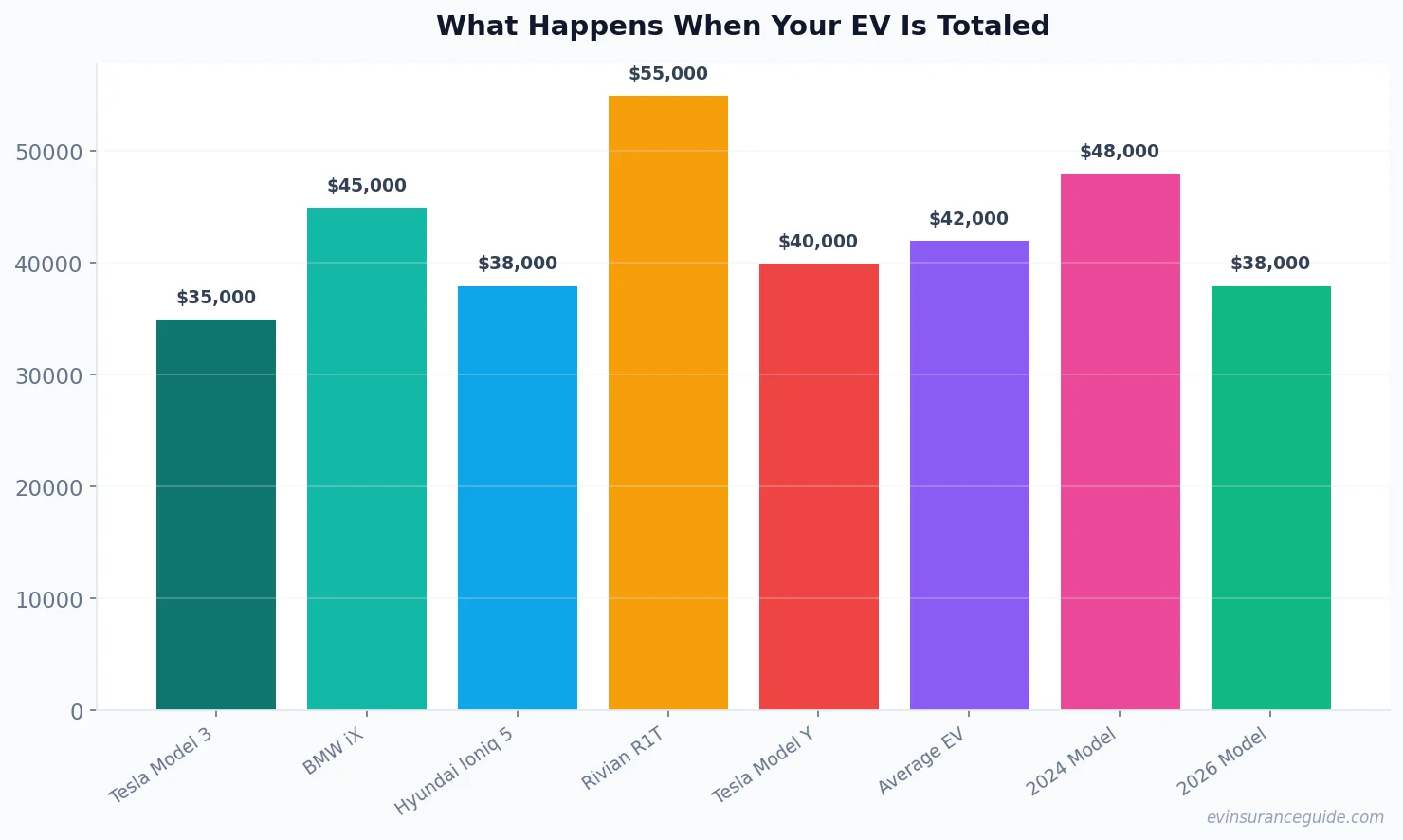

EV insurance isn't the hero you think it is—it's a rigged game that leaves you holding the bag when your ride gets crunched. Take a Tesla Model 3, for instance; you buy it thinking it's future-proof, but one fender-bender in 2026 could turn it into scrap, and you're staring at a payout that barely covers the loan. That's the cold reality: insurers lowball EVs because batteries depreciate faster than a bad meme, and suddenly you're upside down on payments. I've seen folks lose thousands because they didn't see the curveball coming. And yeah, I'm calling it out—most guides gloss over how these policies are stacked against you, especially with rapid tech changes making your shiny BMW iX worth peanuts overnight. So, buckle up, because we're diving into what happens when your EV is totaled, and it's not pretty if you're not prepared.

