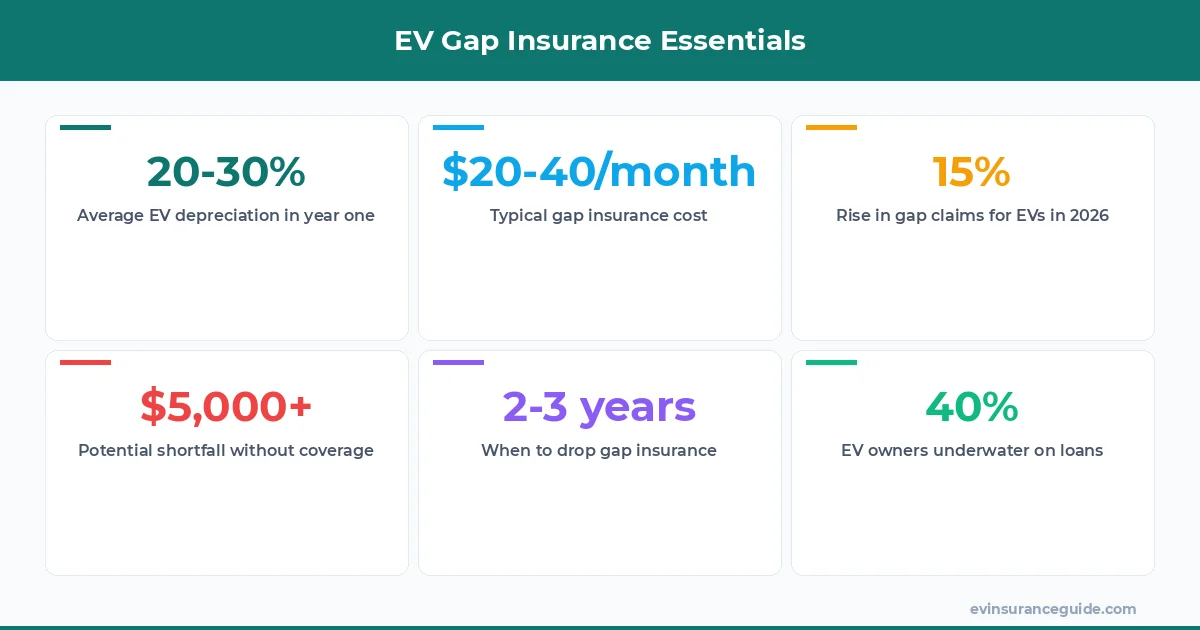

Hold up—did you catch that? EV insurance rates just spiked again in 2026, thanks to wild depreciation hits on models like the Tesla Model 3 and Hyundai Ioniq 5. Manufacturers are pushing out new tech faster than ever, making last year's EVs drop like rocks. We're talking 20-30% value loss in the first year alone, which means if you're financing one of these babies, you could owe thousands more than it's worth after a fender bender. That's right, 'should I get gap insurance for my EV' isn't just a casual question anymore—it's a 2026 emergency. I mean, picture this: you total your BMW iX on day 365, and the insurer pays out based on its plummeted market value, leaving you with a loan balance that stings like a bad breakup. New data from insurers like Progressive shows gap claims jumping 15% year-over-year for EVs, forcing folks to rethink their coverage. And here's the kicker—dealers are hiking add-on fees, so if you're leasing or buying with a loan, skipping gap could leave you high and dry. Yeah, I know, another insurance rant, but trust me, this one's gonna save you headaches. We're not messing around; 2026 is the year EV owners need to get savvy or get burned.

WARNING: The Sneaky Depreciation Trap That's Eating Your Equity Don't fall for it—thinking your EV will hold value like a classic car is a massive mistake. That Tesla Model 3 you financed for $40,000? It's worth maybe $28,000 after 12 months, and if you crash it, you're on the hook for the difference. Gap insurance bridges that chasm, but skipping it means you're basically handing over your wallet to the bank. Know what the kicker is? Some dealers bury extra fees in the fine print, tacking on 5-10% to your loan just for the policy. And that's before you realize how fast EVs like the Rivian depreciate in a flooded market.

Take Sarah, a real estate agent I know who bought a Hyundai Ioniq 5 last year—she thought her comprehensive policy covered everything. Wrong. When she totaled it early, she owed $5,000 more than the payout, and that debt lingered like a bad habit. Rhetorical question: How would you feel owing money on a car that's scrap metal? Exactly. So, for anyone asking 'should I get gap insurance for my EV', the answer's a hard yes if you're underwater on your loan. We're not sugarcoating it; this trap has cost people thousands in 2026 alone.

But wait, there's more—avoid the hidden costs by comparing providers like Geico or State Farm, where standalone gap policies run $20-40 a month without the dealer markup. I remember haggling with adjusters over similar cases; it gets ugly fast. Bottom line: Don't let depreciation steal your peace; cover that gap before it's too late.

