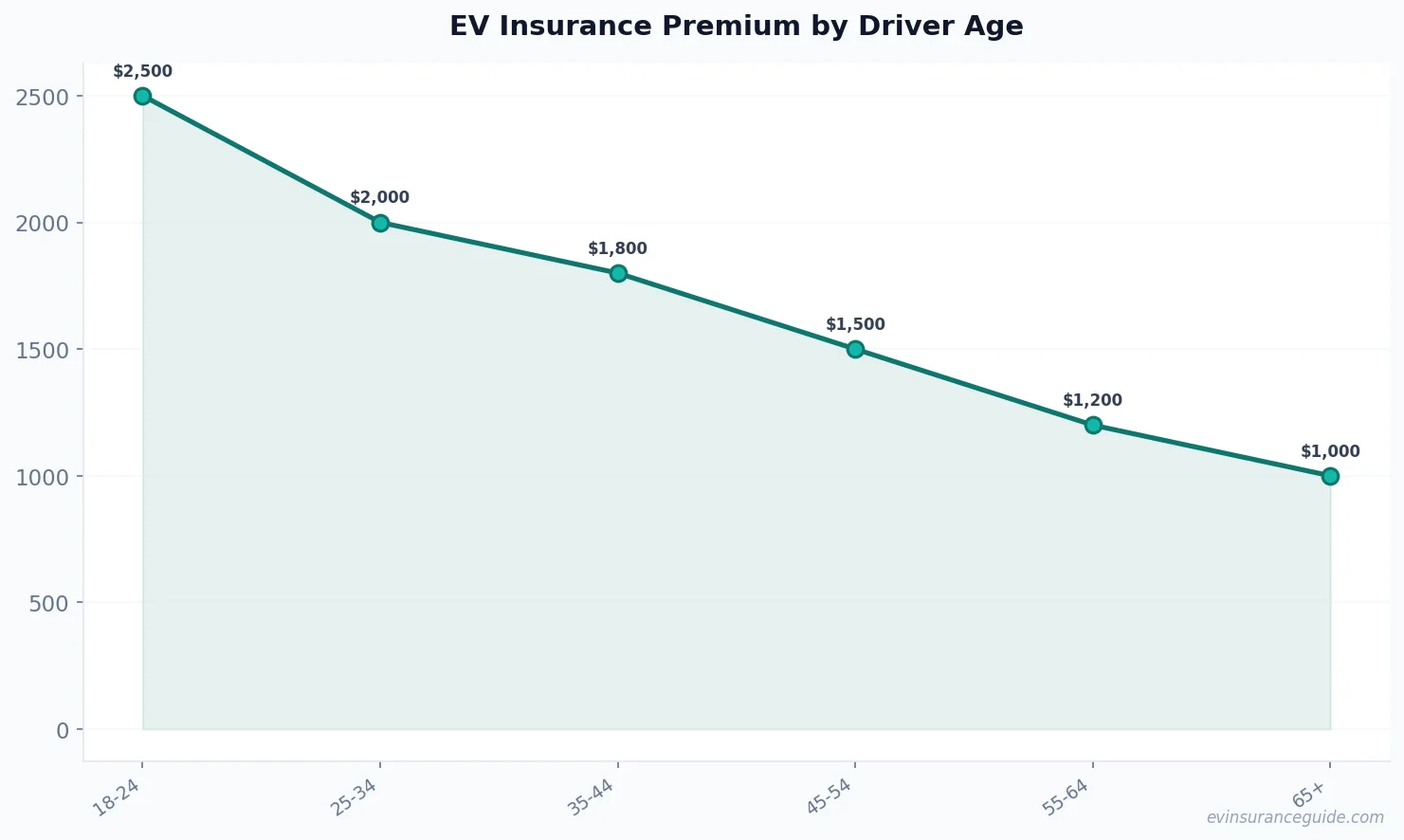

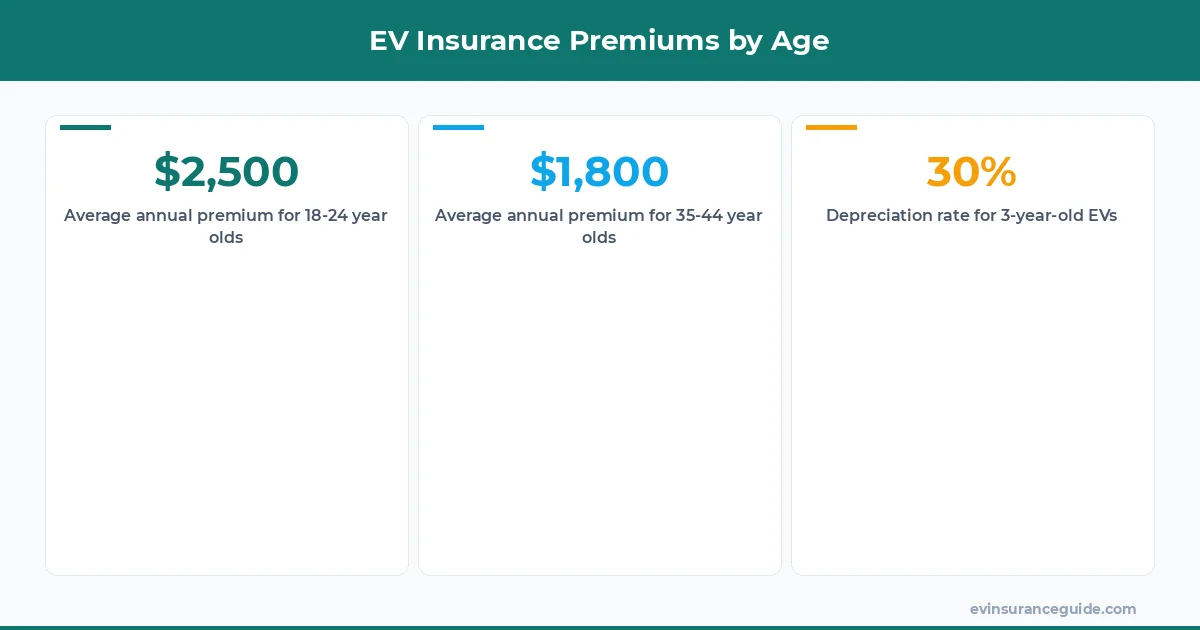

Meet Emily, a 28-year-old EV enthusiast who recently switched from a gas-guzzler to a brand-new Tesla Model 3. Before the switch, her insurance premium was around $1,200 per year. But after getting her new Tesla, her premium skyrocketed to $2,500. She was shocked, to say the least. That was until she discovered that her age was a significant factor in her insurance premium. Fast forward a few months, Emily decided to shop around and found a better deal with Geico, which offered her a premium of $1,800 per year. She saved $700, and that's a big deal.

MYTH_BUST — You're Never Too Old for Affordable EV Insurance

The common myth is that older drivers always pay more for insurance. But that's not entirely true. While it's true that younger drivers tend to pay more, there are some exceptions. For instance, a 55-year-old driver with a clean record and a Rivian R1T can expect to pay around $1,500 per year in insurance premiums. That's not bad, considering the average annual premium for a Rivian is around $2,000. Know what the kicker is? Some insurance companies, like State Farm, offer discounts for older drivers who have completed a defensive driving course. That can save you around $200 per year.

But here's the thing: EV depreciation and insurance are closely linked. As your EV depreciates, your insurance premium may decrease. For example, a 3-year-old Hyundai Ioniq 5 may depreciate by around 30%, which can result in a lower insurance premium. That's a good thing, right? Well, actually, it's a bit more complicated than that. You see, while depreciation can lower your insurance premium, it can also affect the overall value of your vehicle. And that's where ev depreciation and insurance come into play.