Wild, right? But let's get real: in 2026, EVs like the Hyundai Ioniq 5 are pricier to insure due to battery woes, and if yours ends up in a wreck, the insurer's first move is to play hardball. That's why you need to know the drill, from inspection to salvage, or you're gonna regret it. I've argued with adjusters over Rivians that were deemed totaled for repairs costing just over 60% of value—it's maddening. OK, enough setup; let's break this down.

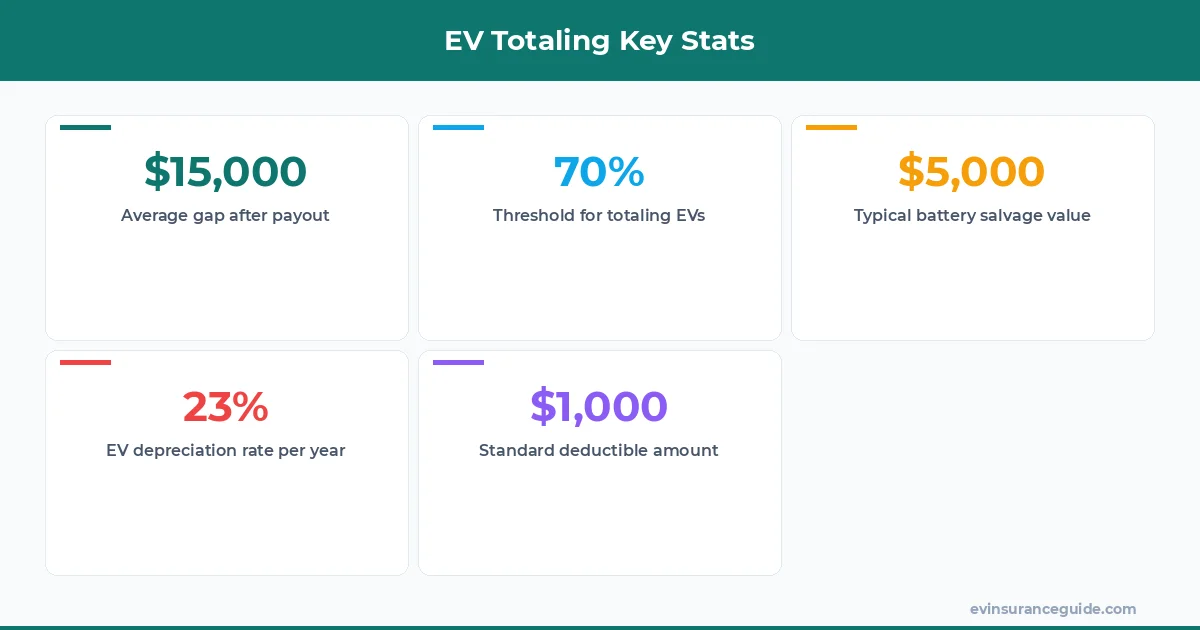

Warning: The Gap Insurance Trap That'll Nail You for $15K Don't fall for the myth that your standard policy covers everything when your EV is totaled—it's a trap that'll leave you owing more than you get. For a Tesla Model Y, insurers might payout $30,000 as actual cash value (ACV), but if you still owe $45,000 on the loan, that's a $15,000 gap staring you down. And here's the kicker: with EV values plummeting due to battery degradation, that gap widens faster than you can say "range anxiety." Know what really grinds my gears? Companies like Geico or State Farm slap on depreciation hits that feel arbitrary, turning your pride and joy into pocket change.

Picture this: you crash your BMW iX, and the repair estimate hits 70% of its value—bam, it's totaled. But without gap insurance, you're on the hook for the difference, and that's no joke in 2026 when EV loans are sky-high. I've heard from readers who skipped it and ended up selling plasma to cover the rest—harsh, but true. Rhetorical question: Why would anyone risk that when gap coverage costs as little as $200 a year? It's not optional; it's essential, especially for high-ticket EVs.

And let's not sugarcoat it—this policy is overpriced trash from some providers, but for EVs, it's the best defense you've got. A buddy of mine bought back his totaled Hyundai Ioniq 5 for $5,000 after the salvage auction, but only because he had gap insurance to bridge the gap. Strong opinion: Skip this, and you're basically inviting financial ruin; get it, and you're one step ahead of the game.

OK So Here's the Deal With What Happens When Your EV Is Totaled Alright, let's lay it out: when your EV is totaled, it starts with the insurer sending an adjuster to poke around, and that's where things get messy. For a Rivian, they might inspect the damage and decide if repairs exceed 50-80% of the vehicle's value—say, $40,000 on a $50,000 car—and boom, it's scrap. Then, you get your ACV payout minus the deductible, like $35,000 after a $1,000 hit, and off it goes to the salvage yard. Sounds straightforward, but trust me, it's not; insurers like Progressive lowball that ACV based on market fluctuations.

