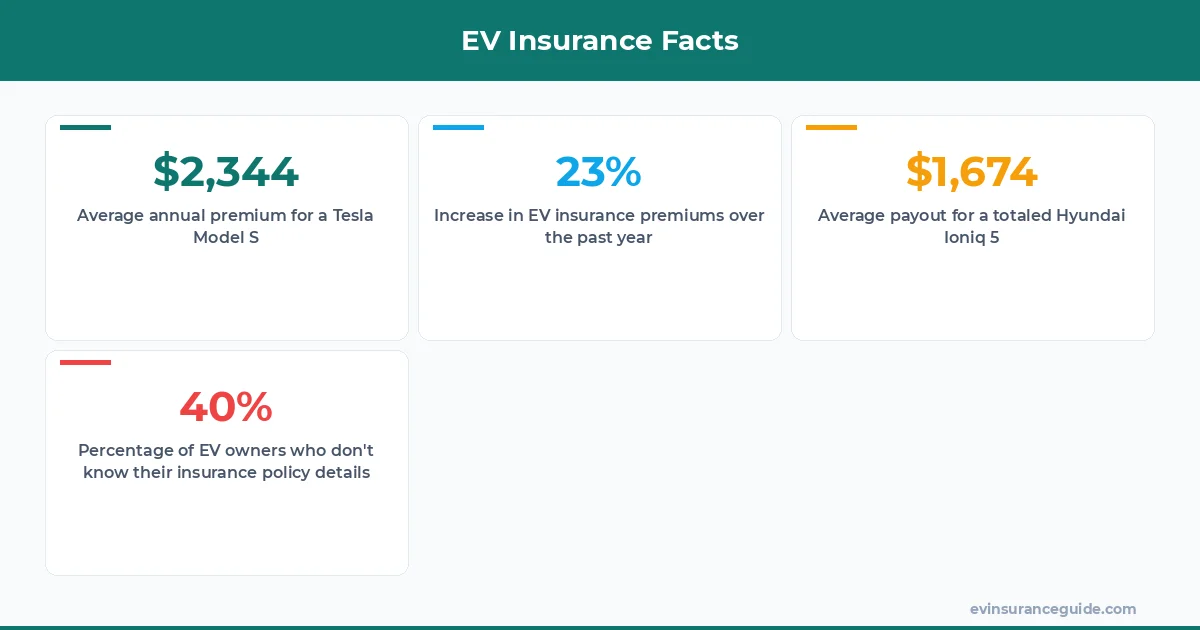

Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd just gotten a new job, moved to a different state, and upgraded to a fancier trim level. Sound familiar? I told him it's not just about the car – it's about the entire package. And that's where total loss comes in.

You see, when your EV is totaled, the insurance company doesn't just cut you a check for the sticker price. Nope. They've got a whole formula to figure out what they owe you. And it's not always pretty. Know what the kicker is? Some EVs are way more expensive to insure than others. Like, have you seen the premiums on a Tesla Model S? That's some crazy stuff.

The thing is, most people don't think about total loss until it's too late. They're too busy comparing monthly payments and wondering if they can afford the down payment. But trust me, it's worth considering. I mean, what if you're in an accident and your brand-new Rivian R1T is totaled? You wanna be prepared, right?

WARNING — Watch Out for Total Loss Traps

Total loss is a tricky business. The insurance company's goal is to pay out as little as possible, while you want to get paid as much as you can. It's a delicate dance. And if you're not careful, you might end up with a payout that's way lower than you expected. For example, let's say you own a BMW iX, which is one of the most expensive EVs to insure. If it's totaled, the insurance company might offer you $60,000, even though the market value is closer to $80,000. That one stung.

But here's the thing: you don't have to take their first offer. You can negotiate. And if you're smart, you'll do your research beforehand. I mean, have you checked the Kelley Blue Book value of your vehicle lately? You should. It's a good starting point for any negotiation.

Now, I know what you're thinking: what about all the extras I've added to my car? The fancy wheels, the premium sound system? Don't those count for something? Well, actually, they might. But it depends on the insurance company and the specific policy you have. Some companies will give you credit for those upgrades, while others won't. It's all about reading the fine print.