QUESTION — How Does Age Affect EV Insurance Premiums, Really?

So, how does age really affect EV insurance premiums? It's a bit of a mixed bag, to be honest. On one hand, younger drivers tend to pay more for insurance, regardless of the type of vehicle they drive. For instance, a 22-year-old driver with a BMW iX can expect to pay around $2,500 per year in insurance premiums. That's a pretty penny, if you ask me. On the other hand, older drivers with a clean record and a reliable EV can expect to pay less. But what about drivers in their 40s and 50s? Do they get a break? Well, kinda. Some insurance companies, like Allstate, offer discounts for drivers in this age group who have a good driving record.

Sound familiar? You're not alone. Many drivers are unaware of the impact of age on their insurance premiums. But here's the thing: ev depreciation and insurance are not just about age. It's also about the type of vehicle you drive, your driving record, and even your location. For example, a driver in California may pay more for insurance than a driver in Texas, simply because of the higher cost of living in California. That one stung, didn't it?

HONEST_OPINION — EV Insurance Premiums Are a Rip-Off for Younger Drivers

Let's be real, folks. EV insurance premiums are a rip-off for younger drivers. I mean, come on, $2,500 per year? That's just not fair. Especially when you consider that many younger drivers are more likely to drive safely and follow the rules of the road. Dead serious. But what can you do, right? Well, actually, there are a few things you can do. For one, you can shop around for insurance quotes. Don't just stick with the first company you find. Compare rates, and look for discounts. You can also consider driving an older EV, which may be cheaper to insure. And, of course, maintaining a clean driving record is key.

