Are you a self-employed EV owner who's tired of navigating the complex world of insurance options? You're not alone. The question on every freelancer's mind is: does it make more sense to lease or buy an EV when it comes to insurance costs?

Let's consider the case of Emily, a freelance writer who uses her Tesla Model 3 for both personal and business trips. She's currently paying around $1,800 per year for insurance, but she's not sure if she's getting the best deal. Sound familiar?

The answer, of course, depends on a variety of factors, including your business usage, driving habits, and personal financial situation. But one thing's for sure: EV lease vs buy insurance is a crucial consideration for self-employed and freelance EV owners. Know what the kicker is? Most insurance companies don't make it easy to compare rates and coverage options.

That's why we've put together this guide to help you navigate the world of EV insurance and make an informed decision about whether to lease or buy.

MYTH_BUST: The High Cost of EV Insurance

One common myth about EV insurance is that it's always more expensive than traditional gas-powered vehicle insurance. But is that really true? Not necessarily. While it's true that some EV models, like the BMW iX, can be pricier to insure due to their high sticker price, other models like the Hyundai Ioniq 5 can be relatively affordable.

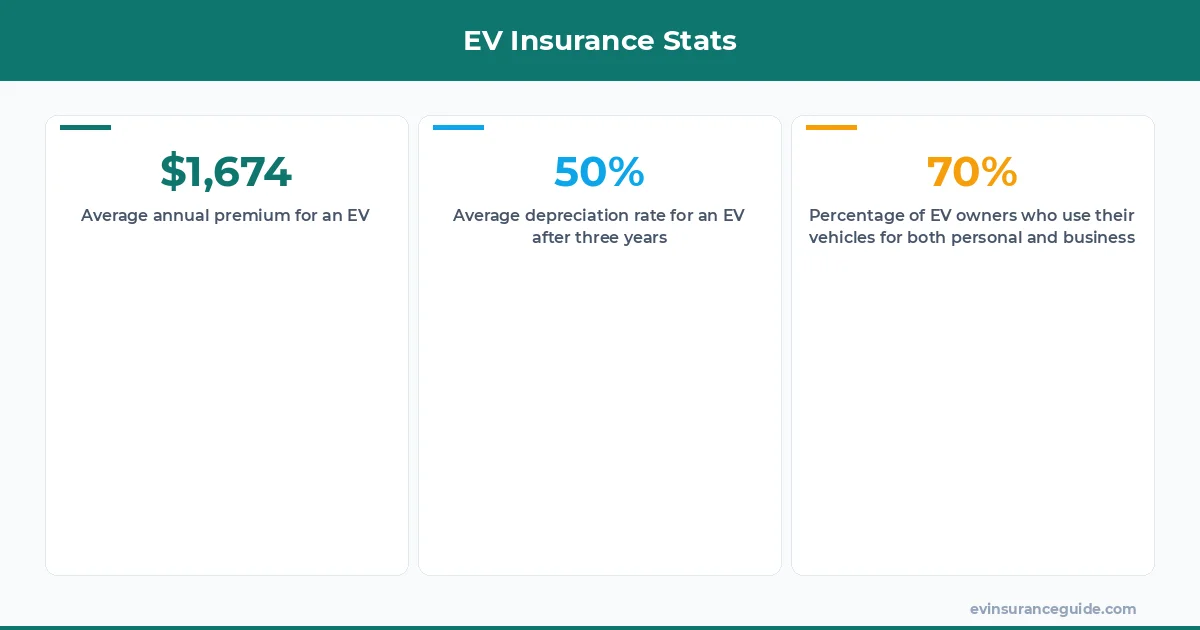

For example, a study by the National Association of Insurance Commissioners found that the average annual premium for an EV is around $1,674, which is only slightly higher than the average premium for a gas-powered vehicle. Dead serious, the cost difference is often negligible.

And let's not forget about the long-term savings of owning an EV. With lower fuel and maintenance costs, you could end up saving thousands of dollars per year. That one stung, didn't it?