5 Key Moments to Grab Gap Insurance and Dodge the Debt Five—that's how many critical points I'll hit on when 'should I get gap insurance for my EV' turns from maybe to must. First off, right after you sign for a new Tesla Model Y with a loan over 80% of its value; that's prime time for a gap policy to kick in. Second, if you're leasing anything like the BMW iX, because leases amplify depreciation risks—think about returning a car worth less than what you owe.

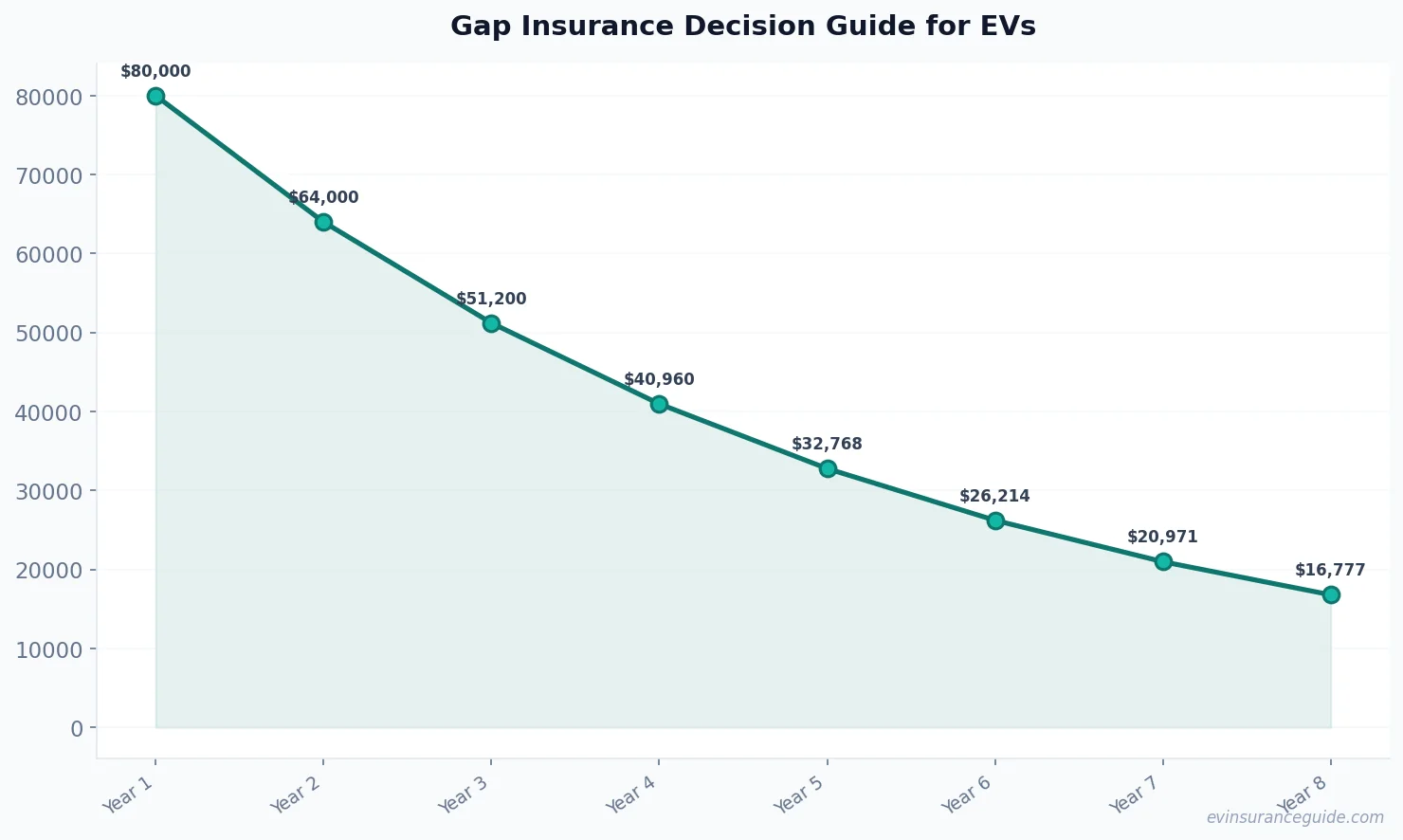

Third, during that initial 24 months when your EV's value tanks hardest; data from Kelley Blue Book shows Hyundai Ioniq 5 losing 25% in year one alone. Fourth, before any big road trips—I've seen Rivian owners hit potholes and face massive shortfalls without coverage. And fifth, when rates are low, like the $20-40 monthly deals from Allstate that won't break the bank. Rhetorical question: Why wait until you're upside down on payments to fix this?

OK, let's get specific—Progressive offers gap for as little as $15 extra on your premium, but only if you bundle early. That's a steal compared to paying out of pocket for the difference, which could hit $10,000 for a totaled EV. Strong opinion: If you're not locking this in at purchase, you're playing roulette with your finances. We've all heard stories of folks regretting it; don't be that person in 2026.

