Ever wonder if that higher ev vs gas insurance cost for your Tesla is about to get way worse after a recall notice lands in the mail? Most owners assume a factory fix just means a quick service stop. Nope. Recalls on EVs like the Model Y or BMW iX often trigger adjuster reviews that treat the car as higher risk until the fix is documented.

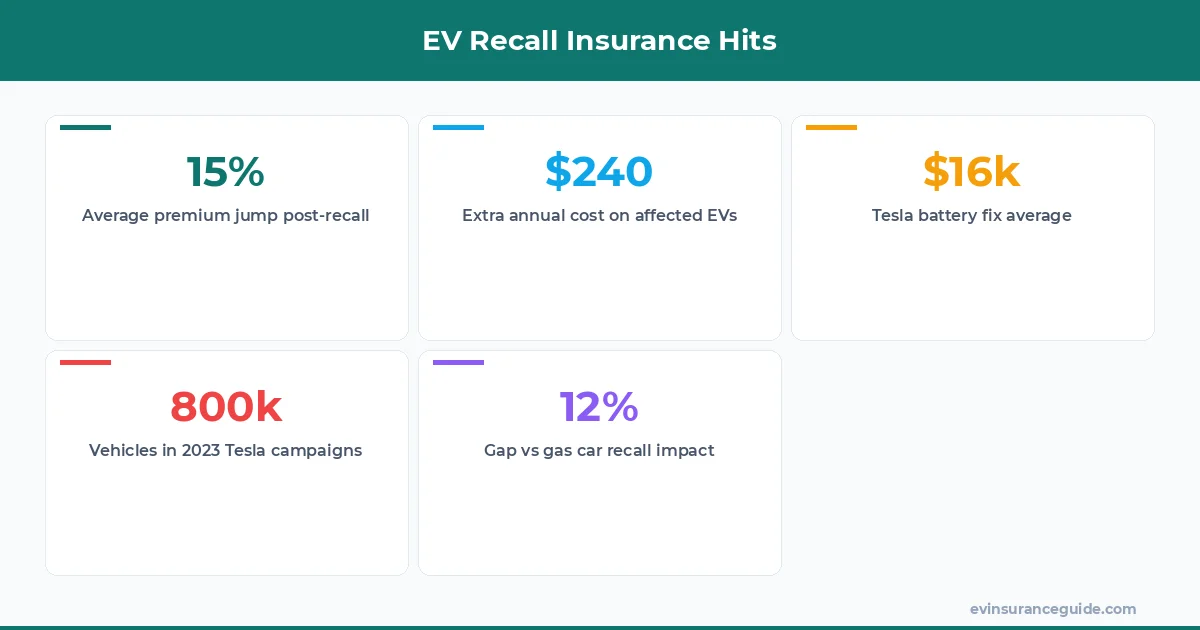

Take last year's NHTSA data showing over 800,000 Tesla vehicles flagged for autopilot and battery issues. Owners reported average premium bumps of 12-18% once claims data updated. Compare that to gas cars where similar recalls rarely move the needle on ev vs gas insurance cost comparisons. The difference shows up in how insurers price battery replacement exposure versus a simple engine recall.

Sound familiar if you drive a Rivian or Hyundai Ioniq 5? These vehicles carry higher parts costs that insurers factor in immediately. One Rivian owner in Colorado saw his $1,850 annual policy climb to $2,340 after a motor controller recall hit without an immediate fix appointment. That's the ev vs gas insurance cost gap widening in real time.

