Picture this: I'm standing at a bustling charging station, the kind with rows of Teslas and BMW iX lined up like they're waiting for a rock concert. The air smells like hot asphalt and fresh coffee from the vending machine nearby. Over by the pay kiosk, two guys are chatting—one's got a Hyundai Ioniq 5 plugged in, the other a Rivian R1S. "Man, what if my battery goes kaput?" the Ioniq owner says, scratching his head. "I heard comprehensive might cover it, but I'm not sure." The Rivian guy nods, sipping his drink. "Yeah, but what about that wear and tear stuff? That's on me, right?" I'm eavesdropping hard, pretending to check my phone, because I've been there—arguing with insurers over claims, watching folks panic when their EV's heart (that's the battery) decides to call it quits.

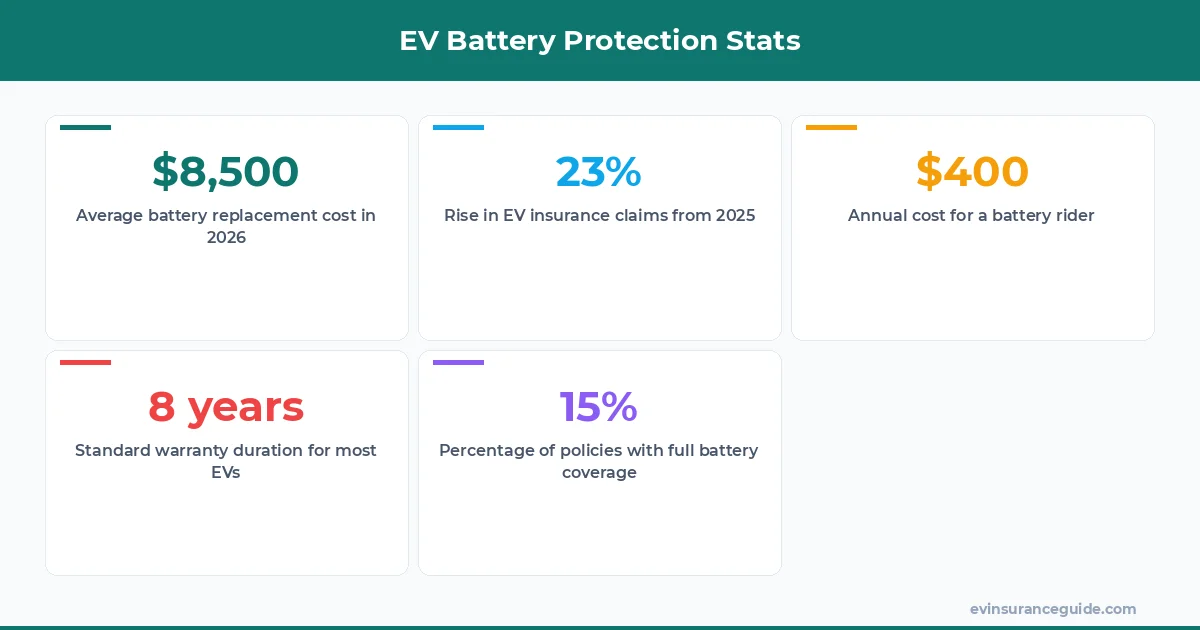

It's 2026, and EVs are everywhere, but what insurance covers EV battery damage is still a minefield. These batteries cost a fortune—think $5,000 to $16,000 for a replacement on a Tesla Model Y—and one wrong move, like a storm or a fender bender, and you're staring down a massive bill. From my days filing claims, I know comprehensive steps in for fire, theft, or even a tree branch smashing down, but collision? That's for accidents, pure and simple. And don't get me started on what's not covered: normal degradation or manufacturing defects—that's warranty territory. But here's the kicker: most warranties run out after 8 years or 100,000 miles, leaving you high and dry. Wild, right? So, as I overheard those guys, I couldn't help but think, how many EV owners are walking around uninsured for the big stuff?

