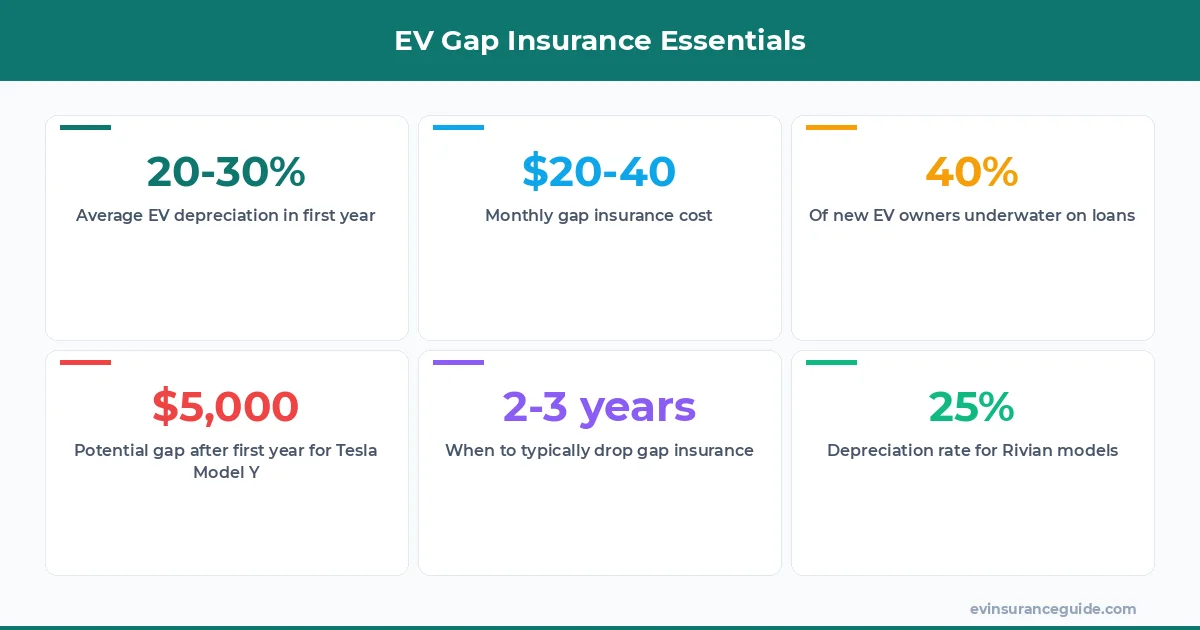

Man, I'm still fuming about how EV insurance companies play games with depreciation values. It's like they're betting on your shiny new Tesla Model 3 losing 25% of its worth the second you drive off the lot, and then they hit you with premiums that don't budge. We've got these groundbreaking electric vehicles promising the future, but insurers act like it's 1995, slapping on extra fees for things that aren't even issues anymore. Take gap insurance—it's this lifesaver for when your loan outpaces your car's value, yet some reps push it like it's optional candy. Nope, if you're upside down on a loan for a BMW iX or Hyundai Ioniq 5, skipping it could leave you thousands in the hole after an accident. And don't get me started on how dealers markup their gap policies by 50% just to line their pockets. That's just greedy, especially when EVs depreciate 20-30% in the first year alone. Sound familiar? It's frustrating because 'should I get gap insurance for my EV' is a question I hear every day, and the answer's often yes if you're financing big. Alright, enough venting—let's dig into why this matters for 2026 buyers.

