I'm sipping coffee at a charging station, listening in on a conversation between two EV owners — Rachel and Mike. They're discussing their Tesla insurance cost, and Rachel mentions how she almost got stuck with a huge bill after her Model 3 was totaled. Mike asks, 'Didn't you have gap insurance?' Rachel replies, 'Nope, I didn't think it was necessary... that one stung.'

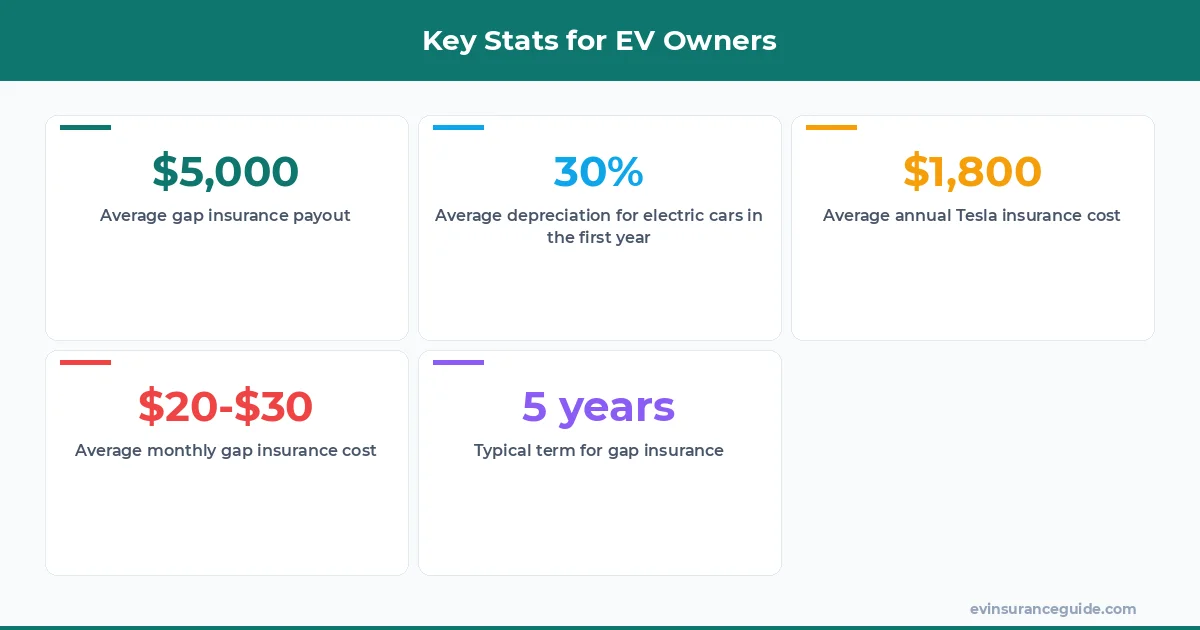

Know what the kicker is? Gap insurance could've saved Rachel around $5,000. That's the difference between the car's actual cash value and the outstanding loan balance. Wild, right? This got me thinking — how many EV owners are unaware of the importance of gap insurance? Sound familiar? You've probably heard stories like this before, but let's break it down.