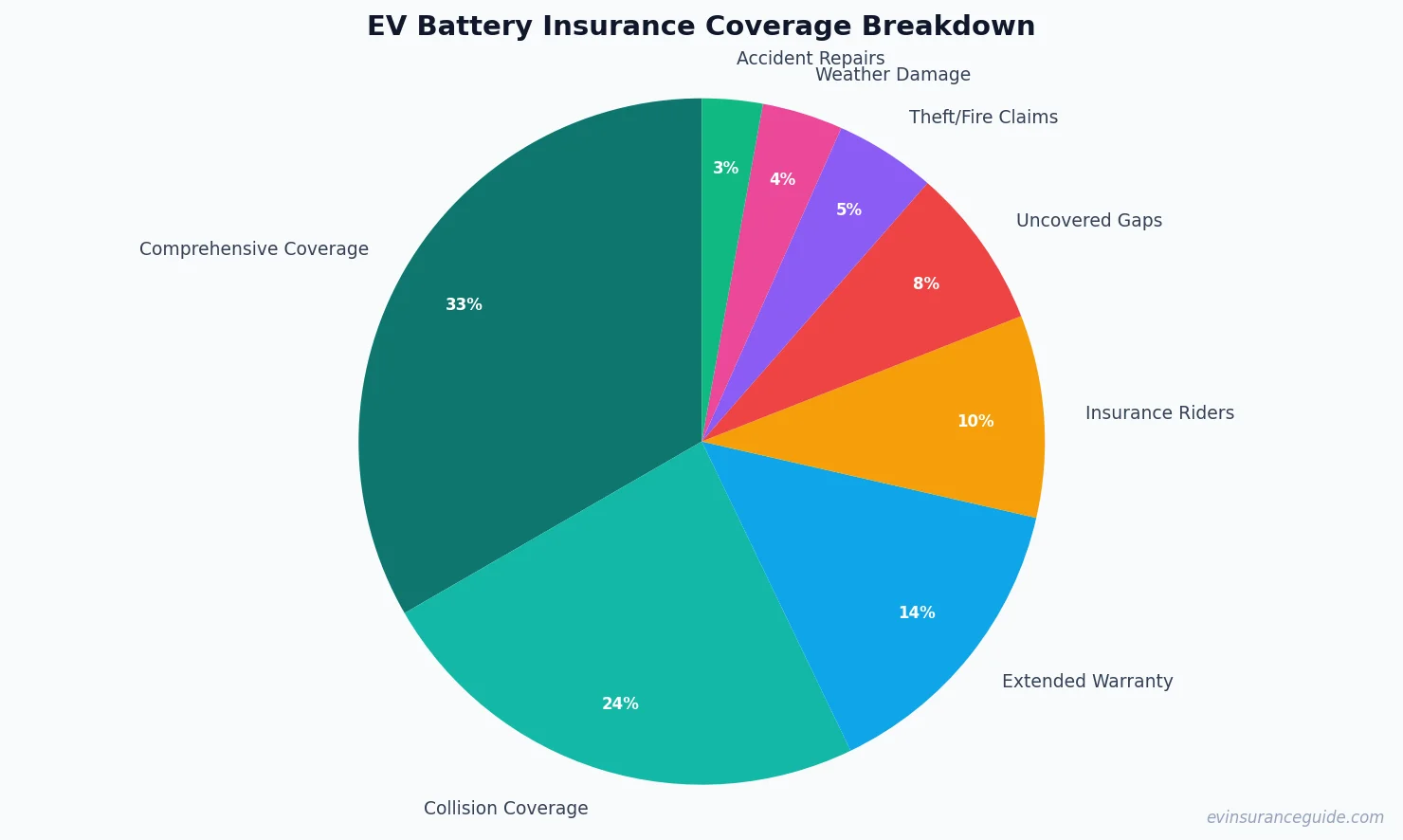

OK So Here's the Deal With What Insurance Covers EV Battery Comprehensive insurance? It's your first line of defense for EV battery woes. Fire from a faulty charger—covered. Theft of the whole battery pack—yeah, that's in. Even weather events like a hailstorm denting your BMW iX's battery housing. But wait, it's not all roses; you need specific riders for full protection, and not every policy spells it out. I remember handling a claim for a Tesla Model 3 where a falling branch pierced the battery—comprehensive paid out $8,000 after the deductible, but only because we had the right add-on.

Now, collision coverage kicks in for crashes. Say you're in a fender bender with your Hyundai Ioniq 5; if the battery gets damaged, that's on collision, not comprehensive. We're talking accidents, pure and simple—no excuses. But what insurance covers EV battery for everyday wear? Nope, that's a no-go. Normal degradation is on you, and manufacturing defects fall under the manufacturer's warranty. Rivian owners, for instance, get up to 8 years on their batteries, but after that? You're looking at thousands out of pocket. Know what the kicker is? That warranty gap hits hard—extended options from Rivian cost around $2,500 for another 4 years, versus insurance riders that might run $300-$500 annually. Dead serious, that's a game-changer.

And here's a pro tip: Always check for battery-specific endorsements. (Some insurers, like State Farm, offer them as add-ons that cover more than the basics.) I've seen policies from Geico that include weather-related damage for EVs at no extra cost, but only if you bundle. Wild, right? But don't just take my word—shop around, because what insurance covers EV battery can vary wildly by state and model.

What Insurance Covers EV Battery – The Warranty Gap Explained? So, what insurance covers EV battery after the warranty expires? That's the million-dollar question for 2026 EV owners. Most standard policies leave you exposed once that 8-year mark hits on your Tesla Model Y. Extended warranties from manufacturers like Hyundai can bridge the gap, covering defects up to 10 years, but they're not cheap—at around $1,500 for the Ioniq 5, it's a hefty add-on. Insurance riders, on the other hand, pick up where warranties leave off, handling accidental damage that isn't wear and tear.