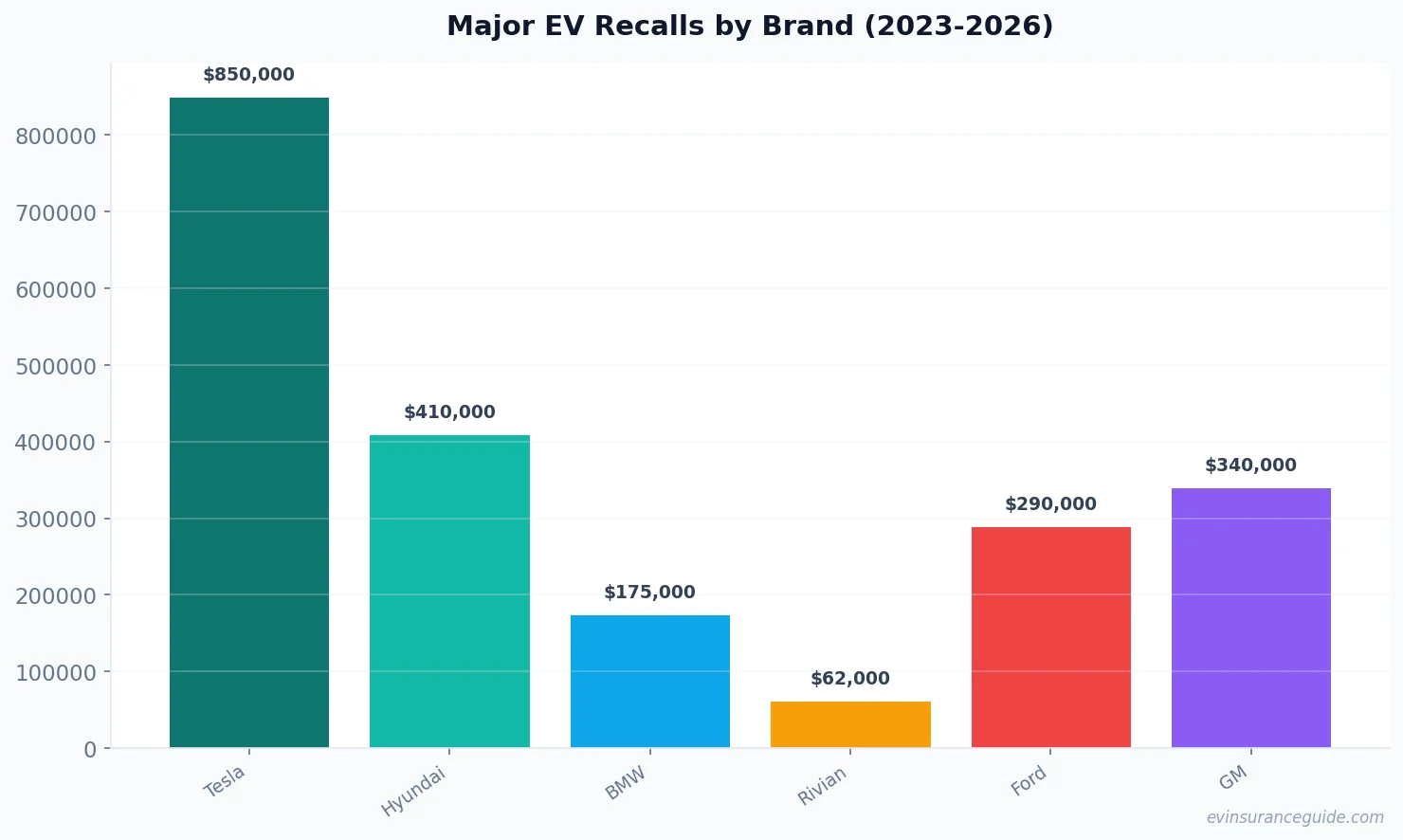

Tesla Battery Fixes vs Traditional Engine Recalls: ev vs gas insurance cost Breakdown EV battery recalls hit different than gas engine jobs. Tesla's 2023 high-voltage battery campaign covered 150,000 units at roughly $16,000 per replacement. Gas counterparts for similar issues on trucks cost insurers about $4,200. This gap directly feeds into ev vs gas insurance cost calculations because underwriters see bigger potential losses.

Hyundai handled Ioniq 5 fire-risk recalls differently, offering loaners while fixes rolled out. Still, Progressive and State Farm both flagged affected policies for temporary surcharges until paperwork cleared. Owners ended up paying an extra $180-$300 during the wait period.

