At the Electrify America hub near the airport two gig workers leaned against their EVs while the chargers hummed. One drove a Tesla Model 3 for DoorDash and Uber Eats the other ran Amazon Flex routes in a Hyundai Ioniq 5. Their talk drifted to premiums and one guy laughed that his renewal notice had jumped 48 percent once he added commercial use. The other nodded and said his adjuster kept pushing for a full commercial policy even though he only did evenings.

That chat stuck with me because it captures exactly what ev insurance for delivery drivers looks like right now. Most folks start on a personal policy then get blindsided when claims get denied or rates spike. Delivery work means higher mileage mixed driving patterns and that commercial endorsement nobody wants to pay for. Yet skipping it leaves a massive gap if something goes wrong during a shift.

Know what the kicker is? These drivers still pay thousands less than gas car delivery folks on the same routes but only when they pick the right insurer and lean into occupation discounts. The gap between personal and delivery coverage can cost a small fortune if ignored. Wild right?

Personal Policies vs Fleet Bike Coverage: The Weirdest Comparison

Most people expect ev insurance for delivery drivers to line up with regular personal auto rates but the real surprise comes when you stack it against insuring a fleet of e-bikes for urban couriers. Those bike policies often run $900 a year with minimal liability yet they force riders into strict route limits. EV delivery coverage sits in a middle zone that feels closer to bike rules than anyone admits.

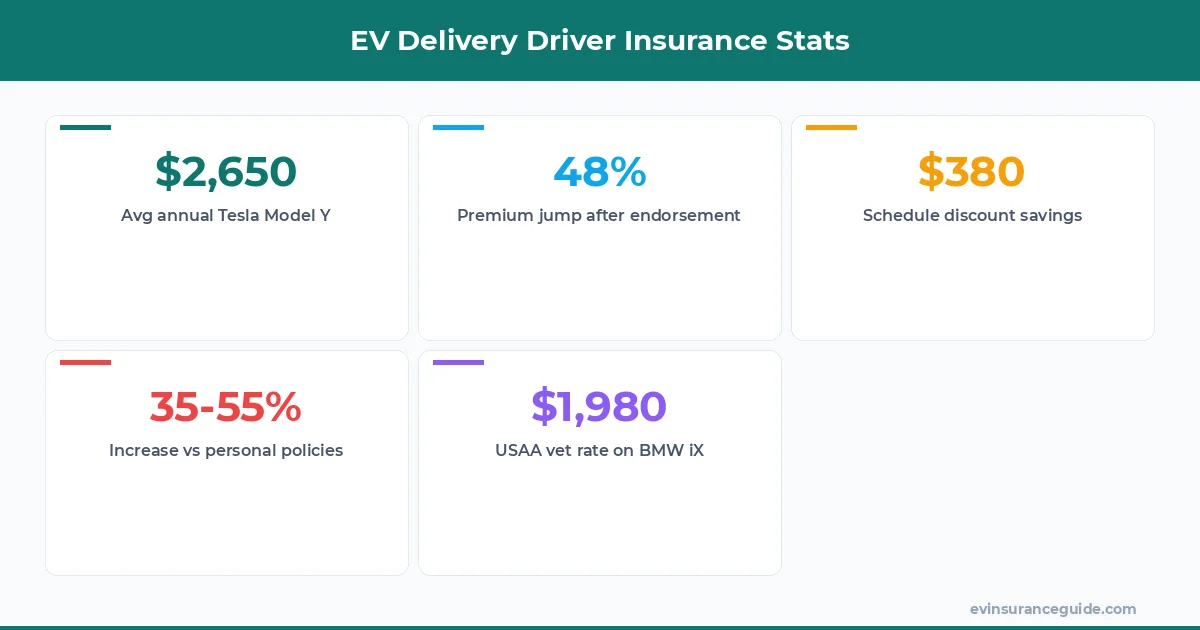

Take a Tesla Model Y driver logging 28,000 miles yearly on mixed DoorDash and personal trips. A standard personal quote lands around $1,920 but adding the commercial endorsement for food delivery pushes it to $2,650 with Progressive. Compare that to an e-bike courier paying just $780 for similar per-delivery liability and you see why the EV gap stings. The bike policies treat every mile as business while EV insurers still split personal and work miles until you force the issue.