Pro tip: Consider driving a vehicle with a lower insurance group rating, such as a Tesla Model Y. This can save you around $500 per year in insurance premiums.

But what about the impact of ev depreciation and insurance on older drivers? Well, it's a bit of a different story. Older drivers may not have to worry as much about depreciation, since their vehicles are already a few years old. But they still need to consider the overall cost of ownership, including insurance premiums. And that's where ev depreciation and insurance come into play. For example, a 60-year-old driver with a 5-year-old Rivian R1T may be able to save around $300 per year in insurance premiums, simply because the vehicle has depreciated.

WARNING — Don't Fall for the 'Low-Down-Payment' Trap

Be careful, folks. Some insurance companies may offer you a low down payment, but then hike up your monthly premiums. That's not a good deal, trust me. You'll end up paying more in the long run. For example, a company like Progressive may offer you a low down payment of $100, but then charge you $250 per month in premiums. That's a total of $3,000 per year. Nope. You're better off paying a higher down payment and getting a lower monthly premium.

COMPARISON — EV Insurance vs. Gas-Powered Vehicle Insurance

So, how does EV insurance compare to gas-powered vehicle insurance? Well, it's a mixed bag, to be honest. On one hand, EVs tend to be more expensive to insure, simply because they're more expensive to repair. For example, a Tesla Model S may cost around $3,000 to repair, whereas a gas-powered sedan may cost around $1,500. That's a big difference. On the other hand, EVs may be cheaper to maintain, since they have fewer moving parts. And that can save you money in the long run.

FAQs

#### What is the average annual premium for an EV?

The average annual premium for an EV can range from $1,500 to $3,000, depending on the type of vehicle, driver age, and location. For example, a 30-year-old driver with a Tesla Model 3 may pay around $2,000 per year in insurance premiums.

#### How does age affect EV insurance premiums?

Age can significantly affect EV insurance premiums. Younger drivers tend to pay more, while older drivers with a clean record may pay less. For instance, a 25-year-old driver with a BMW iX may pay around $2,500 per year in insurance premiums, while a 50-year-old driver with a clean record may pay around $1,800 per year.

#### What is the impact of ev depreciation and insurance on overall vehicle cost?

Ev depreciation and insurance can significantly impact the overall cost of vehicle ownership. For example, a 3-year-old Hyundai Ioniq 5 may depreciate by around 30%, which can result in a lower insurance premium. But that also means the vehicle is worth less, which can affect the overall cost of ownership.

#### Can I save money on EV insurance by driving an older vehicle?

Yes, driving an older EV can save you money on insurance premiums. For example, a 5-year-old Rivian R1T may be cheaper to insure than a brand-new model. And that can save you around $300 per year in insurance premiums.

#### How can I shop for EV insurance quotes?

You can shop for EV insurance quotes by comparing rates from different companies, such as Geico, State Farm, and Allstate. You can also consider working with an insurance broker who specializes in EV insurance.

#### What are some common discounts for EV insurance?

Some common discounts for EV insurance include discounts for older drivers, clean driving records, and low mileage. You can also consider installing safety features, such as anti-theft devices, to save money on insurance premiums.

#### Are there any specific EV models that are cheaper to insure?

Yes, some EV models are cheaper to insure than others. For example, the Tesla Model Y may be cheaper to insure than the Tesla Model S, simply because it's a more affordable vehicle. And that can save you around $500 per year in insurance premiums.

#### How does location affect EV insurance premiums?

Location can significantly affect EV insurance premiums. For example, a driver in California may pay more for insurance than a driver in Texas, simply because of the higher cost of living in California. That one stung, didn't it?

#### What is the best way to save money on EV insurance?

The best way to save money on EV insurance is to shop around for quotes, consider driving an older vehicle, and maintain a clean driving record. You can also consider working with an insurance broker who specializes in EV insurance.

#### Are there any government incentives for EV insurance?

Yes, some governments offer incentives for EV owners, such as tax credits or rebates. For example, the US government offers a tax credit of up to $7,500 for EV owners. And that can save you money on your overall vehicle cost.

#### Can I bundle my EV insurance with other insurance policies?

Yes, you can bundle your EV insurance with other insurance policies, such as home or life insurance. This can save you money on your overall insurance premiums. And that's a good thing, right?

#### How often should I review my EV insurance policy?

You should review your EV insurance policy at least once a year to ensure you're getting the best rates and coverage. You can also consider working with an insurance broker who can help you review your policy and find better deals.

#### What is the average cost of EV insurance for a 30-year-old driver?

The average cost of EV insurance for a 30-year-old driver can range from $1,500 to $2,500 per year, depending on the type of vehicle, location, and driving record. For example, a 30-year-old driver with a Tesla Model 3 may pay around $2,000 per year in insurance premiums.

Drive safe out there.