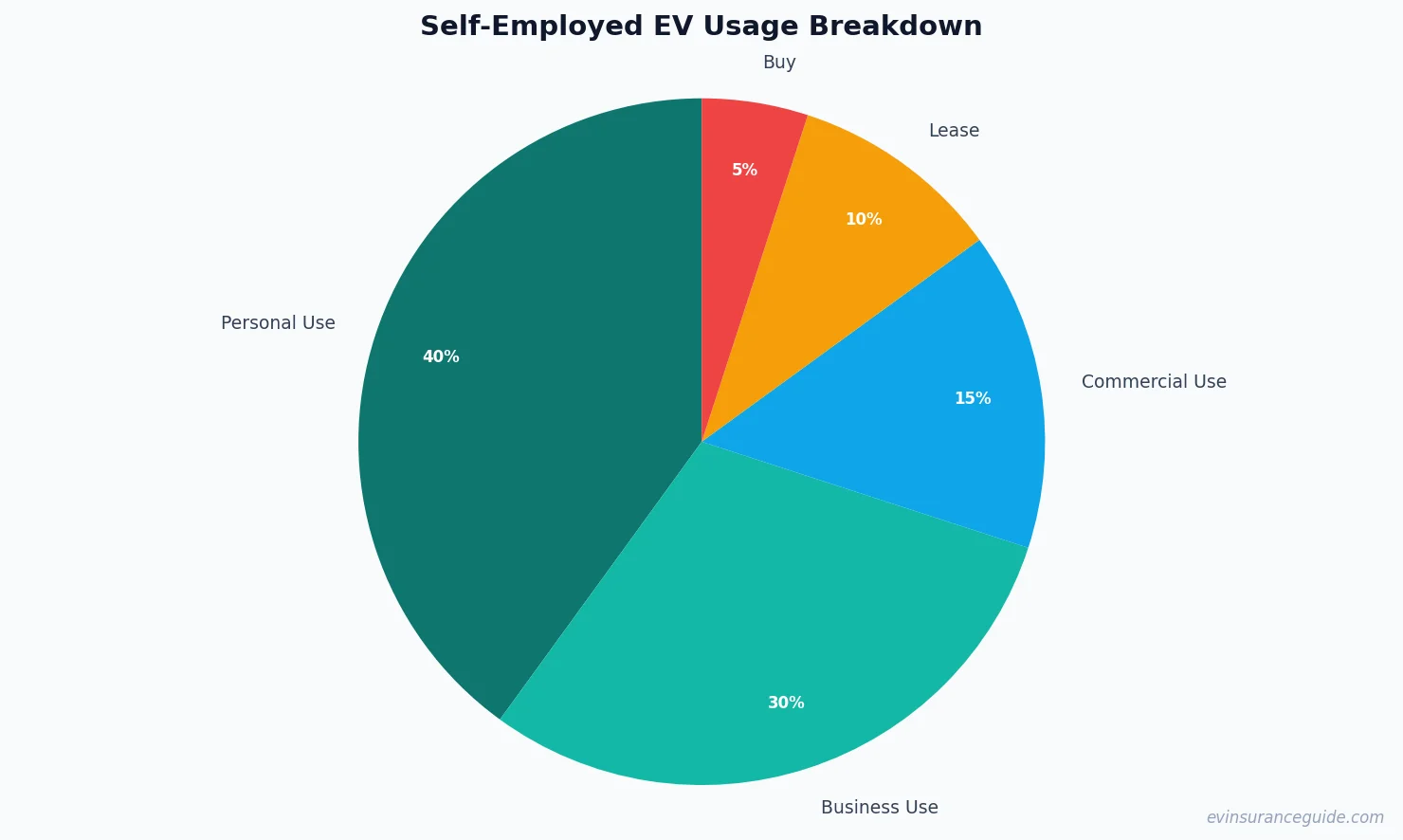

But what about business use? If you're using your EV for business purposes, you may need to purchase a commercial insurance policy, which can be more expensive than a personal policy. However, some insurance companies, like Geico, offer specialized EV insurance policies for business owners that can help reduce costs.

STORY_TEASE: The Real-Life Consequences of Choosing the Wrong Insurance

Meet David, a self-employed consultant who leases a Rivian R1T for both personal and business use. He thought he was getting a good deal on his insurance policy, but when he got into an accident, he discovered that his policy didn't cover all of the damages.

The result? David ended up paying thousands of dollars out of pocket to repair his vehicle. It was a costly mistake, but one that could have been avoided with the right insurance policy.