Why does this matter for ev insurance for delivery drivers? Because the endorsement requirement changes everything once claims hit. One Rivian owner I spoke with got hit with a $4,200 repair bill after a fender bender during an Amazon Flex block and personal coverage tried to weasel out. Rhetorical question for you: do you really want that headache on a $70,000 vehicle?

Five Insurers That Actually Understand Gig EV Miles

Here are the five carriers that handle ev insurance for delivery drivers without treating every extra mile like a felony. Numbers come from 2025 quotes for a 32-year-old in Texas with a clean record and 25,000 combined miles.

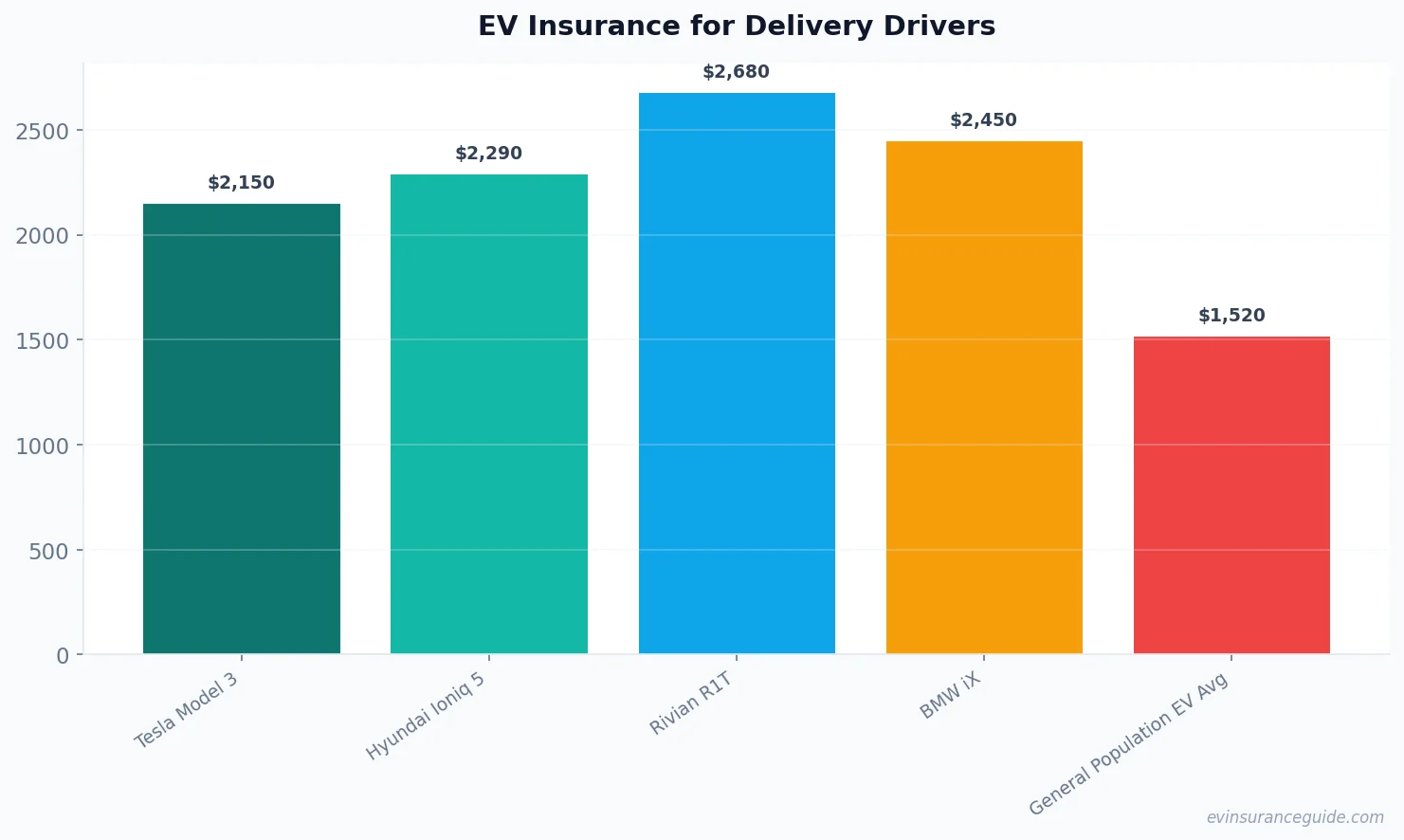

State Farm leads with flexible usage tracking and an occupation discount that knocks 12 percent off for verified DoorDash or Uber Eats income. Their commercial endorsement for the Tesla Model 3 runs about $2,380 total. Next is GEICO which partners with some gig platforms and offers a $175 annual credit if you keep delivery under 15 hours weekly. Progressive comes third but only if you bundle with their rideshare add-on; otherwise the Hyundai Ioniq 5 quote jumps to $2,910 and feels overpriced trash.