WARNING — Hidden Costs in EV Insurance

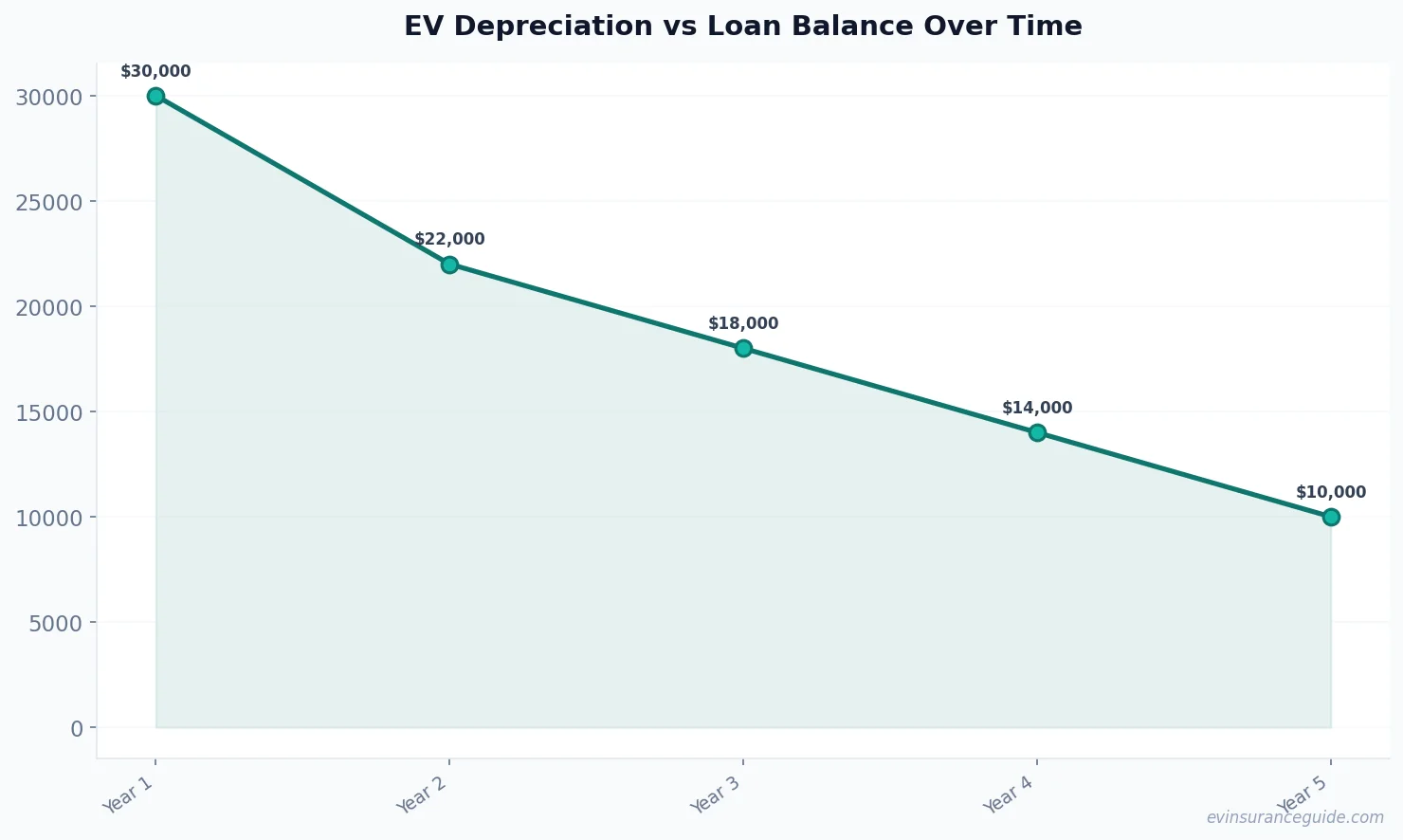

When you buy an electric car, the depreciation hits hard. I mean, we've all seen how quickly EVs lose their value. For instance, a Tesla Model Y can depreciate by around 30% in the first year alone. That's a significant drop, and it's gonna leave you with a loan balance that's higher than the car's actual worth. And, well, actually, this is where gap insurance comes in. It's designed to cover that difference, so you don't end up owing more on the loan than the car is worth.

But, here's the thing: not all gap insurance policies are created equal. Some might have exclusions or limitations that'll leave you high and dry. For example, if you've made any modifications to your car, like adding a fancy sound system or performance upgrades, your gap insurance might not cover those. You'll wanna check the policy terms carefully before signing up. And, let's be real, reading policy documents can be a snooze-fest, but it's crucial.

Now, let's look at some numbers. The average Tesla insurance cost for a Model 3 is around $1,800 per year. But, if you add gap insurance to that, you're looking at an additional $20-$30 per month. That's a small price to pay for the peace of mind that comes with knowing you're protected against depreciation.

HONEST_OPINION — Tesla Insurance Cost and Gap Coverage

Honestly, I think gap insurance is a no-brainer for EV owners. The depreciation is just too steep, and the risk of owing more on the loan than the car is worth is too high. And, let's not forget, Tesla insurance cost is already pretty steep. Adding gap insurance to that might seem like a luxury, but trust me, it's worth it. I mean, would you rather pay an extra $20-$30 per month for gap insurance or risk owing thousands of dollars if your car gets totaled?

For instance, if you're financing a BMW iX, which can cost upwards of $80,000, you'll wanna make sure you've got gap insurance to cover that loan balance. The last thing you want is to be stuck with a huge bill because the car's depreciation left you owing more on the loan than it's worth. And, yeah, I know, another insurance article. But hear me out — this is crucial stuff. You don't wanna end up like Rachel, stuck with a huge bill and no way to pay it.