COMPARISON — Most Expensive EVs to Insure: A Side-by-Side Look

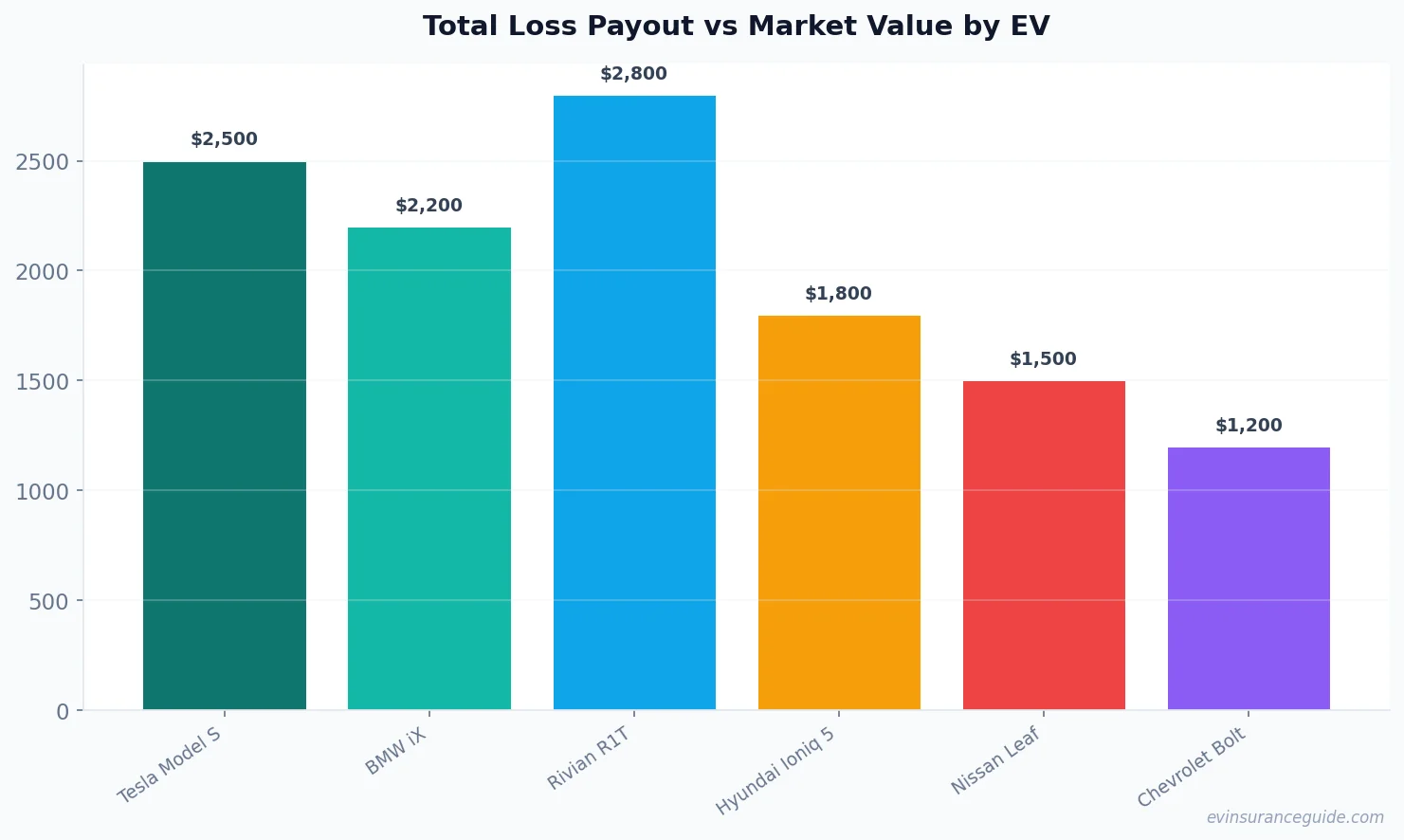

So, which EVs are the most expensive to insure? Well, let's take a look. The Tesla Model S, for example, can cost upwards of $2,500 per year to insure. The BMW iX? That'll be around $2,200. And the Rivian R1T? A whopping $2,800. But what about the Hyundai Ioniq 5? That's a more affordable option, with premiums ranging from $1,500 to $2,000 per year.