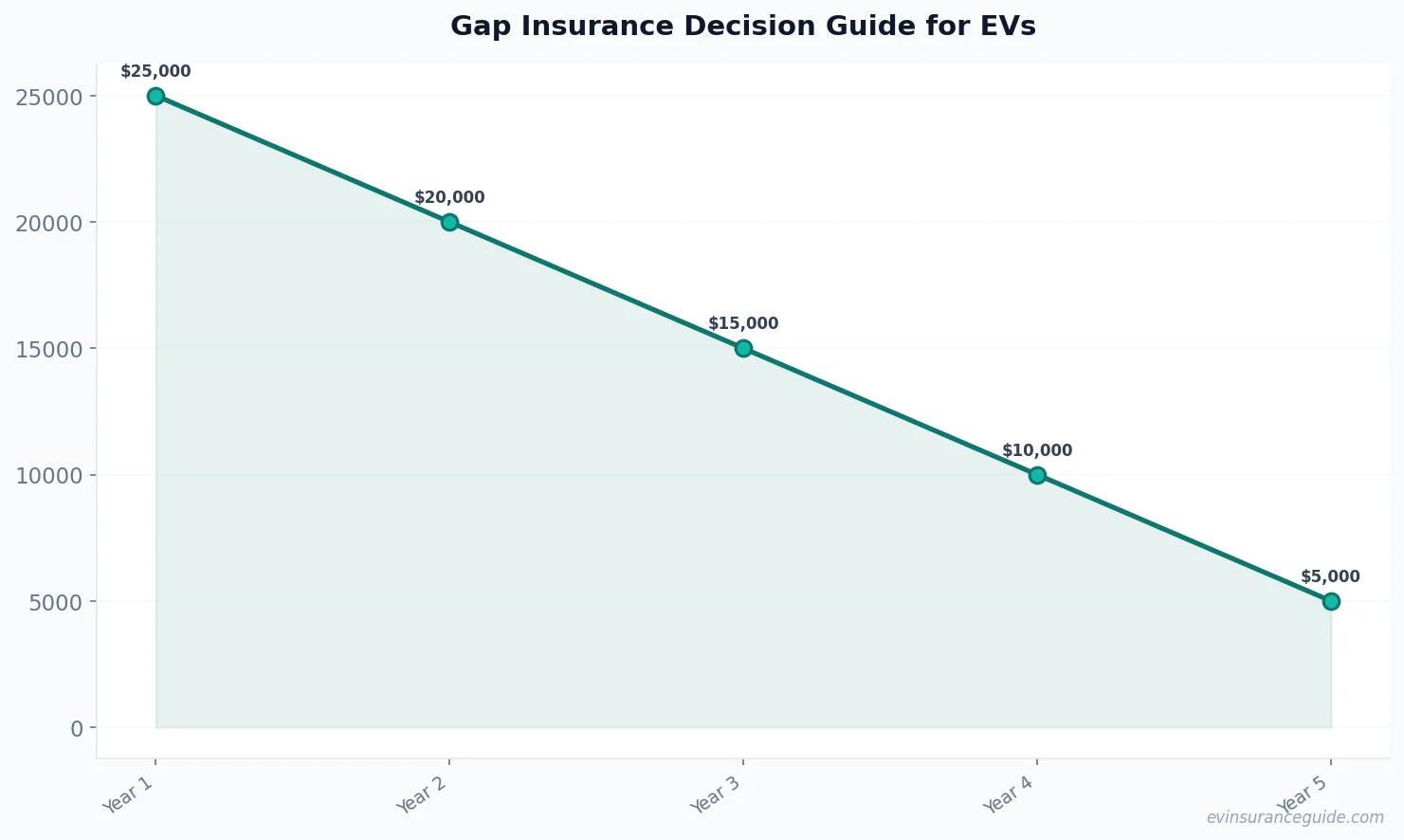

Should You Get Gap Insurance for Your EV If You Owe More Than It's Worth? Yeah, I know, another insurance deep dive, but this one's crucial. If your EV loan balance tops the actual value, gap insurance is basically a must—especially for models like the Rivian that drop value like a rock. We're talking about EVs depreciating 25% in year one, so if you financed a $50,000 Hyundai Ioniq 5 at 72 months, you might owe $40,000 while it's only worth $35,000 after 12 months. Know what the kicker is? Without gap, you're covering that $5,000 gap out of pocket if it's totaled. And I'm dead serious—'should I get gap insurance for my EV' screams yes if you're leasing or buying new with a loan. For instance, Progressive offers gap add-ons starting at $20/month, which could save you way more than that in a crash. But hold on, not every policy is equal; always compare Geico's rates, which might undercut by 10-15%.

