OK so someone DM'd me this question: 'Alex, I just got a Tesla Model 3 and I'm trying to figure out my insurance. I've heard that the deductible can make a huge difference in my premium. Is that true?' Well, yeah... that's an understatement. The deductible is one of the most critical factors in determining your EV insurance premium. And, let's be real, who doesn't want to save money on their insurance? I mean, it's not like we're made of money, right? So, I'm gonna break it down for you - how to save money on EV insurance by finding your deductible sweet spot.

Tease: The $1,000 Deductible Disaster

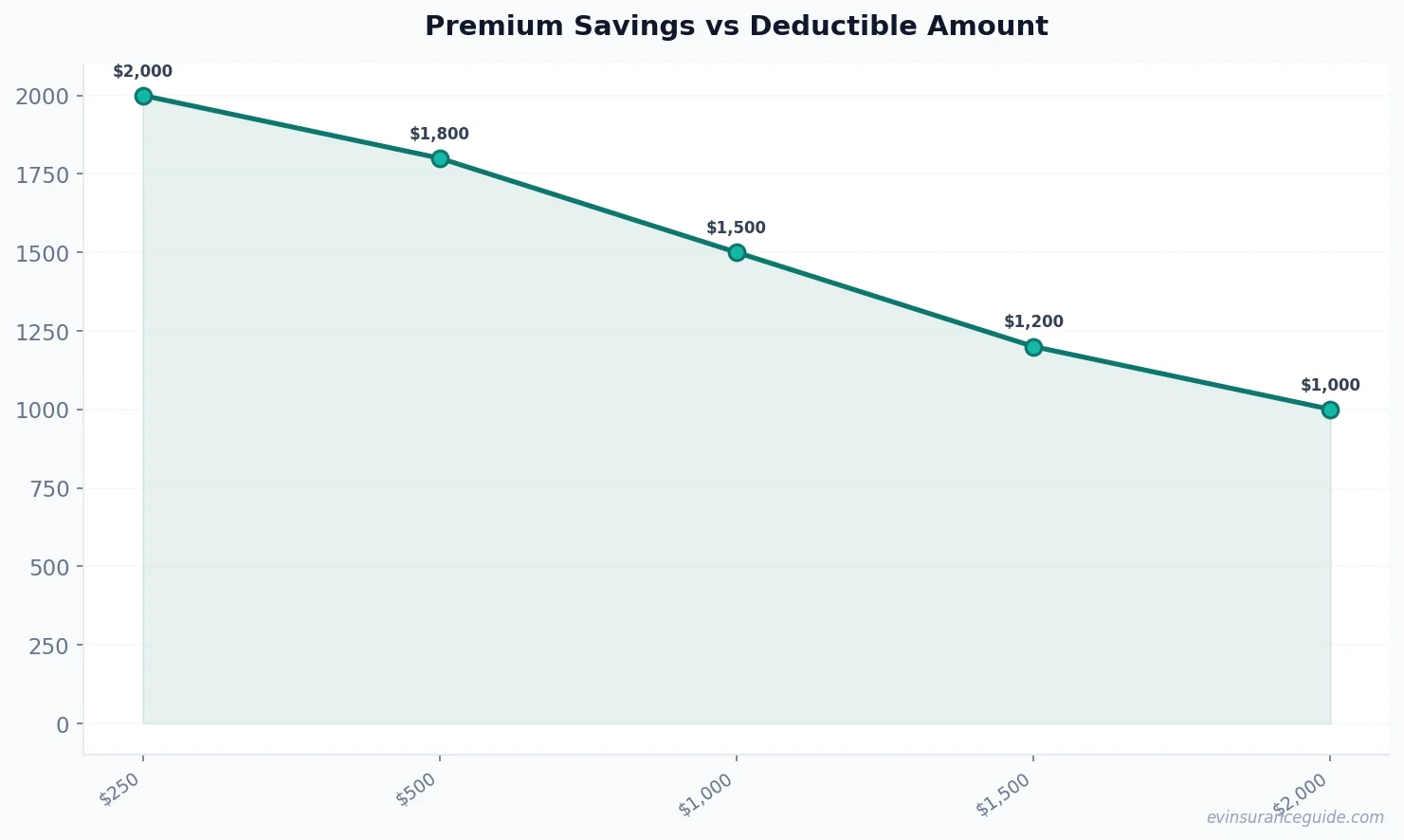

I've got a friend, let's call him Dave, who bought a brand new BMW iX and opted for a $1,000 deductible. He thought it was a good idea at the time, but boy was he wrong. His premium ended up being $2,500 per year, which is crazy high. And, when he got into a fender bender, he had to shell out $1,000 out of pocket. Ouch. That one stung. Know what the kicker is? If he had opted for a $500 deductible, his premium would've only been $2,000 per year. That's a $500 savings right there. Wild, right? So, yeah, the deductible can make a huge difference.

But, here's the thing - a lower deductible doesn't always mean a higher premium. It depends on the insurance company, the type of EV you have, and a bunch of other factors. For example, if you have a Hyundai Ioniq 5, you might be able to get away with a higher deductible and still have a relatively low premium. On the other hand, if you have a Rivian, you might need to opt for a lower deductible to keep your premium in check. And, let's not forget about the insurance company - some companies, like Geico, offer lower premiums for higher deductibles, while others, like Progressive, might not.