So, what can you learn from David's experience? For one, it's crucial to carefully review your insurance policy and make sure it covers all of your business use. You should also consider purchasing a policy that includes roadside assistance and rental car coverage, in case you need to rent a vehicle while your EV is being repaired.

And don't even get me started on the importance of shopping around for insurance quotes. You can save hundreds, even thousands, of dollars per year by comparing rates from different insurance companies.

WARNING: The Hidden Costs of EV Lease vs Buy Insurance

When it comes to EV lease vs buy insurance, there are some hidden costs to watch out for. For example, if you lease an EV, you may be required to purchase gap insurance, which can add hundreds of dollars to your annual premium.

And if you buy an EV, you may need to purchase a policy that includes comprehensive and collision coverage, which can be more expensive than liability-only coverage.

But here's the thing: these costs can vary widely depending on the insurance company and the specific policy you choose. That's why it's essential to carefully review your policy and ask questions before signing on the dotted line.

For instance, some insurance companies, like State Farm, offer discounts for EV owners who drive fewer than 7,500 miles per year. Others, like Allstate, offer discounts for EV owners who have a good driving record.

So, do your research and don't be afraid to negotiate. You might be surprised at how much you can save.

HONEST_OPINION: EV Lease vs Buy Insurance - What's the Best Choice?

In my opinion, the best choice between EV lease vs buy insurance depends on your individual circumstances. If you're a self-employed EV owner who uses your vehicle for both personal and business purposes, a lease may be the way to go.

Leasing can provide more flexibility and lower upfront costs, which can be beneficial for freelancers and small business owners. However, if you plan to keep your EV for an extended period, buying may be the better option.

You'll need to consider factors like depreciation, maintenance costs, and insurance premiums to make an informed decision.

For example, a study by the automotive research firm, iSeeCars, found that the average depreciation rate for an EV is around 50% after three years. However, some models, like the Tesla Model Y, hold their value much better than others.

So, it's crucial to do your research and consider all the factors before making a decision.

QUESTION: Can You Really Save Money with EV Lease vs Buy Insurance?

So, can you really save money with EV lease vs buy insurance? The answer is yes, but it depends on your specific situation.

If you're a self-employed EV owner who uses your vehicle for both personal and business purposes, you may be able to save money by leasing an EV.

For instance, a lease can provide lower upfront costs and lower monthly payments, which can be beneficial for freelancers and small business owners.

However, if you plan to keep your EV for an extended period, buying may be the better option.

You'll need to consider factors like depreciation, maintenance costs, and insurance premiums to make an informed decision.

And don't forget to shop around for insurance quotes. You can save hundreds, even thousands, of dollars per year by comparing rates from different insurance companies.

FAQs

#### What is the average annual premium for an EV?

The average annual premium for an EV is around $1,674, according to a study by the National Association of Insurance Commissioners.

#### Can I get a discount on my EV insurance policy?

Yes, many insurance companies offer discounts for EV owners, such as discounts for low mileage or good driving records. For example, State Farm offers a discount for EV owners who drive fewer than 7,500 miles per year.

#### What is the difference between a personal and commercial EV insurance policy?

A personal EV insurance policy covers your vehicle for personal use, while a commercial EV insurance policy covers your vehicle for business use. If you use your EV for both personal and business purposes, you may need to purchase a commercial policy.

#### How can I save money on my EV insurance policy?

You can save money on your EV insurance policy by shopping around for quotes, choosing a higher deductible, and taking advantage of discounts offered by insurance companies.

#### What is gap insurance, and do I need it?

Gap insurance covers the difference between the actual cash value of your vehicle and the amount you owe on your lease or loan. If you lease an EV, you may be required to purchase gap insurance.

#### Can I insure my EV with a traditional insurance policy?

Yes, many traditional insurance companies offer EV insurance policies. However, you may be able to find better rates and coverage options with a specialized EV insurance company.

As a self-employed EV owner, it's essential to carefully review your insurance policy and make sure it covers all of your business use. Consider purchasing a policy that includes roadside assistance and rental car coverage, in case you need to rent a vehicle while your EV is being repaired.

And remember, EV lease vs buy insurance is a crucial consideration for self-employed and freelance EV owners. By weighing the pros and cons of each option and shopping around for insurance quotes, you can make an informed decision and save money on your premiums.

Until next time — Alex