Now, I know some of you might be thinking, 'But Alex, I've got a good driving record, and I'm careful with my car. I don't need gap insurance.' Well, actually, that's not entirely true. Gap insurance isn't just about protecting yourself against accidents or theft; it's also about protecting yourself against depreciation. And, let's be real, depreciation is unpredictable. You can't control how quickly your car loses its value, but you can control whether or not you've got gap insurance to cover that.

STORY_TEASE — My Friend's Gap Insurance Nightmare

I've got a friend, let's call him Dave, who bought a Rivian R1T without gap insurance. He thought he was saving money, but boy, was he wrong. When his car got totaled, he was left owing over $10,000 on the loan. That's a pretty scary number, especially when you're not expecting it. And, well, actually, that's when I realized how important gap insurance is. You don't wanna end up like Dave, stuck with a huge bill and no way to pay it.

But, let me tell you, Dave's story isn't unique. There are plenty of people out there who've been stuck with huge bills because they didn't have gap insurance. And, yeah, it's a tough lesson to learn, but it's one that'll save you thousands of dollars in the long run. So, don't be like Dave; get gap insurance and protect yourself against depreciation.

Pro tip: Always read the fine print on your gap insurance policy. You don't wanna find out that you're not covered when it's too late. And, trust me, it's better to be safe than sorry.

COMPARISON — Gap Insurance for Electric Cars vs Gas-Powered Cars

Now, let's compare gap insurance for electric cars to gap insurance for gas-powered cars. The thing is, electric cars depreciate way faster than gas-powered cars. I mean, we're talking 30-40% depreciation in the first year alone. That's a huge drop, and it's one that'll leave you owing more on the loan than the car is worth. Gas-powered cars, on the other hand, depreciate at a slower rate. So, if you're driving a gas-powered car, you might not need gap insurance as much. But, if you're driving an electric car, it's a whole different story.

For instance, if you're driving a Hyundai Ioniq 5, you'll wanna make sure you've got gap insurance to cover that loan balance. The car's depreciation is pretty steep, and you don't wanna end up owing more on the loan than it's worth. But, if you're driving a Toyota Camry, you might not need gap insurance as much. The depreciation is slower, and you're less likely to end up owing more on the loan than the car is worth.

MYTH_BUST — Gap Insurance is Only for New Cars

One myth that's out there is that gap insurance is only for new cars. That's just not true. Gap insurance can be beneficial for any car that's financed, regardless of its age. I mean, think about it — if you're financing a used car, you're still gonna be owed more on the loan than the car is worth if it gets totaled. And, yeah, the depreciation might not be as steep, but it's still gonna be a problem.

For example, if you're financing a used Tesla Model S, you'll still wanna make sure you've got gap insurance to cover that loan balance. The car's depreciation might not be as steep as a new car, but it's still gonna be a problem if it gets totaled. And, trust me, you don't wanna end up owing more on the loan than the car is worth.

FAQs

#### What is gap insurance?

Gap insurance is a type of insurance that covers the difference between the actual cash value of your car and the outstanding loan balance. It's designed to protect you against depreciation, so you don't end up owing more on the loan than the car is worth.

#### How much does gap insurance cost?

The cost of gap insurance varies depending on the provider and the type of car you're driving. On average, you can expect to pay around $20-$30 per month for gap insurance. But, hey, that's a small price to pay for the peace of mind that comes with knowing you're protected against depreciation.

#### Can I buy gap insurance from any provider?

No, you can't buy gap insurance from just any provider. You'll need to check with your insurance company to see if they offer gap insurance, and what the terms are. Some providers might have exclusions or limitations that'll leave you high and dry, so make sure you read the fine print carefully.

#### Is gap insurance required by law?

No, gap insurance is not required by law. However, it's highly recommended if you're financing a car. I mean, think about it — if you're financing a car, you're already taking on a significant amount of risk. Gap insurance can help mitigate that risk and protect you against depreciation.

#### How long does gap insurance last?

Gap insurance typically lasts for the term of the loan. So, if you've got a 5-year loan, your gap insurance will last for 5 years. But, hey, that's plenty of time to protect yourself against depreciation.

#### Can I cancel gap insurance at any time?

Yes, you can cancel gap insurance at any time. But, keep in mind that you might not get a refund for the premiums you've already paid. So, make sure you think carefully before canceling your gap insurance.

#### Do all cars depreciate at the same rate?

No, not all cars depreciate at the same rate. Electric cars, for instance, depreciate way faster than gas-powered cars. I mean, we're talking 30-40% depreciation in the first year alone. That's a huge drop, and it's one that'll leave you owing more on the loan than the car is worth.

The best policy is the one you actually understand. — Alex