Now, let's get specific. Take the Tesla Model Y—it's notorious for 30% depreciation in the first year, leaving owners upside down fast. If you're paying $600/month on a loan, gap could prevent you from eating that loss. Wild, right? I've seen folks regret skipping it after a fender-bender turned into a financial nightmare. On the flip side, if your down payment was hefty, say 20%, you might skate by without it. That's the reality—'should I get gap insurance for my EV' depends on your numbers, but I'd lean towards yes for most new buyers in 2026.

And here's a pro tip: Double-check your lender's requirements; some mandate gap if your loan-to-value ratio exceeds 80%. (OK, wait, scratch that—it's not always mandatory, but it sure feels like it.) Either way, for EVs like the BMW iX, getting gap through your insurer rather than the dealer saves fees—think $300 less per year.

OK So Here's the Deal With Gap Insurance Types and When to Get It Alright, let's cut the fluff—gap insurance isn't one-size-fits-all, and for EVs, timing is everything. You snag it when you're buying or leasing a new ride, like a Tesla Model 3, to cover that initial depreciation dive. Costs? We're looking at $20-40 a month from companies like State Farm, which beats paying thousands out of pocket. 'Should I get gap insurance for my EV'—yeah, absolutely, if your loan's over the car's value, which hits hard for models depreciating 28% in year one. I've crunched numbers on Rivian owners, and adding gap through a standalone provider like Assurant can be cheaper than dealer options by $150 annually.

But hold up, there are three main flavors: dealer gap, which is overpriced trash at a 40% markup; insurer gap, bundled with your policy for seamless claims; and standalone, perfect for flexibility. For a Hyundai Ioniq 5, insurer gap from Allstate might run $25/month versus $35 from the dealer. Know what stings? Dealers push their version hard, but it's often loaded with extras you don't need. And me? I'd go with insurer gap every time—less hassle, better rates.

Here's the thing—drop it once your loan dips below the car's value, usually after two to three years. For example, if your BMW iX is worth more than you owe by year three, you're golden. 'Should I get gap insurance for my EV' turns to no at that point, freeing up cash for upgrades. Hmm, let me rethink that—if you're in a high-risk area, keep it longer; depreciation varies by model.

The Harsh Truth: Gap Insurance Isn't Always Worth It, But Often It Is Look, I'm not sugarcoating this—gap insurance is a lifesaver for some, a waste for others, and for EVs, it's leaning towards essential in 2026. These cars tank in value so fast—think 22% for a Tesla Model Y—that if you're financing over $30,000, skipping gap is just dumb. Best deal I've seen? Insurer policies from Geico at $20/month, versus standalone ones that might nickel-and-dime you with fees. 'Should I get gap insurance for my EV'—yes, if you're like most folks with minimal down payments, because that 20-30% depreciation hit is no joke.

Take it from me, after arguing with adjusters over claims, the ones without gap always regret it. For a Rivian, which loses value at 25% annually, you're looking at potential losses of $7,500 in year one alone. But if you've got 30% down, pass on it—save that $500 a year for charging stations. And here's where I take sides: Dealer's gap is overpriced trash; go with your insurer for transparency.

One more thing—statistics show 40% of new EV owners are underwater on loans within a year, per J.D. Power data. That's why 'should I get gap insurance for my EV' is a big deal; it's not just protection, it's peace of mind. Wild, right? Don't let FOMO make you overpay, though—compare quotes religiously.