Ever tried haggling over a totaled Tesla? It's a headache. The process drags on, with them dragging their feet on inspections, and suddenly you're waiting weeks for a check. Why gap insurance is critical here: it picks up that $15,000 shortfall I mentioned, turning a disaster into a manageable bump. And if you want to keep your totaled EV, you can buy it back from the salvage auction—I've seen folks do it for around $10,000 on a Model 3—but good luck getting the battery salvage value factored in, which could add another $5,000 to your pot.

Hmm, let me rethink that—negotiating a higher payout is key, like pushing for $40,000 instead of $35,000 by showing comparable sales. For EVs in 2026, battery salvage value is a big deal; companies recycle them for minerals, so your wreck might be worth more than you think. Dead serious, this step-by-step crap is where most people drop the ball, but with a little fight, you can come out on top.

7 Sneaky Ways Insurers Calculate Your EV's Value Insurers aren't playing fair when they slap a number on your totaled EV, and that's seven ways they screw it up. First, they use databases like NADA or Kelley Blue Book to factor in mileage, condition, and that dreaded battery health— for a Hyundai Ioniq 5 with 30,000 miles, it might drop the value by 20%. Second, depreciation hits hard; EVs lose 30-50% in the first three years, so your 2026 model could be worth way less than you paid. Third, regional market data gets thrown in, like how West Coast prices for Teslas are higher than in the Midwest.

Know what the kicker is? They often ignore upgrades, like that $2,000 battery pack you added to your BMW iX, which is a total rip-off. Fourth, salvage value of the battery alone can be $3,000-$5,000, but good luck getting them to add it. Fifth, economic factors like inflation in 2026 might inflate costs, yet they cap your payout. Sixth, comparable sales data from auctions undervalues EVs because of the green tech stigma. And seventh, if it's a lease, they calculate differently, often leaving you with nothing.

That's infuriating, right? Strong opinion: This whole valuation game is biased trash, especially for EVs like the Rivian, where battery tech evolves so fast. A pro tip: Always demand a detailed breakdown—here's one in > Negotiate by comparing to real sales data; for instance, if similar Model Ys are selling for $45,000, don't settle for less than that minus 10% depreciation. Rhetorical question: Why should you accept their first offer when you can push back with facts? In my book, that's the only way to level the playing field.

FAQs

What's the first step when your EV is totaled? When your EV is totaled, the insurer inspects the damage first, determining if repairs exceed 50-80% of the value, like for a Tesla Model 3 where $25,000 in fixes on a $40,000 car seals its fate. Then, you get an ACV payout minus your deductible, say $35,000 after a $1,000 deduction. It's a raw deal, but knowing this lets you prepare for the fight ahead.

How do insurers decide if an EV is totaled? Insurers base it on repair costs versus the EV's value; for a BMW iX, if it's over 70%, it's totaled, often leading to a salvage send-off. Factors like battery damage play big, since replacing one can cost $15,000 alone. Don't let them rush you—question their math if it feels off.

Why might I owe more than the payout on my totaled EV? You could owe more because of the loan balance exceeding the ACV, like owing $50,000 on a Hyundai Ioniq 5 that's only worth $35,000 totaled. That's where gap insurance steps in, covering that $15,000 gap so you're not left bankrupt. It's a must-have in 2026's EV market.

Can I negotiate a higher payout for my totaled EV? Absolutely, by providing evidence of higher values, like recent Rivian sales data showing $10,000 more than their offer. Insurers like Allstate might budge if you highlight overlooked factors, such as low mileage or added features. I've seen folks add 15-20% with some backbone.

What's involved in buying back a totaled EV? Buying back means purchasing from the salvage auction after it's totaled, potentially for $8,000 on a Model Y, then handling repairs yourself. You get the battery salvage value, around $4,000, but it's risky if the damage is extensive. Only do it if you're handy or have a good mechanic.

Is gap insurance worth it for EVs in 2026? Yes, it's critical because EVs depreciate fast, leaving you with big shortfalls like $15,000 on a totaled Tesla. For just $200-500 annually, it bridges that gap, making it a no-brainer. Skip it, and you're setting yourself up for regret.

How does battery salvage value affect what happens when your EV is totaled? Battery salvage can add $3,000-$6,000 to your EV's worth, which insurers might factor into the payout for something like a Rivian. It means more money in your pocket if you negotiate, but they often downplay it. Always ask for a breakdown to maximize your return.

Alright, we've covered the gritty details of what happens when your EV is totaled, from the inspection headaches to fighting for every dollar. And yeah, I know, another insurance deep-dive, but this one's got your back. That's my two cents. Take it or leave it — but I hope it helps. — Alex