Now, you might be wondering why there's such a big difference. Is it just the price of the car? Nope. It's a combination of factors, including the car's safety features, its performance capabilities, and even its target market. For instance, the Tesla Model S is a luxury vehicle with a lot of power under the hood. That makes it more expensive to insure.

But here's the thing: you don't have to break the bank to own an EV. There are plenty of affordable options out there, like the Nissan Leaf or the Chevrolet Bolt. And if you're willing to do some research, you can find a policy that fits your budget. I mean, have you checked out the rates from companies like Geico or Progressive? They might surprise you.

STORY_TEASE — A Cautionary Tale of Total Loss

I've got a friend, let's call her Sarah, who owns a Tesla Model 3. She's a great driver, never had an accident in her life. But one day, she's driving home from work and some guy runs a red light. Next thing she knows, her car is totaled.

The insurance company offers her $40,000, which is way lower than the market value. She's devastated. But she doesn't give up. She negotiates with the adjuster, shows them the Kelly Blue Book value, and eventually gets them to increase the payout to $55,000. It's still not perfect, but it's better than nothing.

The point is, total loss can happen to anyone. And if you're not prepared, you might end up with a payout that's way lower than you expected. So, what can you do to protect yourself? Well, for starters, you can make sure you have the right insurance policy. One that covers total loss and provides a decent payout.

And don't just take the insurance company's word for it. Do your research, read the fine print, and know your rights. You might be surprised at what you can negotiate. As the saying goes, 'knowledge is power.'

7 Key Factors That Affect Total Loss Payouts

So, what exactly affects the total loss payout? Well, here are 7 key factors:

- 1. The market value of your vehicle

- 2. The age and condition of your vehicle

- 3. The insurance company's policy

- 4. The location where you live

- 5. Your driving record

- 6. The type of vehicle you own (some EVs are more expensive to insure than others)

- 7. The extras you've added to your vehicle (like fancy wheels or a premium sound system)

Now, you might be wondering how these factors interact with each other. Well, it's complicated. But basically, the insurance company takes all these factors into account and comes up with a payout that they think is fair.

But what if you don't agree with their assessment? What if you think the payout is too low? Well, that's where negotiation comes in. And if you're smart, you'll do your research beforehand. I mean, have you checked the National Automobile Dealers Association (NADA) guide values for your vehicle? You should. It's a good starting point for any negotiation.

Can You Really Get a Fair Total Loss Payout for Your EV?

So, can you really get a fair total loss payout for your EV? Well, it's possible. But it takes work. You've got to do your research, know your rights, and be willing to negotiate. And even then, there are no guarantees.

But here's the thing: it's worth trying. I mean, think about it. If you're in an accident and your brand-new Hyundai Ioniq 5 is totaled, you want to get paid as much as possible, right? You've invested a lot of money in that car, and you deserve to get a fair payout.

So, what can you do to increase your chances of getting a fair payout? Well, for starters, you can make sure you have the right insurance policy. One that covers total loss and provides a decent payout. And don't just take the insurance company's word for it. Read the fine print, know your rights, and be prepared to negotiate.

Pro tip: always keep detailed records of your vehicle's maintenance and upgrades. This can help you negotiate a higher payout if your car is ever totaled.

FAQs

#### What is total loss?

Total loss refers to a situation where your vehicle is damaged beyond repair, and the insurance company declares it a total loss.

#### How is total loss payout calculated?

The total loss payout is calculated based on the market value of your vehicle, minus any deductibles or fees.

#### Can I negotiate the total loss payout?

Yes, you can negotiate the total loss payout. It's always a good idea to do your research and know your rights before negotiating with the insurance company.

#### What are the most expensive EVs to insure?

The most expensive EVs to insure include the Tesla Model S, the BMW iX, and the Rivian R1T.

#### How can I save on EV insurance premiums?

You can save on EV insurance premiums by shopping around, comparing rates from different companies, and taking advantage of any discounts you may be eligible for.

#### What is the average cost of insuring an EV?

The average cost of insuring an EV can range from $1,500 to $3,000 per year, depending on the type of vehicle, your location, and other factors.

Keep those batteries topped up and those premiums low.

— Alex