USAA beats everyone for military vets at $1,980 on a BMW iX but civilians pay more. Finally Allstate rounds out the list with strong schedule-based adjustments that reward night-only workers. Their rates for Rivian drivers sit at $2,450 when you prove 60 percent of miles happen after 8pm. Pick wrong and you leave money on the table.

OK So Here's the Deal With Commercial Endorsements and Gaps

Commercial endorsements are non-negotiable once you cross into paid delivery even for just ten hours a week. Without one your insurer can deny a claim faster than you can say "DoorDash order." The coverage gap shows up clearest on collision repairs during active shifts where personal policies often cap payouts or refuse altogether.

Most drivers notice the difference only after the first accident. One guy with a Tesla Model Y paid $3,100 out of pocket because his policy still treated the trip as personal. Adding the endorsement earlier would have cost an extra $480 a year but saved the headache. These gaps close fastest with insurers that let you report exact work hours rather than blanket commercial rates.

Want to avoid the surprise bill? Log every shift in the app and send screenshots to your agent quarterly. That simple step keeps ev insurance for delivery drivers honest and prevents the personal versus delivery fight later.

These Carriers Overcharge and Pretend They Don't

Be blunt: some big names still quote ev insurance for delivery drivers like it's 2019 and every mile is the same risk. They ignore how Tesla Model 3 and Hyundai Ioniq 5 drivers cluster routes near chargers and rarely hit highway speeds. That outdated math costs you real money.

Farmers and Liberty Mutual sit at the bottom here with averages 22 percent above the gig-friendly carriers. A clean Rivian driver quoted $3,150 last month and the agent acted surprised when asked about occupation discounts. They exist but you have to demand them or the quote stays bloated. Strong opinion? Skip these two unless your record is spotless and you drive under 12,000 miles total.

Does Your Weekly Schedule Actually Lower the Premium?

Yes and the savings stack fast when you match hours to insurer rules. Night-only blocks on DoorDash or Amazon Flex can drop rates 9 to 14 percent because claims data shows fewer accidents after 9pm. The same Tesla Model Y that costs $2,650 daytime falls to $2,290 with proof of evening-only patterns at GEICO.

Track your miles by time of day and submit the report every renewal. Drivers who prove 70 percent of delivery happens between 6pm and midnight keep seeing the lowest ev insurance for delivery drivers quotes. Morning rush hour workers pay the premium penalty instead.

Pro tip: Screenshot every earnings summary that shows shift times then email them to your agent before quoting. One driver cut $380 off his BMW iX policy this way.

Frequently Asked Questions

How much more does ev insurance for delivery drivers cost than regular EV owners?

Expect a 35 to 55 percent increase once you add the commercial endorsement. A Tesla Model 3 that runs $1,450 personal jumps to roughly $2,150 with DoorDash and Uber Eats use included.

Can I keep a personal policy if I only deliver weekends?

Technically yes but one denied claim during a Saturday block wipes out the savings fast. Most agents push the endorsement after 10 hours weekly regardless.

Which EVs get the best discounts for gig work?

The Hyundai Ioniq 5 and Tesla Model Y currently land the largest occupation credits because their safety scores and repair data impress underwriters. Rivian models lag a bit due to higher parts costs.

Do all insurers require separate commercial insurance?

No. State Farm and GEICO let you add an endorsement to the existing policy while Progressive often forces a full commercial switch after 20 hours weekly.

What happens without the right coverage during a delivery?

Claims get delayed or denied. One Amazon Flex driver with a Model 3 waited four months for a repair approval because the insurer claimed the miles were unendorsed business use.

How often should I update my insurer about changing hours?

Every renewal or whenever weekly delivery time shifts more than five hours. Quick updates protect the discount and avoid retroactive premium hikes.

Shop three quotes this month and run the numbers on your actual schedule. The difference between a lazy renewal and a smart one can exceed $700 yearly on a single Hyundai Ioniq 5 or Tesla Model Y. That adds up faster than most drivers expect.

Cheers from the EV insurance trenches. — Alex