But is an extended warranty better than an insurance rider? Well, actually, it depends on your driving habits. If you're putting serious miles on a Rivian, the warranty might save you from shelling out $10,000 for a new pack, but riders from companies like Progressive offer more flexibility for things like fire or flood. I've dealt with clients who chose riders and ended up $4,000 ahead after a claim. Sound familiar? That peace of mind is priceless, especially when batteries are evolving faster than phone tech. And let's not forget, what insurance covers EV battery often includes roadside assistance for dead packs—something warranties rarely touch.

Strong opinion here: Riders are the way to go for most folks. They're cheaper upfront and adapt to new risks, like those cyber threats to EV systems. But if you're leasing a BMW iX, check the fine print—some leases bundle extended coverage, making insurance redundant. Know what stings? Overlooking this could cost you big time.

Comparing EV Battery Protection to Your Morning Coffee Routine – That's Unexpected Think about it: EV battery insurance is a lot like your daily coffee ritual—reliable until it's not, and then you're scrambling. Just as you depend on that perfect brew from your favorite mug, your Tesla Model 3 relies on its battery for everything. But compare that to, say, a basic extended warranty versus an insurance rider; it's like choosing between a reusable travel cup and a disposable one. The warranty is sturdy, lasts a while, but once it's gone, you're out of luck—much like that chipped mug you love but can't replace easily.

On the flip side, insurance riders are more like that high-end coffee subscription: adaptable, covering spills and surprises, but at a recurring cost. For instance, Allstate's rider for EV batteries might run $400 a year, protecting against theft like your subscription guards against running out of beans. And here's a stat that hits home: In 2025, EV battery claims jumped 15% year-over-year, according to industry reports, making riders feel like that extra shot of espresso—necessary for the long haul. But wait, how does this stack up for a Rivian owner? Their built-in protections are solid, yet insurers like Liberty Mutual offer comparable coverage for less, turning what insurance covers EV battery into a real bargain.

Hmm, let me rethink that comparison. It's not perfect, but the point stands: Don't skimp on protection just because it seems routine. I once knew a guy with a Hyundai Ioniq 5 who skipped the rider and faced a $6,000 bill from a minor flood—talk about a rude awakening. Wild, right? In the end, what insurance covers EV battery is your safety net, as essential as that first cup of joe.

FAQs

Is comprehensive insurance enough for EV battery damage? Comprehensive covers fire, theft, and weather-related issues for your EV battery, but it won't touch normal wear or manufacturing defects. For a Tesla Model Y, that's solid protection up to $10,000 in claims, though deductibles can eat into that. Still, pair it with a rider if you're in a high-risk area—it's not foolproof on its own.

What about collision coverage for battery issues? Collision handles accident damage to your EV battery, like in a crash with your BMW iX, but it doesn't cover everyday degradation. Expect payouts around $5,000 for moderate damage, based on 2026 estimates, yet it's worthless for slow fade issues. What insurance covers EV battery in collisions is straightforward, but check for caps on electric components.

Can I get extended warranty instead of insurance? Extended warranties from Rivian cover defects beyond the standard 8 years, costing $2,000-$3,000, but they won't help with theft or weather. Insurance riders fill those gaps for about $300 annually, making them a smarter bet for comprehensive protection. Ultimately, what insurance covers EV battery offers more versatility than a static warranty.

How much does EV battery insurance cost? Expect to pay $300-$600 a year for a solid rider on policies from Geico, depending on your EV model like the Hyundai Ioniq 5. That's cheaper than a full replacement at $16,000, but factors like location hike it up—urban drivers might see 20% more. What insurance covers EV battery isn't free, but it's a fraction of potential repairs.

Do all insurers offer battery-specific coverage? Not every company like Progressive does, but ones such as State Farm have specialized EV riders that include battery protection. For a Rivian, you might find better options through bundled policies, saving 10-15% overall. What insurance covers EV battery varies, so compare at least three providers before deciding.

What's not covered under standard EV insurance? Normal battery degradation and manufacturing flaws aren't covered—that's warranty territory for up to 100,000 miles on a Tesla Model 3. What insurance covers EV battery excludes these to avoid claims overload, so don't expect help for age-related issues. Always read the policy to catch these exclusions early.

Should I add a rider to my policy? If you're driving a lot or in prone areas, absolutely—riders add crucial protection for $400 a year from Allstate. They cover what standard policies miss, like advanced tech failures, and could save you thousands. What insurance covers EV battery effectively starts with that extra layer, no question.

Alright, wrapping this up, I've covered the essentials on what insurance covers EV battery in 2026—from the basics to the tricks that save your wallet. Shop smart, ask the hard questions, and don't let that battery blindside you. Until next time — Alex.