Compare: EV Insurance Deductibles vs Gas Guzzlers

So, how do EV insurance deductibles compare to those of gas guzzlers? Well, it's not exactly apples to apples, but I'll give you a rough idea. For a gas-powered car, a $500 deductible is pretty standard. But, for an EV, you might be able to get away with a $1,000 or even $1,500 deductible. And, in some cases, that can actually lower your premium. For example, I know someone who has a Tesla Model Y with a $1,500 deductible and their premium is only $1,800 per year. That's a steal, if you ask me. But, on the other hand, if you have a high-end EV like a Porsche Taycan, you might need to opt for a lower deductible to keep your premium from skyrocketing.

Now, I know what you're thinking - what about the insurance companies? Do they all offer the same deductible options? Nope. Each company has its own set of deductible options, and some are more flexible than others. For example, State Farm offers deductibles ranging from $250 to $2,000, while Allstate offers deductibles ranging from $100 to $1,000. So, it's worth shopping around to find the company that offers the best deductible options for your EV.

Myth Buster: You Need a Low Deductible for Comprehensive Coverage

OK, so here's a myth that needs busting - you need a low deductible for comprehensive coverage. Not true. Comprehensive coverage is a separate animal from collision coverage, and the deductible for one doesn't necessarily affect the other. For example, you could have a $1,000 deductible for collision coverage, but a $500 deductible for comprehensive coverage. And, in some cases, that can actually save you money. For example, if you live in an area prone to hail storms, you might want to opt for a lower comprehensive deductible to protect your EV from hail damage.

But, let's get real - comprehensive coverage is not just about hail damage. It's also about theft, vandalism, and other types of damage that aren't related to collisions. So, you need to think carefully about your comprehensive deductible and how it fits into your overall insurance strategy. And, don't even get me started on the importance of reading the fine print. I mean, it's not like insurance companies are trying to trick you or anything, but... actually, yeah, they kind of are. So, you gotta stay vigilant and make sure you understand what you're getting into.

Pro tip: Always read the fine print and understand what's covered and what's not. It's better to be safe than sorry, especially when it comes to your EV insurance.

Honest Opinion: Don't Skimp on Coverage

Look, I'm gonna give it to you straight - don't skimp on coverage. I know it's tempting to opt for a higher deductible to save money on your premium, but trust me, it's not worth it. You need to make sure you have enough coverage to protect your EV in case something goes wrong. And, if you're not sure what that means, then you need to do some research and figure it out. I mean, it's not rocket science, but it does require some effort. So, don't be lazy and just opt for the cheapest option. Take the time to understand your coverage options and make an informed decision.

For example, let's say you have a Rivian with a $1,000 deductible and you get into a serious accident. If you don't have enough coverage, you could be on the hook for thousands of dollars in damages. And, let's not forget about the potential long-term consequences of underinsuring your EV. I mean, it's not just about the money - it's about your safety and the safety of others on the road. So, yeah, skimping on coverage is not a good idea.

Question: How Low Can You Go?

So, how low can you go with your deductible? Well, that depends on a few factors, including your EV's value, your driving history, and your budget. But, as a general rule of thumb, you should aim for a deductible that's around 1-2% of your EV's value. So, if you have a Tesla Model 3 that's worth $50,000, you should aim for a deductible of around $500-$1,000. And, don't forget to consider your emergency fund - you should have enough savings to cover your deductible in case something goes wrong.

But, what if you're on a tight budget? Can you still afford to insure your EV? Yeah, it's gonna be tough, but it's not impossible. You can look into low-cost insurance options, like liability-only coverage, or you can shop around for discounts. For example, some insurance companies offer discounts for good grades, military service, or even just for being a good driver. So, yeah, it's worth doing some research and seeing what's out there.

FAQs

#### What is the average deductible for EV insurance?

The average deductible for EV insurance is around $500-$1,000, depending on the insurance company and the type of EV you have. But, it's worth noting that some insurance companies offer lower deductibles for certain types of EVs, like the Tesla Model 3.

#### Can I change my deductible after I've already purchased insurance?

Yeah, you can usually change your deductible, but it might affect your premium. So, it's worth checking with your insurance company to see what the deal is. And, don't forget to read the fine print - you don't want to get caught off guard by any unexpected changes to your policy.

#### How does my credit score affect my deductible?

Your credit score can affect your deductible, as well as your premium. If you have a good credit score, you might be able to qualify for a lower deductible. But, if you have a bad credit score, you might be stuck with a higher deductible. So, yeah, it's worth keeping an eye on your credit score and trying to improve it if you can.

#### What is the difference between collision and comprehensive coverage?

Collision coverage covers damage to your EV in the event of a collision, while comprehensive coverage covers damage from other sources, like hail or theft. So, yeah, they're two different types of coverage, and you need to understand the difference.

#### Can I get a discount for having a good driving record?

Yeah, you can usually get a discount for having a good driving record. Some insurance companies offer discounts for good grades, military service, or even just for being a good driver. So, yeah, it's worth asking about discounts when you're shopping for insurance.

#### How does the type of EV I have affect my deductible?

The type of EV you have can affect your deductible, as well as your premium. For example, if you have a high-end EV like a Porsche Taycan, you might need to opt for a lower deductible to keep your premium from skyrocketing. But, if you have a more affordable EV like a Hyundai Ioniq 5, you might be able to get away with a higher deductible.

That's my two cents. Take it or leave it — but I hope it helps. — Alex