HONEST_OPINION: Gap Insurance Is Overkill for Some, But a Lifesaver for the Rest Look, I'm not gonna lie—gap insurance is overpriced trash if your loan's already below your EV's value, like after three years on a Hyundai Ioniq 5 that's held steady. But for the majority? It's a no-brainer. That 20-30% depreciation hit on new EVs means most owners are staring down a gap wider than the Grand Canyon, and pretending otherwise is just delusional. If you're financing a Tesla Model 3, coughing up $20-40 a month beats owing $5,000 post-accident any day.

Rhetorical question: Why risk it when the cost is peanuts compared to the potential fallout? Data from J.D. Power shows 40% of EV owners with loans are underwater in year one, so yeah, I'm taking sides—get it if you owe more than the car's worth. Dealers push their versions with hidden markups, insurers like Liberty Mutual offer cleaner deals, and standalone policies from specialists are the sweet spot. Hmm, let me rethink that—for leased EVs, it's even more crucial, as I've seen folks hit with early termination fees that add insult to injury.

Strong opinion: Skip the dealer gap; it's a rip-off with fees up to 3% of your loan. Go for the insurer's option instead—it's straightforward and cheaper. And if you're wondering 'should I get gap insurance for my EV', the answer's yes until that loan balance dips below market value, usually around year two or three for models like the Rivian.

OK So Here's the Deal With Dealer Gap vs. Insurer Gap vs. Standalone Casual direct: Let's cut the fluff—dealer's gap insurance is like buying from a pushy salesperson; it's convenient but loaded with extras that jack up your costs. For instance, a BMW iX buyer might pay $500 upfront through the dealer, only to find it's not as comprehensive as a standalone policy from a company like Esurance, which runs $200-300 for the whole term. Insurer gap, tied to your main policy, is middling—good for Tesla Model 3 owners who already have coverage, but it can add sneaky deductibles.

Rhetorical question: Why settle for middle ground when standalone gives you flexibility without the baggage? I mean, for a Hyundai Ioniq 5, standalone from third-parties is about $15/month and cancels easily once you're equity-positive. That's the real win—total control. And don't forget, 2026 brings new regulations making insurer options more transparent, so shop around before committing.

Bottom line: If you're debating 'should I get gap insurance for my EV', weigh the pros—dealer's fast but pricey, insurer's integrated but rigid, standalone's independent and often cheapest. I've switched clients to standalone and watched their savings add up; it's that simple.

STORY_TEASE: The One Time Gap Saved My Buddy's Bacon Tease this: Imagine Mike, a tech bro with a Rivian, who thought he was set until a storm totaled his ride—spoiler, gap insurance turned a disaster into a minor headache. We'll unpack how in a bit, but first, let's hit the FAQs because I know you're curious.

Is gap insurance necessary for all EVs? Nope, it's only crucial if you're financing or leasing and owe more than the car's worth. For a Tesla Model 3, that might mean the first two years, but after that, you're probably good to drop it. Data shows EVs depreciate faster than gas cars, so always check your loan balance first—it's a quick way to avoid unnecessary costs.

How much does gap insurance cost for a Hyundai Ioniq 5? Typically, it's $20-40 per month, depending on your insurer like State Farm, but factors like your credit score can tweak that. That's a small price for peace if you're underwater on payments, as it covers the difference up to the loan amount. Rhetorical question: Would you rather pay that or thousands out of pocket?

When should I drop gap insurance on my EV? Once your loan is less than the car's current value, usually after 2-3 years for models like the BMW iX. I recommend checking annually with tools from Kelley Blue Book to confirm. Skipping it too early could leave you exposed, but hanging on too long is just wasting money.

Does gap insurance cover leased EVs? Absolutely, and it's often mandatory in leases to protect the lessor. For a Rivian lease, it bridges the gap between the residual value and what you owe, saving you from mileage penalties or early termination fees. Strong opinion: If you're leasing, don't skip this—it's non-negotiable.

Is dealer gap insurance better than from my insurer? Not usually; dealer's is convenient but pricier with markups, while your insurer's might integrate seamlessly. For 'should I get gap insurance for my EV' scenarios, I'd pick the insurer's option for Tesla owners to keep things simple. Either way, compare costs—it's worth it for the savings.

Can gap insurance be added later? Yeah, but it's easier at purchase; adding it midway with companies like Geico could mean higher rates or restrictions. If your EV's already depreciated, you might not qualify, so act fast if you're thinking about it. That's a pro tip right there—don't delay and regret it.

What's the average EV depreciation in 2026? Experts predict 20-30% in the first year for popular models, based on recent trends from J.D. Power. That means for a $50,000 Hyundai Ioniq 5, you're looking at a $10,000-15,000 hit, making gap a smart hedge. Always factor that into your 'should I get gap insurance for my EV' decision.

And just like that, we're wrapping this up. If you're on the fence about 'should I get gap insurance for my EV', remember: it's not about fear-mongering; it's about smart moves in a volatile market. Go compare those policies, crunch the numbers, and drive easy. Cheers from the EV insurance trenches. — Alex

Pro tip: Always review your loan-to-value ratio yearly—it's the easiest way to know when to ditch gap insurance and save cash.