Buying insurance for an electric vehicle (EV) can be like trying to assemble a piece of IKEA furniture without the instructions - it's a frustrating experience that leaves you wondering what you're doing wrong. But what if I told you that the real challenge isn't the assembly itself, but rather understanding the secret language that insurance companies speak? Sound familiar?

WARNING: Don't Get Caught Off Guard By These Hidden Costs

When it comes to insuring your brand-new Tesla Model 3, you might be surprised to learn that the cost of EV insurance can be significantly higher than traditional gas-powered vehicles. We're talking upwards of $2,500 per year, compared to around $1,800 for a similar gas-powered car. That one stung. But why is EV insurance so expensive, anyway? Well, actually, it's not just the cost of the vehicle itself, but also the cost of replacement parts, labor, and the fact that EVs are still a relatively new technology. For instance, the BMW iX's advanced battery system can cost upwards of $10,000 to replace, which is a significant factor in determining insurance premiums. Know what the kicker is? Insurance companies often use complex algorithms to determine your premium, taking into account factors like your driving history, location, and even your credit score. Wild, right?

But here's the thing: understanding these algorithms and the terminology used by insurance companies can help you make informed decisions and potentially save you money in the long run. Take, for example, the concept of "actuarial tables" - these are statistical models used to predict the likelihood of certain events, like accidents or theft. By understanding how these tables work, you can better navigate the insurance landscape and avoid costly surprises. And, let's be real, who doesn't love saving money?

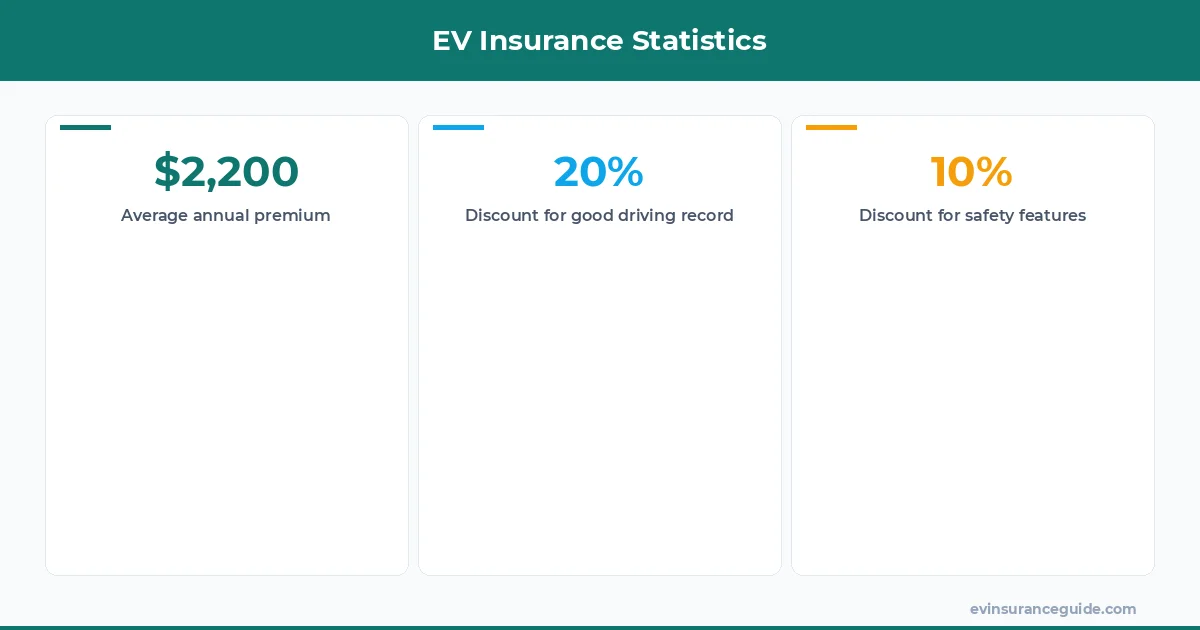

Pro tip: When shopping for EV insurance, be sure to ask about discounts for safety features like adaptive cruise control or lane departure warning systems. Some insurance companies, like Geico, offer discounts of up to 10% for vehicles equipped with these features.

STORY_TEASE: My Friend's Rivian R1T Insurance Nightmare

I've got a friend who recently purchased a brand-new Rivian R1T, and let me tell you, the insurance quotes he received were nothing short of astonishing. We're talking upwards of $3,500 per year, which is basically the cost of a brand-new laptop. But what really took the cake was when one insurance company told him that they wouldn't cover his vehicle at all, citing the fact that it was an "experimental" vehicle. Experimental? The Rivian R1T is a production vehicle, available for purchase at dealerships across the country. It's not like my friend was trying to insure a homemade electric vehicle or something. But, I guess that's just the kind of thing that can happen when you're dealing with insurance companies.

