whistles, the iX might be the way to go. But, if you're on a budget, you might want to consider something else.

Comparing Rivian Insurance Cost to Other EVs

So, how does the Rivian insurance cost stack up against other EVs on the market? Well, it's a mixed bag, really. On the one hand, the R1T's high resale value and impressive safety features make it a relatively affordable option to insure. But, on the other hand, its high purchase price and limited availability make it a more expensive option overall.

To give you a better idea, here are some estimated insurance costs for popular EVs: the Tesla Model 3 can range from $1,200 to $2,500 per year, while the Hyundai Ioniq 5 can set you back around $1,500 to $3,000 annually. But, the Rivian R1T? That's a whole different story, with estimates ranging from $1,200 to $2,200 per year. Now, I know what you're thinking: "Is the R1T really worth it?" And my answer is, absolutely. Its unique blend of off-road capability, luxurious interior, and cutting-edge tech make it a highly sought-after vehicle, and its relatively low insurance premiums are just the icing on the cake.

FAQs

#### What is the average insurance cost for an EV?

The average insurance cost for an EV can range from $1,000 to $3,000 per year, depending on the make, model, and other factors. For example, the Tesla Model Y can cost around $1,500 to $2,500 per year to insure, while the Rivian R1T can cost around $1,200 to $2,200 per year.

#### How does resale value affect EV insurance premiums?

The resale value of an EV can significantly impact insurance premiums. If an EV holds its value well, the insurer won't have to shell out as much to replace it if something goes wrong, which means lower premiums for you.

#### What are some factors that affect EV resale value?

The resale value of an EV is influenced by a multitude of factors, including the vehicle's range, charging time, and overall performance. Other factors, such as the manufacturer's reputation, the overall demand for the model, and even the battery's durability, can also play a role.

#### Can I get a discount on my EV insurance?

Yes, there are several ways to get a discount on your EV insurance. For example, you can ask about discounts for things like low mileage, good grades, or even being a member of certain organizations. You can also compare quotes from different insurers to find the best deal for your specific needs.

#### How does the Rivian insurance cost compare to other EVs?

The Rivian insurance cost is relatively low compared to other EVs on the market. With estimates ranging from $1,200 to $2,200 per year, the R1T is a highly sought-after vehicle that offers a unique blend of off-road capability, luxurious interior, and cutting-edge tech.

#### What is the best way to find affordable EV insurance?

The best way to find affordable EV insurance is to shop around and compare quotes from different insurers. You can also ask about discounts and consider factors such as the vehicle's resale value, safety features, and overall performance.

That's my two cents. Take it or leave it — but I hope it helps. — Alex