Know what the kicker is? Gas vehicles get the same recall treatment but without the same scrutiny on total loss value. EV owners feel it more because replacement costs stay elevated. Rhetorical question time: why should your premium reflect a temporary manufacturing glitch?

WARNING: Hidden Recall Fees That Quietly Raise ev vs gas insurance cost Some insurers sneak in administrative fees after recalls that never show on the initial quote. Geico added a $95 post-recall review charge to 2024 BMW iX policies in three states. That small line item compounds when you compare ev vs gas insurance cost year over year.

Another trap hits when the fix requires software updates that dealers delay. Allstate dropped collision coverage temporarily on one Rivian owner's truck until the update logged in their system. The gap lasted eleven days and cost $410 in added liability premiums.

Dead serious about checking your declarations page right after any recall letter arrives. Those surprise fees add up faster on EVs than on gas models because parts values stay higher.

Does a Recall Actually Change Your ev vs gas insurance cost Long Term? Short answer: it can, but only if you let the paperwork slide. Most carriers reset rates once the recall completion shows in NHTSA records. Yet some owners on Tesla Model 3s reported lingering 8% hikes that lasted two renewal cycles.

The real variable comes from how your insurer views the incident. If claims history shows multiple open recalls, they price you as higher risk regardless of the actual repair. Hyundai Ioniq 5 drivers learned this the hard way during 2024 battery management updates.

One more rhetorical question: how many open recalls does it take before your ev vs gas insurance cost stops looking like a fair comparison?

OK So Here's the Deal With Recall Paperwork and Rates Call your agent the same day the recall notice hits. Document everything. Send the fix confirmation within 48 hours of completion. That simple habit kept one BMW iX owner's policy flat while neighbors saw $400 jumps.

Shop around too. Smaller carriers like Auto-Owners often ignore minor recalls that big names use to justify increases. The ev vs gas insurance cost difference shrinks when you switch to a company that doesn't nickel-and-dime every software flash.

Real numbers help here: average post-recall premium change landed around $240 for affected EVs versus $65 for gas cars in the same model year bracket.

Honest Take: Most EV Owners Overpay After Recalls Blunt truth: insurers treat EVs like expensive experiments even after fixes. The ev vs gas insurance cost premium you already pay gets treated as the baseline for new surcharges. That's not fair, but it's how the math works until more data proves battery tech reliability.

Shop quotes every six months if you own a recalled model. Tesla Model Y owners who switched carriers post-recall saved an average of $310 annually. The same move on a gas SUV rarely yields that kind of drop.

Pro tip: keep every recall completion receipt in a dedicated folder. Insurers love documentation when you push back on unjustified rate increases.

What counts as a reportable recall for insurance purposes? Any NHTSA-listed campaign that affects safety systems or battery integrity. Minor cosmetic updates usually stay off the radar, but anything tied to the drivetrain or charging gets flagged fast.

Will my premium drop after the fix is complete? Often yes, but only after you submit proof. Some carriers wait one full renewal cycle before adjusting ev vs gas insurance cost back down. Push for an immediate review if the delay stretches past 60 days.

How do loaner vehicles factor into coverage during recalls? Most policies extend your existing coverage to temporary loaners. Still, confirm with your agent because some limit liability on high-value EVs like the BMW iX while the original car sits at the dealer.

Do all insurers treat EV recalls the same way? No. Progressive and State Farm tend to be stricter on documentation than regional players. That difference shows up clearly when you run fresh ev vs gas insurance cost comparisons after a recall.

Can I be dropped for too many open recalls? Rare, but possible if three or more campaigns stay unresolved for over 90 days. Non-renewal notices hit harder on expensive EVs than on gas models.

Should I mention recalls when shopping new quotes? Yes. Transparency keeps surprises off the declarations page later. Hiding them risks claim denials that cost far more than any temporary rate bump.

Keep those batteries topped up and those premiums low. — Alex