Busting the Myth: Gap Insurance Is Only for New Cars Here's the deal—people think gap insurance is just for brand-new EVs, but that's bunk. Even a two-year-old Hyundai Ioniq 5 with a loan could need it if depreciation's outpaced payments. I've heard the myth that it's pointless after the first year, yet data from Kelley Blue Book shows EVs like BMW iX still depreciate 15% annually. So, 'should I get gap insurance for my EV' isn't limited to day-one owners; it's about your specific loan situation.

Let me clarify: The real myth is that gap's a scam—it's not, especially when EVs drop 25% faster than gas cars. For Tesla Model 3 buyers, adding it mid-lease can save headaches. Know what the kicker is? Insurers like Progressive offer it for used EVs too, as long as you owe more than it's worth.

And yeah, some say it's redundant with comprehensive coverage, but that's false—comprehensive doesn't cover the loan gap. 'Should I get gap insurance for my EV'—bust that myth and check your equity first.

Warning: The Hidden Traps of Cheap Gap Insurance Watch out, because not all gap insurance is as straightforward as it seems—especially for EVs where depreciation tricks are everywhere. Some policies from sketchy providers exclude common claims, leaving you high and dry on a totaled Tesla Model Y. And don't even think about the 'cheap' standalone options that cap payouts at 80% of your loan— that's a trap that'll cost you thousands when you need it most.

For instance, a Rivian owner I knew grabbed a $15/month gap policy online, only to find it didn't cover the full depreciation gap after an accident. 'Should I get gap insurance for my EV' means picking one with no exclusions, like those from major insurers. Hidden fees can add up, too—some charge $100 activation just to start coverage.

Bottom line: Always read the fine print; policies from dealers often have waiting periods or mileage caps that bite EV owners. That's the warning—don't cheap out and regret it later.

FAQs on Gap Insurance for EVs

What's the average cost of gap insurance for a Tesla Model 3? Typically, gap insurance for a Tesla Model 3 runs about $20-40 per month, depending on your insurer. That's a small price to avoid owing thousands if it's totaled, especially with 25% depreciation in year one. But shop around; Geico might offer it for $18/month versus Allstate's $35.

Should I get gap insurance if I'm leasing an EV like the BMW iX? Absolutely, if your lease payments exceed the car's value—leases often leave you owing more upfront. For a BMW iX, gap can cover the difference if it's wrecked early, saving you from mileage penalties. Still, check if your lease already includes it; most don't, so add it through your insurer.

Can I drop gap insurance after one year on my Hyundai Ioniq 5? Yeah, once your loan balance is below the car's value, usually after 2-3 years, you can drop it to save money. For a Hyundai Ioniq 5 depreciating at 20% annually, that might mean ditching it by year two. But verify with an appraisal first—'should I get gap insurance for my EV' evolves as values change.

Is dealer gap insurance better than from my insurer? Nope, insurer gap is usually cheaper and less markup-heavy; dealer's version can cost 40% more. For EVs, going with your policy provider avoids conflicts and ensures smoother claims. That's my take—always compare for the best deal.

Does gap insurance cover all types of EVs, like Rivian trucks? Yes, as long as you're financing or leasing, gap works for any EV, including Rivian trucks with their rapid depreciation. It covers the gap regardless of model, but confirm with your provider for specifics on high-value vehicles. Remember, it's not about the type; it's about your loan status.

How does EV depreciation affect 'should I get gap insurance for my EV'? EV depreciation, like 30% in the first year for some models, makes gap a smart move if you're owing more. This rapid drop increases the risk, so for buyers of new EVs, it's often essential to bridge that value gap. Check your equity annually to decide.

What's the difference between gap and regular insurance for EVs? Regular insurance covers repairs or replacement up to the car's current value, while gap handles the difference between that value and your loan balance. For EVs, this is key because of fast depreciation—without it, you're on the hook for the rest. Always bundle it if you're at risk.

So, there you have it—gap insurance for your EV isn't just another add-on; it's a shield against the depreciation beast. Weigh your options, crunch those numbers, and make the call that fits your ride. Go get yourself a better quote. You deserve it. — Alex