So, what can you do to avoid a similar situation? For starters, it's essential to do your research and shop around for insurance quotes from multiple companies. Don't be afraid to ask questions, either - what's the average cost of EV insurance? Why is EV insurance so expensive, anyway? And, what kind of discounts are available for EV owners? By understanding the answers to these questions, you can make informed decisions and avoid costly surprises.

And, let's not forget about the Hyundai Ioniq 5 - a fantastic EV that's often overlooked in favor of more popular models like the Tesla Model Y. But, the Ioniq 5 has its own set of unique features, like its advanced battery system and sleek design. And, when it comes to insurance, the Ioniq 5 can be a bit of a mixed bag - some insurance companies offer competitive rates, while others charge an arm and a leg. But, that's a story for another time...

QUESTION: What Exactly Is A 'Loss Payee' And Why Should I Care?

So, you're browsing through your insurance policy, and you come across the term "loss payee." What does it mean, exactly? Well, a loss payee is essentially the party that's entitled to receive payment in the event of a loss or damage to your vehicle. In most cases, this will be you, the vehicle owner. But, in some cases, it could be a lender or leasing company, especially if you're financing your vehicle. Know what the implications are? If you're not careful, you could end up with a situation where the loss payee is someone other than you, which could lead to all sorts of problems down the line.

For instance, let's say you're financing your Tesla Model 3 through a bank, and the bank is listed as the loss payee on your insurance policy. If your vehicle is involved in an accident, the insurance company will pay the bank directly, rather than you. This can be a problem if you need the money to repair or replace your vehicle, but the bank is holding onto it. But, if you understand what a loss payee is and how it works, you can avoid these kinds of situations and ensure that you're protected in the event of a loss.

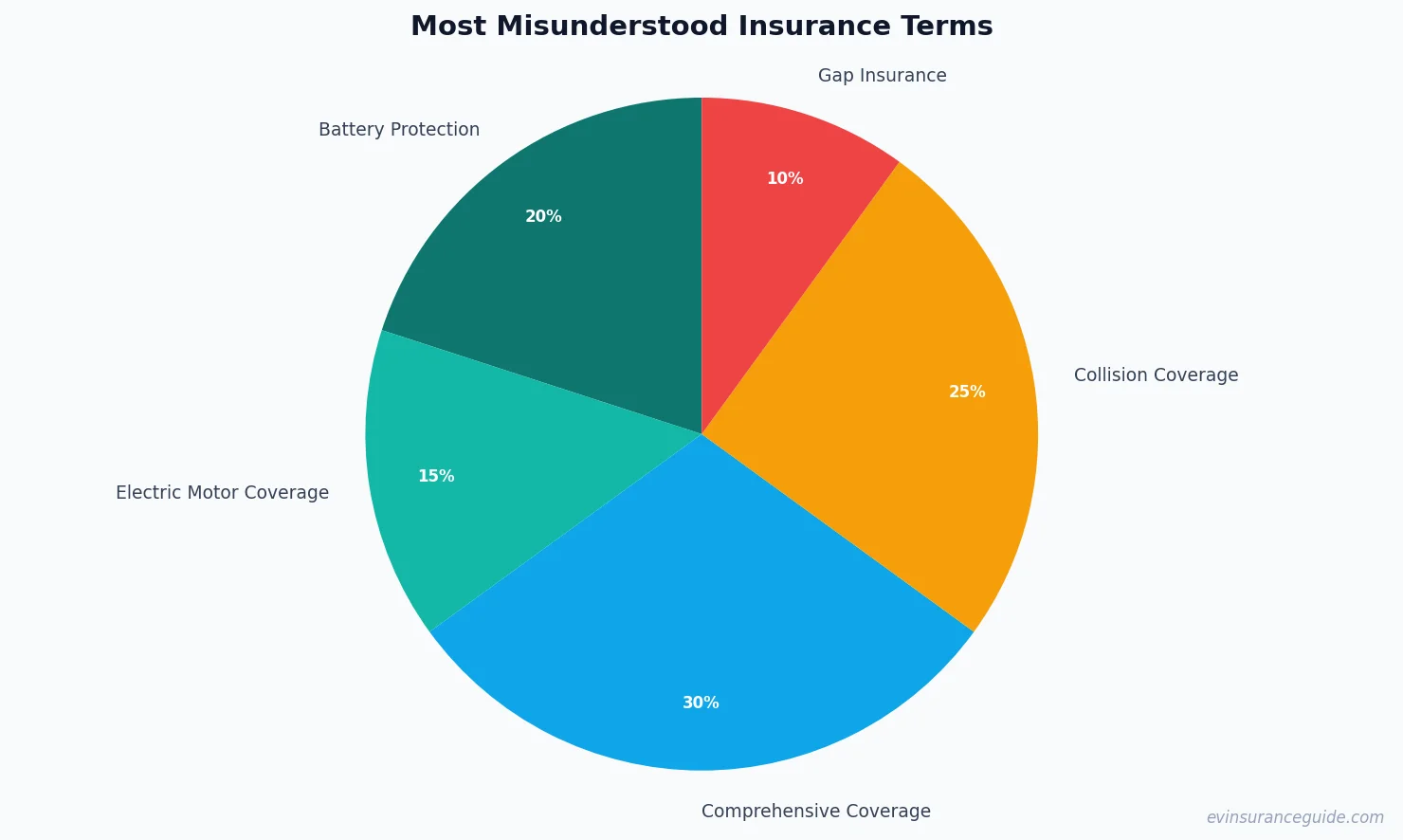

And, speaking of protection, have you ever heard of "gap insurance"? It's a type of insurance that covers the difference between the actual cash value of your vehicle and the amount you still owe on your loan or lease. It's a pretty common practice in the automotive industry, but it's especially important for EV owners, who may be more likely to experience a total loss due to the high cost of replacement parts.

HONEST_OPINION: The Truth About EV Insurance - It's Not All Bad News

Look, I'm not gonna sugarcoat it - EV insurance can be expensive. But, it's not all bad news. There are some insurance companies out there that are actually working to make EV insurance more affordable and accessible to the masses. Take, for example, the insurance company, USAA, which offers competitive rates for EV owners, as well as discounts for safety features like adaptive cruise control. Or, consider the company, Liberty Mutual, which offers a "green vehicle discount" for owners of hybrid or electric vehicles.

So, what's the takeaway? Don't be afraid to shop around and compare rates from different insurance companies. And, don't be discouraged if you don't find the perfect policy right away. With a little patience and persistence, you can find an insurance policy that meets your needs and fits your budget. And, remember, it's not just about the cost - it's about the level of protection and service you receive.

And, let's not forget about the environmental benefits of EVs - they produce zero tailpipe emissions, which can help reduce air pollution and mitigate the impacts of climate change. So, even if EV insurance is a bit more expensive, it's worth it in the long run.

COMPARISON: EV Insurance Vs. Traditional Insurance - What's The Difference?

So, how does EV insurance compare to traditional insurance? Well, for starters, EV insurance tends to be more expensive, due to the higher cost of replacement parts and the fact that EVs are still a relatively new technology. But, there are some key differences in terms of coverage and benefits, as well. For example, some insurance companies offer specialized coverage for EVs, like "battery protection" or "electric motor coverage."

And, let's not forget about the Rivian R1T's advanced battery system - it's a game-changer in the world of EVs. But, it's also a significant factor in determining insurance premiums. So, if you're considering purchasing a Rivian R1T or any other EV, be sure to factor in the cost of insurance when making your decision.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance can vary widely depending on a number of factors, including the type of vehicle, driving history, and location. However, according to recent estimates, the average cost of EV insurance is around $2,200 per year, which is significantly higher than traditional insurance.

#### Why is EV insurance so expensive?

EV insurance is expensive due to a number of factors, including the high cost of replacement parts, the fact that EVs are still a relatively new technology, and the lack of data on EV crash rates and repair costs.

#### What are some common mistakes to avoid when shopping for EV insurance?

Some common mistakes to avoid when shopping for EV insurance include not comparing rates from multiple companies, not reading the fine print, and not asking about discounts for safety features or other perks.

#### Can I get a discount on my EV insurance if I have a good driving record?

Yes, many insurance companies offer discounts for drivers with good driving records, including those who own EVs. In fact, some companies offer discounts of up to 20% for drivers with spotless records.

#### What is the difference between comprehensive and collision coverage?

Comprehensive coverage covers damage to your vehicle that's not related to an accident, such as theft, vandalism, or natural disasters. Collision coverage, on the other hand, covers damage to your vehicle that's related to an accident, regardless of who's at fault.

#### Are there any specialized insurance companies that cater to EV owners?

Yes, there are several insurance companies that specialize in EV insurance, including companies like USAA and Liberty Mutual. These companies often offer competitive rates and specialized coverage options for EV owners.

That's my two cents. Take it or leave it — but I hope it helps. — Alex